In the spring of 2021, the world’s leading authority on energy published a “roadmap” for preventing the most catastrophic climate change scenarios. One of its conclusions was particularly daunting. Getting energy-related emissions down to net zero by 2050, the International Energy Agency said, would require “huge leaps in innovation.”

Existing technologies would be mostly sufficient to carry us down the carbon curve over the next decade. But after that, nearly half of the remaining work would have to come from solutions that, for all intents and purposes, did not exist yet. Some would only require retooling existing industries, like developing electric long-haul trucks and carbon-free steel. But others would have to be built from almost nothing and brought to market in record time.

What will it take to rapidly develop new solutions, especially those that involve costly physical infrastructure and which have essentially no commercial value today?

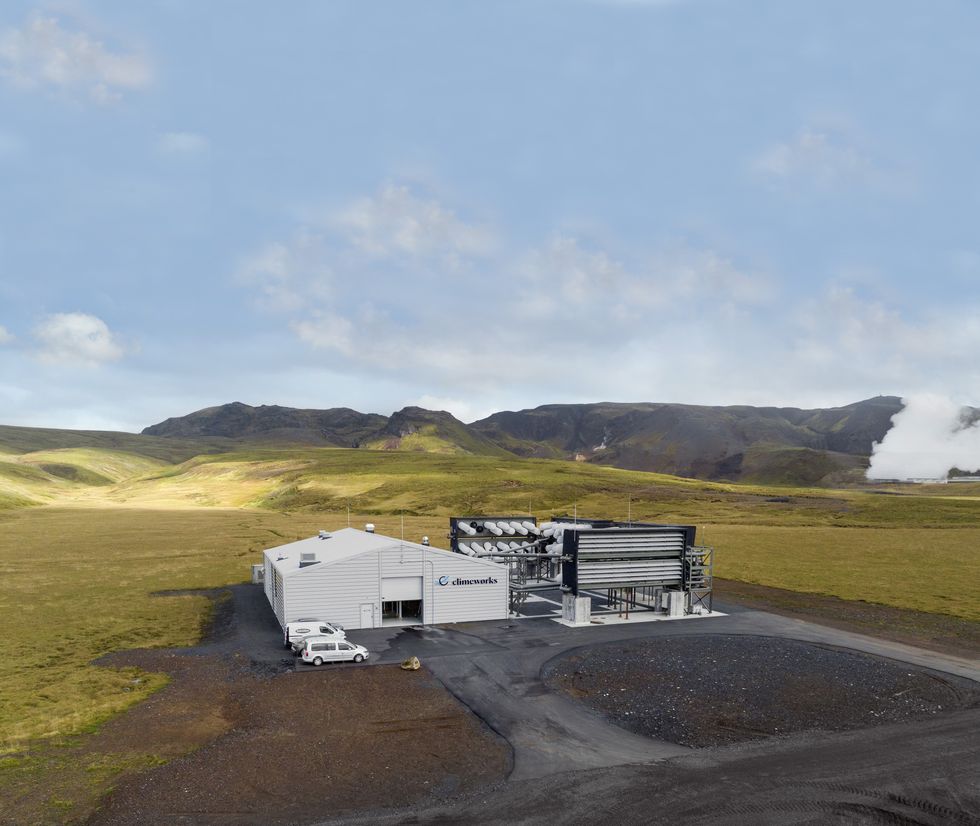

That’s the challenge facing Climeworks, the Swiss company developing machines to wrest carbon dioxide molecules directly from the air. In September 2021, a few months after the IEA’s landmark report came out, Climeworks switched on its first commercial-scale “direct air capture” facility, a feat of engineering it dubbed “Orca,” in Iceland.

The technology behind Orca is one of the top candidates to clean up the carbon already blanketing the Earth. It could also be used to balance out any stubborn, residual sources of greenhouse gases in the future, such as from agriculture or air travel, providing the “net” in net-zero. If we manage to scale up technologies like Orca to the point where we remove more carbon than we release, we could even begin cooling the planet.

As the largest carbon removal plant operating in the world, Orca is either trivial or one of the most important climate projects built in the last decade, depending on how you look at it. It was designed to capture approximately 4,000 metric tons of carbon from the air per year, which, as one climate scientist, David Ho, put it, is the equivalent of rolling back the clock on just 3 seconds of global emissions. But the learnings gleaned from Orca could surpass any quantitative assessment of its impact. How well do these “direct air capture” machines work in the real world? How much does it really cost to run them? And can they get better?

The company — and its funders — are betting they can. Climeworks has made major deals with banks, insurers, and other companies trying to go green to eventually remove carbon from the atmosphere on their behalf. Last year, the company raised $650 million in equity that will “unlock the next phase of its growth,” scaling the technology “up to multi-million-ton capacity … as carbon removal becomes a trillion-dollar market.” And just last month, the U.S. Department of Energy selected Climeworks, along with another carbon removal company, Heirloom, to receive up to $600 million to build a direct air capture “hub” in Louisiana, with the goal of removing one million tons of carbon annually.

