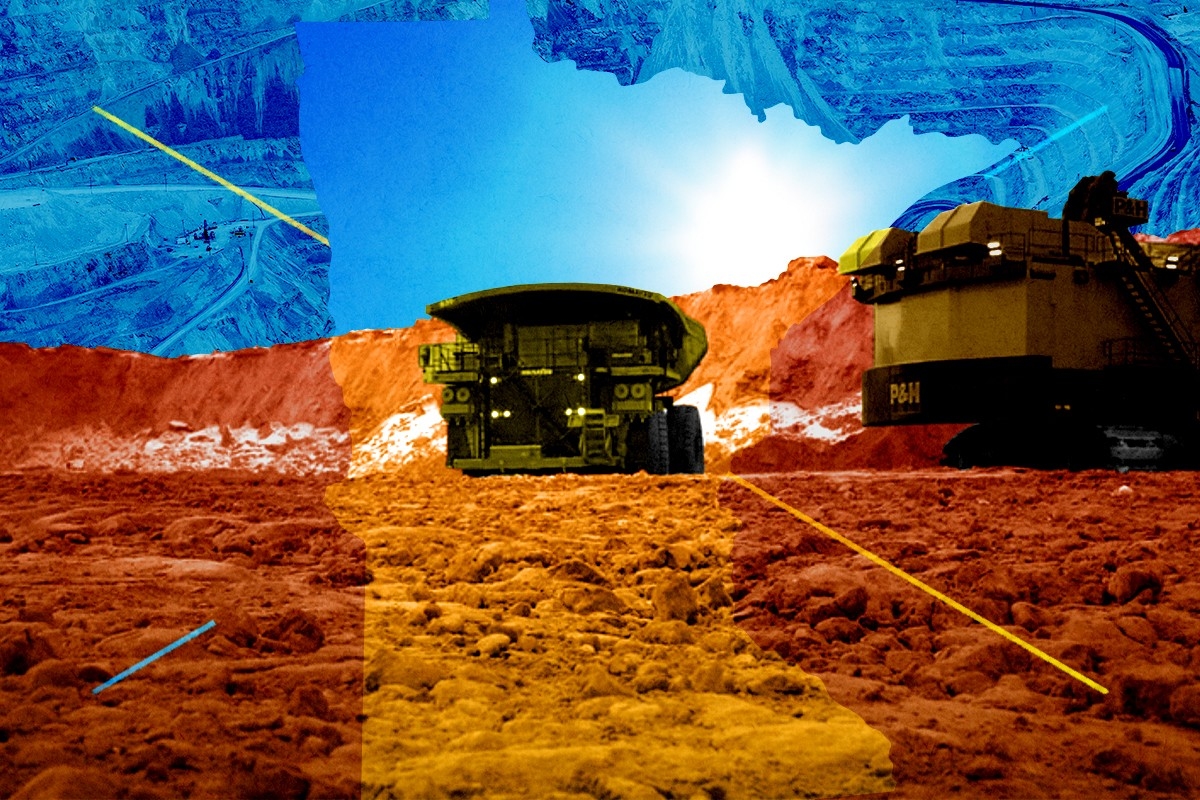

In northeastern Minnesota, a fight over the proposed NewRange Copper Nickel mine, better known as PolyMet, has dragged on for nearly two decades. Permits have been issued and revoked; state and federal agencies have been sued. The argument at the heart of the saga is familiar: Whether the pollution and disruption the mine will create are worth it for the jobs and minerals that it will produce.

The arguments are so familiar, in fact, that one wonders why we haven’t come up with a permitting and approval process that accounts for them. In total, the $1 billion NewRange project required more than 20 state and federal permits to move forward, all of which were secured by 2019. But since then, a number have been revoked or remanded back to the permit-issuing agencies. Just last year, for instance, the Army Corps of Engineers rescinded NewRange’s wetlands permit on the recommendation of the Environmental Protection Agency.

The messy history of this mine displays the difficult decisions the U.S. faces when it comes to securing the critical minerals that are key to a clean energy future — and the ways in which our current regulatory and permitting infrastructure is ill-equipped to resolve these tensions.

All sides in this debate recognize that minerals like nickel and copper are vital to the energy transition. Nickel is an integral component in most lithium-ion EV battery chemistries, and copper is used across a whole swath of technologies — electric vehicles, solar panels, and wind turbines, to name a few.

“We recognize that you're going to need copper, nickel, and other minerals in order to have a functioning society and to make the clean energy transition that we're all interested in,” Aaron Klemz, Chief Strategy Officer at the Minnesota Center for Environmental Advocacy, told me. But along with a number of other environmental groups and the Fond du Lac band of the Minnesota Chippewa tribe, which lives downstream of the proposed mine, MCEA opposes the project. “You can’t not mine. We understand that. But you have to take it on a case-by-case basis.”

On the one hand, the Duluth Complex, where the NewRange mine would be sited, contains one of the world’s largest untapped deposits of copper, nickel and other key metals. However, the critical minerals in this water-rich environment are bound to sulfide ores that can release toxic sulfuric acid when exposed to water and air. The proposed mine sits in a watershed that would eventually flow into Lake Superior, a critical source of drinking water for the Upper Midwest.

Many advocacy groups believe water pollution from the mine is inevitable, especially given NewRange’s plans for its waste basin. The current proposal involves covering the waste products, known as tailings, with water and containing the resulting slurry will with a dam. That’s considered much riskier than draining water from the tailings and “dry stacking” them in a pile. NewRange’s upstream dam construction method is also a concern, as the wet tailings can erode the dam’s walls more easily than with other designs. An upstream dam collapsed in Brazil in 2019, leading the country to ban this type of construction altogether.

