Preliminary data from Princeton University’s REPEAT Project (led by Heatmap contributor Jesse Jenkins) forecasts that said bill will have a dramatic effect on the deployment of clean energy in the U.S., including reducing new solar and wind capacity additions by almost over 40 gigawatts over the next five years, and by about 300 gigawatts over the next 10. That would be enough to power 150 of Meta’s largest planned data centers by 2035.

But clean energy development will hardly grind to a halt. While much of the bill’s implementation is in question, the bill as written allows for several more years of tax credit eligibility for wind and solar projects and another year to qualify for them by starting construction. Nuclear, geothermal, and batteries can claim tax credits into the 2030s.

Shares in NextEra, which has one of the largest clean energy development businesses, have risen slightly this year and are down just 6% since the 2024 election. Shares in First Solar, the American solar manufacturer, are up substantially Thursday from a day prior and are about flat for the year, which may be a sign of investors’ belief that buyer demand for solar panels will persist — or optimism that the OBBBA’s punishing foreign entity of concern requirements will drive developers into the company’s arms.

Partisan reversals are hardly new to climate policy. The first Trump administration gleefully pulled the rug from under the Obama administration’s power plant emissions rules, and the second has been thorough so far in its assault on Biden’s attempt to replace them, along with tailpipe emissions standards and mileage standards for vehicles, and of course, the IRA.

Even so, there are ways the U.S. can reduce the volatility for businesses that are caught in the undertow. “Over the past 10 to 20 years, climate advocates have focused very heavily on D.C. as the driver of climate action and, to a lesser extent, California as a back-stop,” Hannah Safford, who was director for transportation and resilience in the Biden White House and is now associate director of climate and environment at the Federation of American Scientists, told Heatmap. “Pursuing a top down approach — some of that has worked, a lot of it hasn’t.”

In today’s environment, especially, where recognition of the need for action on climate change is so politically one-sided, it “makes sense for subnational, non-regulatory forces and market forces to drive progress,” Safford said. As an example, she pointed to the fall in emissions from the power sector since the late 2000s, despite no power plant emissions rule ever actually being in force.

“That tells you something about the capacity to deliver progress on outcomes you want,” she said.

Still, industry groups worry that after the wild swing between the 2022 IRA and the 2025 OBBA, the U.S. has done permanent damage to its reputation as a business-friendly environment. Since continued swings at the federal level may be inevitable, building back that trust and creating certainty is “about finding ballasts,” Harry Godfrey, the managing director for Advanced Energy United’s federal priorities team, told Heatmap.

The first ballast groups like AEU will be looking to shore up is state policy. “States have to step up and take a leadership role,” he said, particularly in the areas that were gutted by Trump’s tax bill — residential energy efficiency and electrification, transportation and electric vehicles, and transmission.

State support could come in the form of tax credits, but that’s not the only tool that would create more certainty for businesses — considering the budget cuts states will face as a result of Trump’s tax bill, it also might not be an option. But a lot can be accomplished through legislative action, executive action, regulatory reform, and utility ratemaking, Godfrey said. He cited new virtual power plant pilot programs in Virginia and Colorado, which will require further regulatory work to “to get that market right.”

A lot of work can be done within states, as well, to make their deployment of clean energy more efficient and faster. Tyler Norris, a fellow at Duke University's Nicholas School of the Environment, pointed to Texas’ “connect and manage” model for connecting renewables to the grid, which allows projects to come online much more quickly than in the rest of the country. That’s because the state’s electricity market, ERCOT, does a much more limited study of what grid upgrades are needed to connect a project to the grid, and is generally more tolerant of curtailing generation (i.e. not letting power get to the grid at certain times) than other markets.

“As Texas continues to outpace other markets in generator and load interconnections, even in the absence of renewable tax credits, it seems increasingly plausible that developers and policymakers may conclude that deeper reform is needed to the non-ERCOT electricity markets,” Norris told Heatmap in an email.

At the federal level, there’s still a chance for, yes, bipartisan permitting reform, which could accelerate the buildout of all kinds of energy projects by shortening their development timelines and helping bring down costs, Xan Fishman, senior managing director of the energy program at the Bipartisan Policy Center, told Heatmap. “Whether you care about energy and costs and affordability and reliability or you care about emissions, the next priority should be permitting reform,” he said.

And Godfrey hasn’t given up on tax credits as a viable tool at the federal level, either. “If you told me in mid-November what this bill would look like today, while I’d still be like, Ugh, that hurts, and that hurts, and that hurts, I would say I would have expected more rollbacks. I would have expected deeper cuts,” he told Heatmap. Ultimately, many of the Inflation Reduction Act’s tax credits will stick around in some form, although we’ve yet to see how hard the new foreign sourcing requirements will hit prospective projects.

While many observers ruefully predicted that the letter-writing moderate Republicans in the House and Senate would fold and support whatever their respective majorities came up with — which they did, with the sole exception of Pennsylvania Republican Brian Fitzpatrick — the bill also evolved over time with input from those in the GOP who are not openly hostile to the clean energy industry.

“You are already seeing people take real risk on the Republican side pushing for clean energy,” Safford said, pointing to Alaska Republican Senator Lisa Murkowski, who opposed the new excise tax on wind and solar added to the Senate bill, which earned her vote after it was removed.