Two years after powering up Orca, Climeworks has yet to reveal how effective the technology has proven to be. But in extensive interviews, top executives painted a picture of innovation in progress.

Chief marketing officer Julie Gosalvez told me that Orca is small and climatically insignificant on purpose. The goal is not to make a dent in climate change — yet — but to maximize learning at minimal cost. “You want to learn when you're small, right?” Gosalvez said. “It’s really de-risking the technology. It’s not like Tesla doing EVs when we have been building cars for 70 years and the margin of learning and risk is much smaller. It’s completely new.”

From the ground, Orca looks sort of like a warehouse or a server farm with a massive air conditioning system out back. The plant consists of eight shipping container-sized boxes arranged in a U-shape around a central building, each one equipped with an array of fans. When the plant is running, which is more or less all the time, the fans suck air into the containers where it makes contact with a porous filter known as a “sorbent” which attracts CO2 molecules.

Courtesy of Climeworks

Courtesy of Climeworks

When the filters become totally saturated with CO2, the vents on the containers snap shut, and the containers are heated to more than 212 degrees Fahrenheit. This releases the CO2, which is then delivered through a pipe to a secondary process called “liquefaction,” where it is compressed into a liquid. Finally, the liquid CO2 is piped into basalt rock formations underground, where it slowly mineralizes into stone. The process requires a little bit of electricity and a lot of heat, all of which comes from a carbon-free source — a geothermal power plant nearby.

A day at Orca begins with the morning huddle. The total number on the team is often in flux, but it typically has a staff of about 15 people, Climeworks’ head of operations Benjamin Keusch told me. Ten work in a virtual control room 1,600 miles away in Zurich, taking turns monitoring the plant on a laptop and managing its operations remotely. The remainder work on site, taking orders from the control room, repairing equipment, and helping to run tests.

During the huddle, the team discusses any maintenance that needs to be done. If there’s an issue, the control room will shut down part of the plant while the on-site workers investigate. So far, they’ve dealt with snow piling up around the plant that had to be shoveled, broken and corroded equipment that had to be replaced, and sediment build-up that had to be removed.

Courtesy of Climeworks

Courtesy of Climeworks

The air is more humid and sulfurous at the site in Iceland than in Switzerland, where Climeworks had built an earlier, smaller-scale model, so the team is also learning how to optimize the technology for different weather. Within all this troubleshooting, there’s additional trade-offs to explore and lessons to learn. If a part keeps breaking, does it make more sense to plan to replace it periodically, or to redesign it? How do supply chain constraints play into that calculus?

The company is also performing tests regularly, said Keusch. For example, the team has tested new component designs at Orca that it now plans to incorporate into Climeworks’ next project from the start. (Last year, the company began construction on “Mammoth,” a new plant that will be nine times larger than Orca, on a neighboring site.) At a summit that Climeworks hosted in June, co-founder Jan Wurzbacher said the company believes that over the next decade, it will be able to make its direct air capture system twice as small and cut its energy consumption in half.

“In innovation lingo, the jargon is we haven’t converged on a dominant design,” Gregory Nemet, a professor at the University of Wisconsin who studies technological development, told me. For example, in the wind industry, turbines with three blades, upwind design, and a horizontal axis, are now standard. “There were lots of other experiments before that convergence happened in the late 1980s,” he said. “So that’s kind of where we are with direct air capture. There’s lots of different ways that are being tried right now, even within a company like Climeworks."

Although Climeworks was willing to tell me about the goings-on at Orca over the last two years, the company declined to share how much carbon it has captured or how much energy, on average, the process has used.

Gosalvez told me that the plant’s performance has improved month after month, and that more detailed information was shared with investors. But she was hesitant to make the data public, concerned that it could be misinterpreted, because tests and maintenance at Orca require the plant to shut down regularly.

“Expectations are not in line with the stage of the technology development we are at. People expect this to be turnkey,” she said. “What does success look like? Is it the absolute numbers, or the learnings and ability to scale?”

Danny Cullenward, a climate economist and consultant who has studied the integrity of various carbon removal methods, did not find the company’s reluctance to share data especially concerning. “For these earliest demonstration facilities, you might expect people to hit roadblocks or to have to shut the plant down for a couple of weeks, or do all sorts of things that are going to make it hard to transparently report the efficiency of your process, the number of tons you’re getting at different times,” he told me.

But he acknowledged that there was an inherent tension to the stance, because ultimately, Climeworks’ business model — and the technology’s effectiveness as a climate solution — depend entirely on the ability to make precise, transparent, carbon accounting claims.

Nemet was also of two minds about it. Carbon removal needs to go from almost nothing today to something like a billion tons of carbon removed per year in just three decades, he said. That’s a pace on the upper end of what’s been observed historically with other technologies, like solar panels. So it’s important to understand whether Climeworks’ tech has any chance of meeting the moment. Especially since the company faces competition from a number of others developing direct air capture technologies, like Heirloom and Occidental Petroleum, that may be able to do it cheaper, or faster.

