What happens after solar modules get cheap? The relentless cost declines for solar technology driven by mass production and steady innovation — largely in China — has resulted in a commercial ecosystem where pricing is dominated by everything but the solar panels themselves.

In this world, a more efficient panel is not necessarily one that costs less to buy from a supplier, but rather one that can optimize on these “soft costs,” getting more energy out of the given time and money spent on installing the panel. This will come to matter more and more as solar costs inevitably plateau — and especially if Congress decides to eliminate clean energy incentives under the Inflation Reduction Act, which, combined with high tariffs on solar imports from Asia, could take away solar’s cost advantage over new natural gas-fired power.

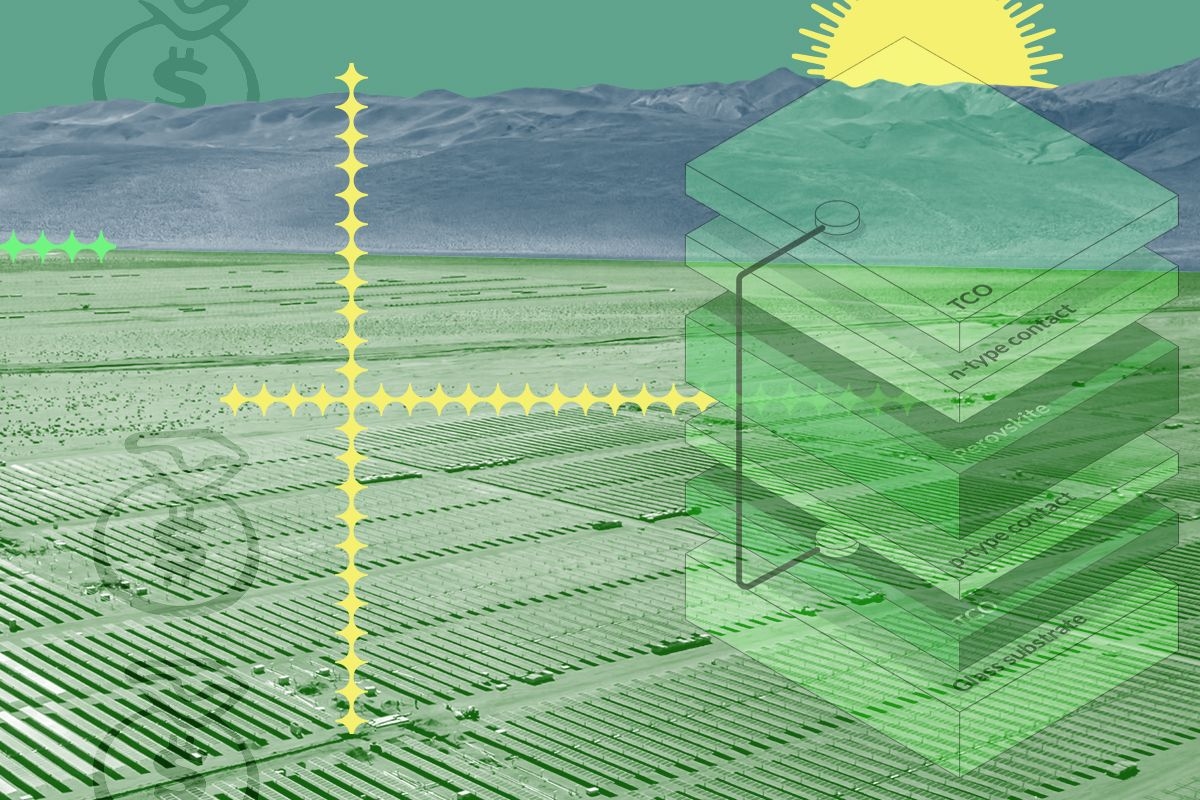

At least that’s the thesis of Tandem PV, which uses so-called perovskite technology to build solar panels that, the company says, are already more efficient than existing silicon panels, and could become almost twice as efficient as existing panels as the technology improves. Perovskite refers to a group of minerals that share a similar structure and which, when stacked with silicon, can absorb a broad range of light, maximizing the efficiency of converting light to electricity.

I spoke with Tandem PV chief executive Scott Wharton about why he thinks that even in this era of rock bottom costs, greater performance will still win the day. Our conversation has been edited for length and clarity.

Why does it not matter so much that your solar panels are a little more expensive than other ones?