And lastly, there’s the narrow question of the NewRange dam’s bentonite clay liner. Late last year, an administrative law judge recommended that state regulators refrain from reissuing NewRange’s permit to mine on the grounds that this liner was not a “practical and workable” method of containing the tailings.

Christie Kearney, director of sustainability, environmental and regulatory affairs for NewRange Copper Nickel, called these criticisms “tired and worn talking points” in a follow-up email to me, and said that the concerns simply don’t hold water “after the most comprehensive and lengthy environmental review and permitting process in Minnesota history.” The bentonite issue in particular, she told me, represents one of the main reasons permitting has been so challenging. “Instead of allowing agencies (who have the expertise) to make these decisions as established in Minnesota law, the regulatory decisions get challenged in court by mining opponents, leaving it to judges (who don’t have the technical expertise) to make these determinations,” she wrote.

The whole process could have gone more smoothly if all the stakeholders were involved from the beginning, she told me when we spoke. “In particular, we have a number of state permits that are overseen by the EPA, yet the EPA isn't involved until the very end, which has caused frustration both in our environmental review process as well as our permitting process.”

Klemz has another approach to ending the confusion. What is needed, he said, is a pathway to shut down projects once and for all if they’re deemed too environmentally hazardous. “There is no way to say no under the system we have now,” he told me. While courts can deny or revoke a permit, companies like NewRange can always go back to the drawing board and resubmit. “What we have instead is a system where the company has the incentive to keep on trying over and over and over again, despite whatever setback they encounter.”

While there’s no systematic way to block a mine, myriad avenues can lead to a “no.” Last year, the federal government placed a moratorium on mining on federal lands upstream of Minnesota’s Boundary Waters Canoe Wilderness Area, effectively shutting down another proposed copper-nickel mine. And the EPA banned the disposal of mine waste near Alaska’s proposed Pebble mine, blocking that project as well.

It’s a delicate balancing act, because ultimately the administration does want to incentivize domestic critical minerals production. The Inflation Reduction Act provides generous tax credits for companies involved in minerals processing, cathode materials production, and battery manufacturing. Then there’s the $7,500 credit available to consumers that purchase a qualifying EV, which depends on the automaker sourcing minerals from either the U.S. or a country the U.S. has a free-trade agreement with.

Under the current interpretation of the IRA, it’s possible that none of this money would flow directly to NewRange, since mineral extraction isn’t eligible for a tax credit, and it’s yet unclear whether the company will process the metals to a high enough grade to be eligible for credits there, either. Automakers that source from NewRange could benefit, but the project doesn’t currently have offtake agreements with any electric vehicle or clean energy company. That’s something that critics of the mine point to when NewRange touts its clean energy credentials.

“It's much more likely that this will end up in a string of Christmas lights than it will end up in a wind turbine in the United States,” Klemz told me. Of course, more critical minerals in the market overall will lower prices, thereby benefiting clean energy projects. But NewRange is a less neat proposition than, say, the proposed Talon Metals nickel mine, which is sited about two hours southwest of NewRange. As MIT Technology Review reports, this mine could unlock billions in federal subsidies through its offtake agreement with Tesla.

That hasn’t inoculated Talon from fierce local opposition, either. “As disinterested as the public may be in a lot of things, they are really engaged in a new mining project in their backyard,” said Adrian Gardner, Principal Nickel Markets Analyst at the energy and research consultancy Wood Mackenzie, which has been tracking both the Talon and NewRange mine since they were first proposed.

The Biden administration is also engaged. Two years ago, the Department of the Interior convened an interagency working group to make domestic minerals production more sustainable and efficient, starting with the Mining Law of 1872 — still the law of the land when it comes to new mining projects. The group released a report last September recommending, among other things, that the Bureau of Land Management and U.S. Forest Service provide standardized guidance to prospective developers and require meetings between all relevant agencies and potential developers before any applications are submitted. That means Congress will need to provide more resources to permitting agencies.

Those resources could come from a proposed royalty of between 4% and 8% on the net proceeds of minerals extracted from public lands, a fee that would also go to help communities most impacted by mining. The National Mining Association, of which NewRange is a member, has come out strongly against the report’s recommendations, highlighting the high royalties as a particular point of contention.

But many of the report’s proposals might have helped NewRange in its early days. “There were a lot of early missteps by the company,” Kearney admits. “The first draft [Environmental Impact Statement] that the company went through received a very poor reading from the EPA, and the company went back to its drawing board, changed out its leadership and its environmental leads.”

More stern rebukes, of course, would be the ideal for many advocacy groups. “I don't know how they could redesign it quite honestly, given what we know about the science, to comply with the law,” Klemz said.

Kearney is adamant, though, that even after five years of litigation, NewRange has no plans to give up the fight. “Not many companies can weather that,” Kearney said. Not many companies, however, are backed by mining giant Glencore. PolyMet, the project’s original developer, “really only survived because Glencore came in a few years back and invested over time until the point where they got 100% control,” Kearney told me.

Glencore, a $65 billion Swiss company, is pursuing the NewRange project in partnership with Teck Resources, which is worth $20 billion. The companies can afford to fight for a very long time, meaning nobody knows quite how or when this all ends.

“We do need this material. I get that,” Klemz told me. “So I don't really know if there's going to be some kind of neat future resolution to this.”

Kearney put it simply. “We don't have a timeline right now.”

Charred remains of a truck and a home in Spokane's Balboa neighborhood. Erick Doxey / AFP via Getty Images

Charred remains of a truck and a home in Spokane's Balboa neighborhood. Erick Doxey / AFP via Getty Images