However, Nemet was also sympathetic to the position the company was in. “It’s relatively incremental how these technologies develop,” he said. “I have heard this criticism that this is not a real technology because we haven’t built it at scale, so we shouldn’t depend on it. Or that one of these plants not doing the removal that it said it would do shows that it doesn’t work and that we therefore shouldn’t plan on having it available. To me, that’s a pretty high bar to cross with a climate mitigation technology that could be really useful.”

More data on Orca is coming. Climeworks recently announced that it will work with the company Puro.Earth to certify every ton of CO2 that it removes from the atmosphere and stores underground, in order to sell carbon credits based on this service. The credits will be listed on a public registry.

But even if Orca eventually runs at full capacity, Climeworks will never be able to sell 4,000 carbon credits per year from the plant. Gosalvez clarified that 4,000 tons is the amount of carbon the plant is designed to suck up annually, but the more important number is the amount of “net” carbon removal it can produce. “That might be the first bit of education you need to get out there,” she said, “because it really invites everyone to look at what are the key drivers to be paid attention to.”

She walked me through a chart that illustrated the various ways in which some of Orca’s potential to remove carbon can be lost. First, there’s the question of availability — how often does the plant have to shut down due to maintenance or power shortages? Climeworks aims to limit those losses to 10%. Next, there’s the recovery stage, where the CO2 is separated from the sorbent, purified, and liquified. Gosalvez said it’s basically impossible to do this without losing some CO2. At best, the company hopes to limit that to 5%.

Finally, the company also takes into account “gray emissions,” or the carbon footprint associated with the business, like the materials, the construction, and the eventual decommissioning of the plant and restoration of the site to its former state. If one of Climeworks’ plants ever uses energy from fossil fuels (which the company has said it does not plan to do) it would incorporate any emissions from that energy. Climeworks aims to limit gray emissions to 15%.

In the end, Orca’s net annual carbon removal capacity — the amount Climeworks can sell to customers — is really closer to 3,000 tons. Gosalvez hopes other carbon removal companies adopt the same approach. “Ultimately what counts is your net impact on the planet and the atmosphere,” she said.

Get one great climate story in your inbox every day:

Despite being a first-of-its-kind demonstration plant — and an active research site — Orca is also a commercial project. In fact, Gosalvez told me that Orca’s entire estimated capacity for carbon removal, over the 12 years that the plant is expected to run, sold out shortly after it began operating. The company is now selling carbon removal services from its yet-to-be-built Mammoth plant.

In January, Climeworks announced that Orca had officially fulfilled orders from Microsoft, Stripe, and Shopify. Those companies have collectively asked Climeworks to remove more than 16,000 tons of carbon, according to the deal-tracking site cdr.fyi, but it’s unclear what portion of that was delivered. The achievement was verified by a third party, but the total amount removed was not made public.

Climeworks has also not disclosed how much it has charged companies per ton of carbon, a metric that will eventually be an important indicator of whether the technology can scale to a climate-relevant level. But it has provided rough estimates of how much it expects each ton of carbon removal to cost as the technology scales — expectations which seem to have shifted after two years of operating Orca.

In 2021, Climeworks co-founder Jan Wurzbacher said the company aimed to get the cost down to $200 to $300 per ton removed by the end of the decade, with steeper declines in subsequent years. But at the summit in June, he presented a new cost curve chart showing that the price was currently more than $1,000, and that by the end of the decade, it would fall to somewhere between $400 to $700. The range was so large because the cost of labor, energy, and storing the CO2 varied widely by location, he said. The company aims to get the price down to $100 to $300 per ton by 2050, when the technology has significantly matured.

Critics of carbon removal technologies often point to the vast sums flowing into direct air capture tech like Orca, which are unlikely to make a meaningful difference in climate change for decades to come. During a time when worsening disasters make action feel increasingly urgent, many are skeptical of the value of investing limited funds and political energy into these future solutions. Carbon removal won’t make much of a difference if the world doesn’t deploy the tools already available to reduce emissions as rapidly as possible — and there’s certainly not enough money or effort going into that yet.

But we’ll never have the option to fully halt climate change, let alone begin reversing it, if we don’t develop solutions like Orca. In September, the International Energy Agency released an update to its seminal net-zero report. The new analysis said that in the last two years, the world had, in fact, made significant progress on innovation. Now, some 65% of emission reductions after 2030 could be accounted for with technologies that had reached market uptake. It even included a line about the launch of Orca, noting that Climeworks’ direct air capture technology had moved from the prototype to the demonstration stage.

But it cautioned that DAC needs “to be scaled up dramatically to play the role envisaged,” in the net zero scenario. Climeworks’ experience with Orca offers a glimpse of how much work is yet to be done.

Read more about carbon removal:

The Dawn of a New Climate Industry

Courtesy of Climeworks

Courtesy of Climeworks Courtesy of Climeworks

Courtesy of Climeworks