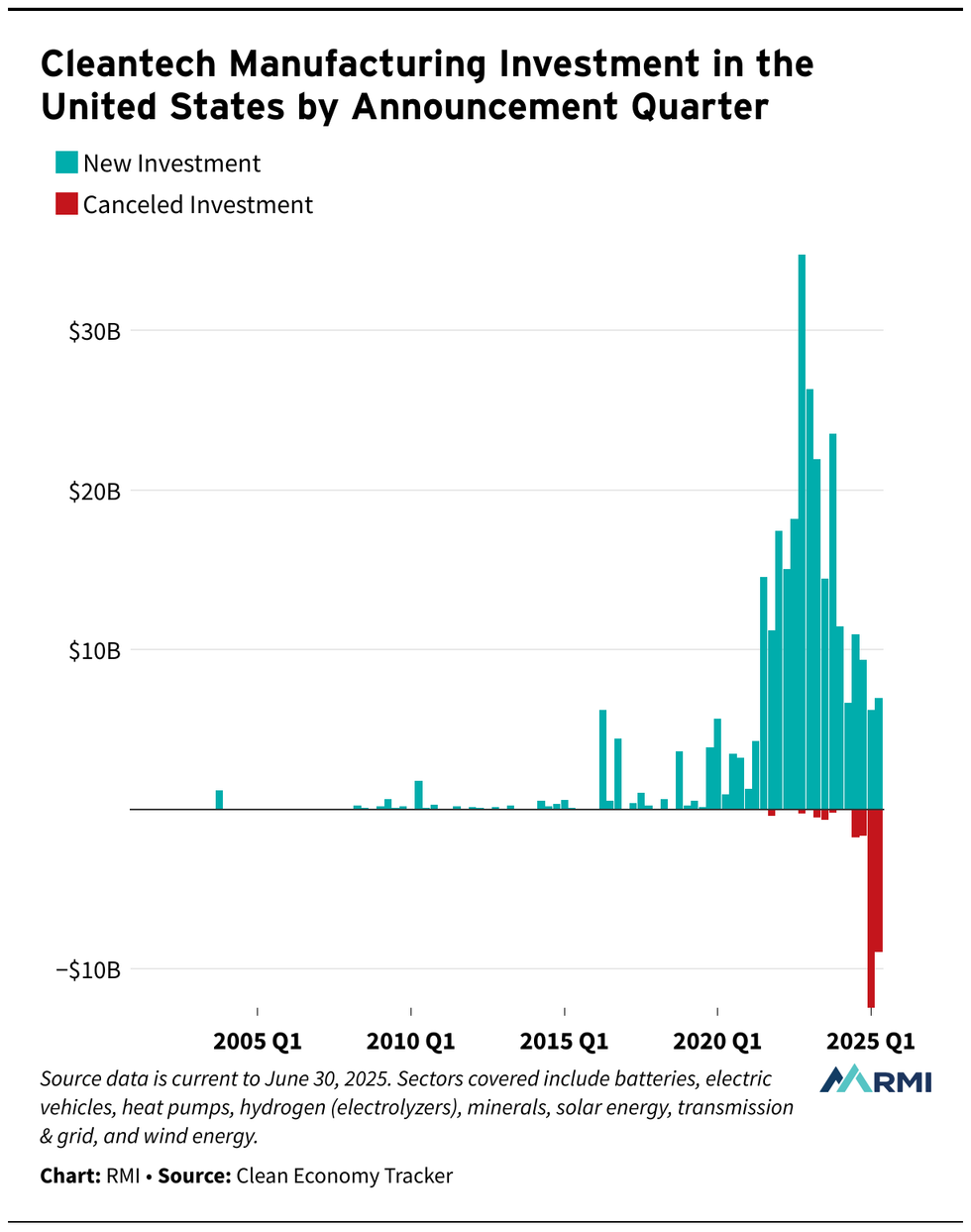

Some damage has already been done, however. Canceled clean energy investments adds up to $23 billion so far this year, compared to just $3 billion in all of 2024, according to the decarbonization think tank RMI. And that’s before OBBBA hits Trump’s desk.

The start-and-stop nature of the Inflation Reduction Act may lead some companies, states, local government and nonprofits to become leery of engaging with a big federal government climate policy again.

“People are going to be nervous about it for sure,” Safford said. “The climate policy of the future has to be polycentric. Even if you have the political opportunity to make a big swing again, people will be pretty gun shy. You will need to pursue a polycentric approach.”

But to Godfrey, all the back and forth over the tax credits, plus the fact that Republicans stood up to defend them in the 11th hour, indicates that there is a broader bipartisan consensus emerging around using them as a tool for certain energy and domestic manufacturing goals. A future administration should think about refinements that will create more enduring policy but not set out in a totally new direction, he said.

Albert Gore, the executive director of the Zero Emissions Transportation Association, was similarly optimistic that tax credits or similar incentives could work again in the future — especially as more people gain experience with electric vehicles, batteries, and other advanced clean energy technologies in their daily lives. “The question is, how do you generate sufficient political will to implement that and defend it?” he told Heatmap. “And that depends on how big of an economic impact does it have, and what does it mean to the American people?”

Ultimately, Fishman said, the subsidy on-off switch is the risk that comes with doing major policy on a strictly partisan basis.

“There was a lot of value in these 10-year timelines [for tax credits in the IRA] in terms of business certainty, instead of one- or two- year extensions,” Fishman told Heatmap. “The downside that came with that is that it became affiliated with one party. It was seen as a partisan effort, and it took something that was bipartisan and put a partisan sheen on it.”

The fight for tax credits may also not be over yet. Before passage of the IRA, tax credits for wind and solar were often extended in a herky-jerky bipartisan fashion, where Democrats who supported clean energy in general and Republicans who supported it in their districts could team up to extend them.

“You can see a world where we have more action on clean energy tax credits to enhance, extend and expand them in a future congress,” Fishman told Heatmap. “The starting point for Republican leadership, it seemed, was completely eliminating the tax credits in this bill. That’s not what they ended up doing.”