In a tumultuous time for clean energy financing, leading infrastructure investment firm Generate Capital is seeking to realign its approach. Last month the firm trumpeted its appointment of a new CEO, the first in its 11-year history. Less publicly, it also implemented firm-wide layoffs, representatives confirmed to Heatmap.

“Like many others in our space, we grew quickly and made some mistakes,” Jonah Goldman, Generate’s head of external affairs, told me. He was responding to a report from infrastructure and energy intelligence platform IJ Global, which last week reported that Generate had “shut down its equity investing arm” and laid off 50 people. While Goldman confirmed that there were indeed layoffs earlier this summer, he would not specify how many employees were let go, and disputed the claim that any particular team was dissolved. “We have not ‘shut down’ any strategies,” he told me. “Our investment team continues to find opportunities across the capital stack.”

Goldman’s comments echoed those of the firm’s new CEO, David Crane, a former undersecretary for infrastructure at the Department of Energy. In an article published to Generate’s website a few weeks ago, Crane admitted that the firm had “deviated from our operational roots,” a reference to the firm’s unconventional investment strategy.

Generate is unique as a sustainability-focused investor, in that it often acts as an owner and operator for the projects it finances rather than taking a passive equity stake The firm also provides tailored project financing options for its partners to help manage risk.

But over the past few years, Generate made a number of large equity investments in companies whose projects it did not directly oversee. These included utility-scale solar and energy storage developer Pine Gate Renewables, which is on the verge of bankruptcy, and green hydrogen developer Ambient Fuels, which was recently acquired by Electric Hydrogen amidst tumult in the industry.

“While other investors had no choice but to act as pure investors, we were distracted from who we are and what we were good at,” Crane wrote, noting that this distraction led to “poor performance in one component of our investment portfolio.” That would appear to be its equity division.

Generate’s model is designed to bridge a critical gap in the climate tech ecosystem known as the “missing middle,” the phase at which a company with some proven tech has outgrown early-stage venture capital but is still considered too risky for most traditional infrastructure investors. Historically, the firm has generated high returns by backing “leading-edge technologies,” Jigar Shah, the firm’s co-founder and former director of the DOE’s Loan Programs Office, said on the Open Circuit podcast he co-hosts. These include investments in projects involving fuel cells, anaerobic digesters, and battery storage.

Shah hasn’t worked at Generate since he joined the Biden administration in 2021. But from the outside, he says, the firm appears to have moved away from taking these riskier but potentially more lucrative bets. “They ended up with 38 people in their capital markets team, and their capital markets team went out to the marketplace and said, Hey, we have all this stuff to sell. And the people that they went to said, Well, that’s interesting, but what we really would love is boring community solar,“ Shah said on the podcast. As he saw it, Generate began making equity investments into lower-risk projects such as community solar, which naturally generated stable but lower returns. Then once interest rates went up post-Covid, that put downward pressure on equity returns.

Shah said it’s these slipping returns that have made it harder for Generate to raise capital over the past two years. Axios Pro recently reported that the firm is now exploring an IPO to bring in additional funding, following hesitation from some of its existing backers to reinvest.

While Goldman acknowledged that “there is some skepticism in the capital markets about our space now,” he disagreed with the idea that Generate has abandoned its focus on leading-edge technologies. “We have invested over the last number of years in a lot of assets that are predictable assets with predictable cash flows that have performed very strongly for our investors. And we continue to have the creativity of the team that’s focused on trying to bring newer technologies to the market to bridge the bankability gap,” he told me.

By way of example, he highlighted two of the firm’s most recent investments, a $200 million loan to Pacific Steel Group for the first green steel mill in California and a $100 million scalable credit facility for green data center developer Soluna, which allows the company to increase its borrowing capacity as new projects come online.

The latter deal was announced just weeks after Crane stepped into his new role. Having served as the CEO of five publicly traded energy companies before joining Generate, Crane is now promising to turn around the firm’s fortunes. With the Trump administration rolling back federal support for clean energy infrastructure and investors remaining cautious, Crane has said that now is the time to jump on undervalued opportunities.

“Right now, there’s a lot of noise telling people to stop writing checks. But this is precisely the time to invest in the infrastructure that will power the next twenty years,” he wrote. Goldman backed this up, telling me, “We believe managers who understand the space and who can take advantage of the opportunities that are underpriced in this tougher market environment are set up to succeed.”

Just as tech giants such as Google, Salesforce, and Amazon were able to expand rapidly in the wake of the dot-com bubble and consolidate their positions in the market, Generate’s leadership say they’re now well positioned to help select clean energy companies do the same.

It will certainly be a boon for the sector if they can, given the abundance of undercapitalized climate tech opportunities, from clean cement to thermal energy storage, next-generation geothermal, and carbon capture, all looking to build first-of-a-kind projects. And there’s not nearly enough infrastructure funding to go around.

So if Generate has indeed lost the confidence of its investors, it’s critical that Crane, Goldman, and company regain it swiftly. Their ability to do so could shape not only which technologies drive the energy transition, but how quickly they do so.

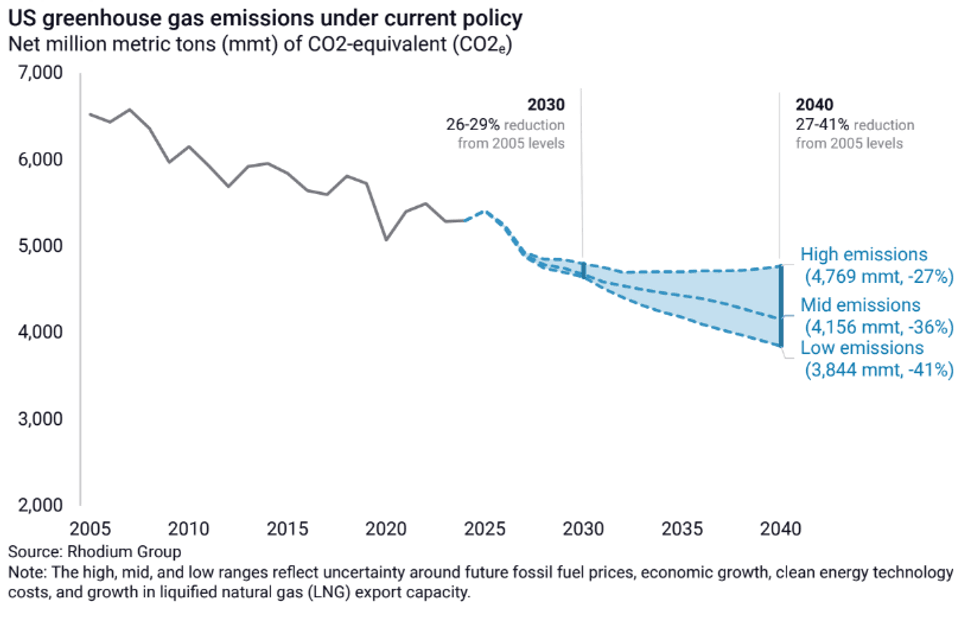

The 2030s crossroads.Rhodium Group

The 2030s crossroads.Rhodium Group