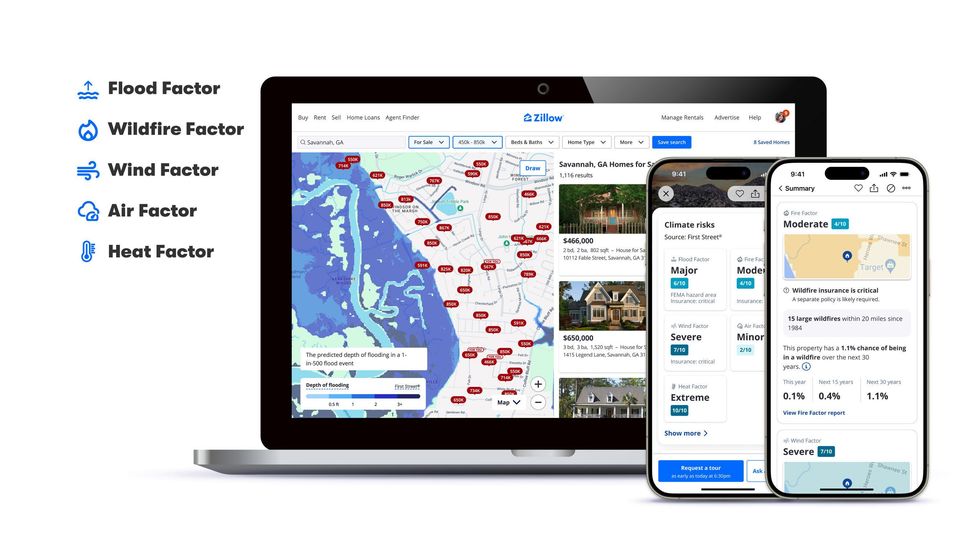

Starting this month, the tens of millions of Americans who browse the real-estate listings website Zillow will encounter a new type of information.

In addition to disclosing a home’s square footage, school district, and walkability score, Zillow will begin to tell users about its climate risk — the chance that a major weather or climate event will strike in the next 30 years. It will focus on the risk from five types of dangers: floods, wildfires, high winds, heat, and air quality.

The data has the potential to transform how Americans think about buying a home, especially because climate change will likely worsen many of those dangers. About 70% of Americans look at Zillow at some point during the process of buying a home, according to the company.

“Climate risks are now a critical factor in home-buying decisions,” Skylar Olsen, Zillow’s chief economist, said in a statement. “Healthy markets are ones where buyers and sellers have access to all relevant data for their decisions.”

That’s true — if the information is accurate. But can homebuyers actually trust Zillow’s climate risk data? When climate experts have looked closely at the underlying data Zillow uses to assess climate risk, they have walked away unconvinced.

Zillow’s climate risk data comes from First Street Technology, a New York-based company that uses computer models to estimate the risk that weather and climate change pose to homes and buildings. It is far and away the most prominent company focused on modeling the physical risks of climate change. (Although it was initially established as a nonprofit foundation, First Street reorganized as a for-profit company and accepted $46 million in investment earlier this year.)

But few experts believe that tools like First Street’s are capable of actually modeling the dangers of climate change at a property-by-property level. A report from a team of White House scientific advisors concluded last year that these models are of “questionable quality,” and a Bloomberg investigation found that different climate risk models could return wildly different catastrophe estimates for the same property.

Courtesy of Zillow

Courtesy of Zillow

Not all of First Street’s data is seen as equally suspect. Its estimates of heat and air pollution risk have generally attracted less criticism from experts. But its estimates of flooding and wildfire risk — which are the most catastrophic events for homeowners — are generally thought to be inadequate at best.

So while Zillow will soon tell you with seeming precision that a certain home has a 1.1% chance of facing a wildfire in the next 30 years, potential homebuyers should take that kind of estimate with “a lot of grains of salt,” Michael Wara, a senior research scholar at the Stanford Woods Institute for the Environment, told me.

Here’s a short guide for how to think through Zillow’s estimates of climate risk.

Neither First Street nor Zillow immediately responded to requests for comment.

If Zillow tells you a property has flooded recently, take it seriously.

Zillow has said that, when the data is available, it will tell users whether a given home has flooded or burned in a wildfire recently. (It will also say whether a home is near a source of air pollution.)

Homebuyers should take that information seriously, Madison Condon, a Boston University School of Law professor who studies climate change and financial markets, told me.

“If the house flooded in the recent past, then that should be a major red flag to you,” she said. Houses that have flooded recently are very likely to flood again, she said. Only 10 states require a home seller to disclose a flood to a potential buyer.

Use Zillow’s flood risk assessment as a starting place — but contact the local government to learn more.

