With the markets for electric vehicles and battery energy storage systems on the come-up, energy market analysts predict that the world is hurtling towards a global lithium shortage by the 2030’s. Lithios, a Massachusetts-based startup with a novel method of lithium extraction, is aiming to help by unlocking previously untapped lithium resources around the world.

The company just raised a $12 million seed round to help fund this mission, led by Clean Energy Ventures with support from Lowercarbon Capital, among others. The round included $10 million in venture funding and $2 million in venture debt loans from Silicon Valley Bank.

It’s not as if the world actually lacks for lithium, the energy dense mineral that is the primary component in lithium-ion batteries. It’s just that many current reserves are too low-grade to be economically exploited, and traditional extraction methods are land-intensive, inefficient, and often controversial with local communities. Chile, Australia, and China dominate the market, while the U.S. contributes less than 2% of the world’s annual supply.

Lithios aims to make it more economical and environmentally friendly to extract lithium from salty groundwater deposits, a.k.a. brines. The company’s CEO, Mo Alkhadra, told me that while about two-thirds of the world’s lithium is contained in brine rather than hard rock, only about 15% to 20% of these brines are currently worth mining. Lithios, he said, will get that number up to around 80% to 85%, in theory. “The vision with Lithios’ tech is to enable access to these lower-grade resources at a similar or maybe slightly higher cost structure relative to the highest grade deposits that are mined today,” Alkhadra explained.

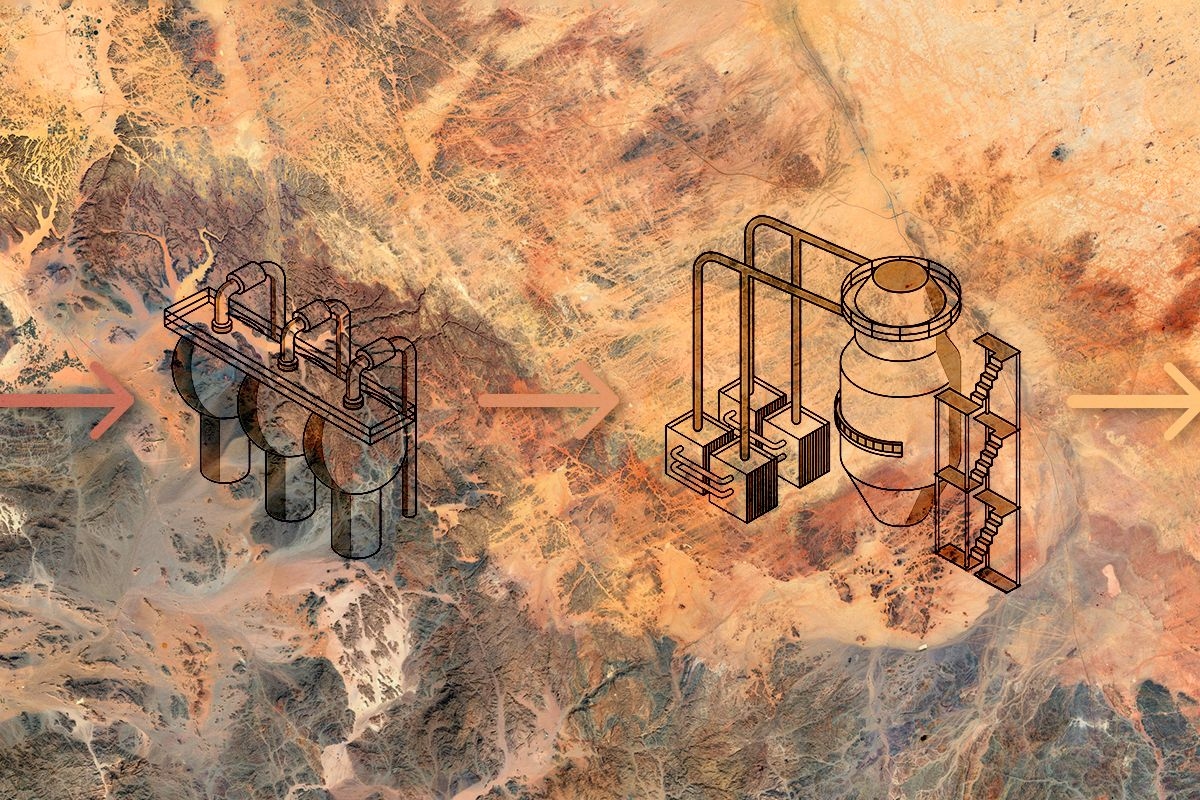

The normal lithium brine extraction process involves pumping saline water from underground reservoirs to the surface, where it’s then moved through a series of large, wildly colored evaporation ponds, often located in the middle of vast salt deserts. Over a period of about 18 months, the sun slowly evaporates the brine, leaving behind increasingly high concentrations of lithium. But Lithios’ tech avoids these ponds altogether. Instead, the brine is pumped to the surface and delivered directly to the company’s refrigerator-sized electrochemical reactors, which contain stacks of electrodes that capture the lithium.

While the company wouldn't disclose the electrodes’ exact chemistry, Alkhadra told me they are made from “inorganic compounds which have geometries that fit basically only lithium and none of the other larger ions that you would find in these brine mixtures.” After lithium is extracted, the company produces a purified lithium concentrate and sends that off for refining into battery chemicals. The final batteries could end up in EVs, energy storage systems, or even just plain old portable consumer electronics.

Lithios’ tech comes at a good time, as the Inflation Reduction Act’s domestic content requirements for EVs incentivizes manufacturers to source critical minerals from the U.S. and countries that the U.S. has free trade agreements with. Alkhadra told me that Lithios could open up opportunities for brine mining in the Smackover formation, which spans a number of southern states including Texas and Arkansas, the Salton Sea area, which has been dubbed “Lithium Valley,” as well as deposits in Utah and Nevada. More areas in Canada and Europe could also be in play. (The company said it couldn’t talk yet about any specific partnership agreements.)

While there are a number of other companies such as Lilac Solutions and EnergyX that are also pursuing more efficient and less land-intensive brine-based extraction methods, they rely on a different, purely chemical process known as direct lithium extraction, which uses technology adapted from the water treatment industry. “The core thesis around what we're building at Lithios stems from that work,” Alkhadra told me, explaining that electrifying these chemical processes makes them “much more selective, energy efficient, and water efficient” — resulting in “modest to significant cost reduction.”

Lithios’ new funding will help the company scale its research and development efforts as well as build out a pilot facility in Medford, Massachusetts, with initial production to begin in the first quarter of next year. At first, output will be limited to just “several battery packs” per year, Alkhadra told me, scaling up to commercial production “in the coming years.”

Alkhadra is excited to see investors and the federal government alike beginning to express interest in the upstream, “dirtier” portions of the battery supply chain, which he told me have generally been overlooked in favor of downstream sectors such as battery manufacturing and cell production. “I think the U.S. departments of both energy and defense, and investors too, are coming to realize that the real bottlenecks in battery manufacturing and EV production are on the resource side.”

A transformer factory in Jiangsu Province, China. Costfoto/NurPhoto via Getty Images

A transformer factory in Jiangsu Province, China. Costfoto/NurPhoto via Getty Images