Well, I would say, for the whole history of solar panels, the cost of it was really high. There was this move to get the cost down, reduce the green premium, etc. We’re now in a world where that view is, I would say, antiquated.

And by cost, you mean the cost of the physical module.

The cost of the panel itself, yeah. The reason why is that for utility scale, which is where we’re focused on, only 20% of the cost is the panel. So 80% of the actual cost of a solar deployment — which is what matters, right? The cost of deploying it — labor, land, the balance of systems, the construction loans. It’s typical, I would say, of engineers — everything’s about the commodity. Whereas from my experience, it depends on the total cost. What we’re doing is, we’re saving the cost where it matters: on the labor.

So I guess the argument you’re trying to make is that even if the upfront cost of the panel is higher, the higher efficiency actually does make the kind of physical cost over time go down — and then all the soft costs, I imagine, are basically the same. Or is there any argument why the soft costs would be different, too?

First of all, I’m not sure that we will charge a premium. We want to be the same or cheaper. But even if we did, the point is that most of the cost is in those other things: labor, land, and installation. So if our panel has 30% more power in a single panel — a 28% [efficient] panel is about [third] more [efficient] than a 21% panel — then you need 30% fewer panels.

The other thing I learned recently is that people think that, oh, you just have this huge parcel of land and everything is equal. But a lot of times, when you’re deploying solar, you can’t actually fit everything on one parcel. So there’s a savings from having more density.

There’s also an issue where a lot of the best solar locations are taken, or you don’t have a ton of choice, necessarily, about where you put your panels because co-location matters so much. So it’s even more important to have efficiency in how you use that land.

Where is Tandem PV on the trajectory from lab to mass deployment?

We just announced a $50 million [Series A funding round], and we’re building out the first significant commercial perovskite factory in the United States. Conventional wisdom for manufacturing is, you put it as far away as possible. I think when you’re trying to do something really new, it’s probably the same story: It seems cheaper, but it’s not. Because if it takes you six more months because you’re flying back and forth and people don’t understand each other, then that actually costs you money and time and delay. We’re going to emphasize quality and speed over cost.

If we do this right, then the theory is, we’ve become the next First Solar — that’s our intention. We want to take back solar leadership from China, which is a bold statement, but I think we’re on the journey. I tell the team, it’s like a bicycle race, where you go slowly, slowly, slowly, and then there’s a point where you need to break out. Well, I think we’ve broken out. Whether we fall flat on our face because we’re exhausted or we jump out ahead, we’ll see what history writes.

Obviously a big story in the solar industry is cost declining so much, and that’s tied to, a very specific technological stack. What do you guys have to do besides demonstrating results to tell the story that a different technology might be necessary?

So number one, there’s a reason why people are interested in perovskites. It’s 200 times thinner than traditional silicon panels — no rare earth minerals or metals, no mining.

What people don’t know about silicon solar is, you’ve got to heat this up to, like, 2,000 degrees Celsius to purify it, and it’s very, very expensive. We’re using the same glass and basically putting on a 1 micron-thick layer of ink. So we’re adding a little bit of cost, but you get a lot more energy for it than what you add.

The second thing is, we’re not actually competing with silicon so much as we’re building on top of it. As silicon technology gets better and cheaper, our product gets better and cheaper. And then the third thing is, see point number one, where we started. If you have a 28% or 30% [efficient] panel — by the way, silicon hits its physics limits at 26%. It can never get better than that. So we’re already better than where silicon is. And as labor and land become more expensive in the United States and around the world, it actually is cheaper to make something that focuses on where all the costs are.

I know you’re not in mass production yet, but are you going out to utility scale developers? Do they want a more efficient panel, or are they just comfortable working with the stuff they normally work with?

It’s both. They like what they have, but their feedback is — especially given all the supply chain risks that are going on around the world — if you can build it, we’ll buy it. We’re basically building something that is the same thing they already have, for a market that we already know. And is there a market for electricity? Yeah, there’s going to be a huge shortage of it with the AI boom. So we feel pretty confident that if we can build this, they will come.

Putting aside public policy issues, what’s to stop one of the big Chinese solar manufacturers from using this technology? People have been talking about it for decades.

It’s like any hard thing. It’s not a secret that people want to have rockets and go to space, it’s just a very, very hard technology. It’s the same thing as, why did Google and Apple win back the mobile phone war from the Japanese and the Germans and others? It’s a leapfrogging thing. I think the market’s up for grabs.

Feel the Burnham. Carl Court/Getty Images

Feel the Burnham. Carl Court/Getty Images