First Street claims that its physics-based models can identify the risk that any individual property will flood. But the ability to determine whether a given house will flood depends on having an intricate knowledge of local infrastructure, including stormwater drains and what exists on other properties, and that data does not seem to exist in anyone’s model at the moment, Condon said.

When Bloomberg compared the output of three different flooding models, including First Street’s, they agreed on results for only 5% of properties.

If you’re worried about a home’s flood risk, then contact the local government and see if you can look at a flood map or even talk to a flood manager, Condon said. Many towns and cities keep flood maps in their records or on their website that are more granular than what First Street is capable of, she said.

“The local flood manager who has walked the property will almost always have a better grasp of flood risk than the big, top-down national model,” she said.

Don’t hesitate to buy flood insurance.

In some cases, Zillow will recommend that a home buyer purchase federal flood insurance. That’s generally not a bad idea, Condon said, even if Zillow reaches that conclusion using national model data that has errors or mistakes.

“It simply is true that way more people should be buying flood insurance than generally think they should,” she said. “So a general overcorrection on that would be good.”

Zillow probably underestimates a home’s wildfire risk, especially out west.

If you’re looking at buying a home in a wildfire-prone area, especially in the American West, then you should generally assume that Zillow is underestimating its wildfire risk, Wara, the Stanford researcher, told me.

That’s because computer models that estimate wildfire risk are in a fairly early stage of development and improving rapidly. Even the best academic simulations lack the kind of granular, structure-level data that would allow them to predict a property’s forward-looking wildfire risk.

That is actually a bigger problem for homebuyers than for insurance companies, he said. A home insurance company gets to decide whether to insure a property every year. If it looks at new science and concludes that a given town or structure is too risky, then it can raise its premiums or even simply decline to cover a property at all. (State Farm stopped selling home insurance policies in California last year, partly because of wildfire risk.)

But when homeowners buy a house, their lives and their wealth get locked into that property for 30 years. “Maybe your kids are going to the school district,” he said. It’s much harder to sell a home when you can’t get it covered. “You have an illiquid asset, and it’s a lot harder to move.”

That means First Street’s wildfire risk data should be taken as “absolute minimum estimate,” Wara said. In a wildfire-prone area, “the real risk is most likely much higher” than its models say.

Wildfire models are especially bad at predicting the most destructive types of fires.

Over the past several years, runaway wildland fires have killed dozens of people or destroyed tens of thousands of homes in Lahaina, Hawaii; Paradise, California; and Marshall, Colorado.

But in those cases, once the fire began incinerating homes, it ceased to be a wildland fire and became a structure-to-structure fire. The fire began to leap from house to house like a book of matches, condemning entire neighborhoods to burn within minutes.

Modern computer models do an especially poor job of simulating that transition — the moment when a wildland fire becomes an urban conflagration, Wara said. Although it only happens in perhaps 0.5% of the most intense fires, those fires are responsible for destroying the most homes.

But “how that happens and how to prevent that is not well understood yet,” he said. “And if they’re not well understood yet from a scientific perspective, that means it’s not in the [First Street] model.”

Nor do the best university wildfire models have good data on every individual property’s structural-level details — such as what material its walls or roof are made of — that would make it susceptible to fire.

Your whole neighborhood matters when assessing flood or wildfire risk.

When assessing whether your home faces wildfire risk, its structure is very important. But “you have to know what your neighbor’s houses look like, too, within about a 250-yard radius. So that’s your whole neighborhood,” Wara said. “I don’t think anyone has that data.”

A similar principle goes for thinking about flood risk, Condon said. Your home might not flood, she said, but it also matters whether the roads to your house are still driveable or whether the power lines fail. “It’s not particularly useful to have a flood-resilient home if your whole neighborhood gets washed out,” she said.

Experts agree that the most important interventions to discourage wildfire — or, for that matter, floods — have to happen at the community level. Although few communities are doing prescribed burns or fuel reduction programs right now, some are, Wara said.

But because nobody is collecting data about those programs, national risk models like First Street’s would not factor those programs into an area’s wildfire risk, he said. (In the rare case that a government is clearing fuel or doing a prescribed burn around a town, wildfire risk there might actually be lower than Zillow says, Wara added.)

Going forward, figuring out a property’s climate risk — much like pushing for community-level resilience investment — shouldn’t be left up to individuals, Condon said.

The state of California is investing in a public wildfire catastrophe model so that it can figure out which homes and towns face the highest risk. She said that Fannie Mae and Freddie Mac, the federal entities that buy home mortgages, could invest in their own internal climate-risk assessments to build the public’s capacity to understand climate risk.

“I would advocate for this not to be an every-man-for-himself, every-consumer-has-to-make-a-decision situation,” Condon said.

Courtesy of Zillow

Courtesy of Zillow

EIA

EIA