In a warming world where winter snow is melting earlier and rain is arriving later, “wildfire season” has become somewhat of a misnomer. Some parts of the country now see blazes popping up practically year round. This, combined with decades of fire management policy that promoted suppression over natural and controlled burns, has turned certain states — California, most famously — into tinderboxes.

With wildfire smoke becoming a standard component of Silicon Valley summers, it’s probably no surprise that numerous data analytics and artificial intelligence-focused startups have sprung up to address the issue. There’s even a San Francisco-based venture capital firm, Convective Capital, devoted solely to funding wildfire solutions.

“My big question coming into starting Convective was, are there enough companies in this category?” Bill Clerico, founder and managing partner of the firm told me. The answer, he found, was yes. After establishing Convective Capital in the beginning of 2022, he said, “we’ve identified about 500 of what we call fire tech companies.” They run the gamut from startups that work on wildfire suppression to those dealing with identification, prevention, mitigation, and insurance against damages.

Rhizome, a company making an AI-powered wildfire risk mitigation platform for utilities, is one of the firm’s most recent investments. “Think of it as Sim City for the grid,” Mishal Thadani, CEO of the Washington, D.C.-based startup, told me. “You obviously need to know, as extreme weather events hit, how this is going to affect your assets,” he explained.

Rhizome’s platform gives utilities insight into, “if there is an asset failure, given the asset type, the type of failure, and the burn probability given the vegetation makeup and the dryness conditions, what’s going to be the likelihood of a wildfire ignition?” This information helps utilities decide where to put their money, whether that means replacing a power line or pole, insulating conductors, undergrounding power lines, or trimming back a bush. Last month, Rhizome announced a $1 million investment from Convective Capital, not tied to a particular funding round. The company raised $2.5 million in its pre-seed round last year.

The problem is not simply a lack of data, Thadani told me — utilities often know things about their assets such as last inspection date and outage history, and have systems that can render the surrounding landscape and other infrastructural features. The problem is that data is not part of a holistic system that can provide comprehensive insights. If risk analysis is being performed, Thadani said, “it’s being done on a super scrappy spreadsheet basis.”

Rhizome aims to build the “connective tissue” between a utility’s disparate data systems, then combine that with other geographic datasets on climate, weather, and vegetation. From there, the company uses its machine learning models to assess the likelihood of extreme weather events and their subsequent impacts. Ultimately, this allows utilities to provide regulators with more quantifiable information on their plans to improve grid resiliency and prevent wildfires, beyond just citing a figure for how much money they want to spend.

Utilities are not exactly known for their technical prowess, but are hungry nevertheless for solutions to their wildfire woes. Pacific Gas & Electric, the nation’s largest utility, was driven into bankruptcy after being found liable for a spate of enormous California wildfires in 2017 and 2018. After reemerging from bankruptcy in 2020, it now has a plan to spend $18 billion on wildfire mitigation through 2025. Other utilities such as Hawaii Electric and Berkshire Hathaway Energy face billions in potential liabilities for wildfires in their service areas.

The most common customers for companies in Convective Capital’s portfolio are utilities, governments, and insurance companies. “These are tremendously deep-pocketed institutions, but they are not, you know, necessarily the most fast-moving or innovative,” he told me. “And so that is the fundamental challenge of building a wildfire technology company.”

So far, Rhizome has announced partnerships with two utilities, Seattle City Light and Vermont Electric Power Company. But Clerico acknowledges that getting traditional institutions onboard is no easy task, even when the benefits seem clear. The magnitude of the destruction in recent years has served as an accelerant, though — something the vegetation management platform provider AiDash has seen first hand. Abhishek Singh, cofounder and CEO of the startup (which is not in Convective’s portfolio), said that when he founded the company in 2019, “Every investor warned us not to do this because utilities don’t buy and they won’t invest.” But that’s not what he’s experienced.

AiDash raised $58.5 million in an oversubscribed Series C round earlier this year, led by the impact investor Lightrock, and has five utility partnerships, including Southern California Edison’s holding company, Edison International, as well as Duke Energy. The company uses satellite data and AI analytics to assess vegetation near utility infrastructure for wildfire risk. It can also detect faults by fusing satellite data with other sources such as thermal or LiDAR-based imagery. (Convective Capital sees the value proposition in using satellites for vegetation management, too — it’s invested in one of AiDash’s direct competitors, an Amsterdam-based startup called Overstory.)

When Singh founded AiDash in 2019, both the size and cost of satellites were plummeting, leading to far more launches and thus far more data. . “Since the history of the first satellite until 2018, there were 2,200-odd satellites launched,” he told me. “From 2019 onwards, each year close to 1,000 satellites are getting launched.” The company purchases mounds of that data to conduct its vegetation analyses.

Vegetation management is typically the largest line item in a utility’s operations and maintenance budgets, Singh told me, costing the entire sector around $6 billion or $7 billion annually. “It’s also the single largest cause of utility-caused wildfires, as well as the cause of most outages,” he said, as power lines coming into contact with trees, grasses, and shrubs can easily spark a fire. Anything that can help them trim that budget and preempt the need for costly equipment repairs is worth a lot. “These are all million dollar contracts,” Singh told me.

But big data platforms alone are just one tool in the vast toolbox that comprises a holistic approach to wildfire management. “There’s no panacea, where you just do one thing and then it solves the problem,” Clerico told me. “It’s going to get solved as a combination of consistent and repeated forest management, building towns and cities that are fire adapted, building great infrastructure, and then having the ability to detect and respond quickly. All of these things are huge, multi decade, multi billion dollar investments.”

So for the foreseeable future, Convective Capital will have its work cut out for it. But when I asked Clerico if one day, in a beautiful, far-off dreamland, there might not be the need for a dedicated wildfire tech VC, he said he hopes so.

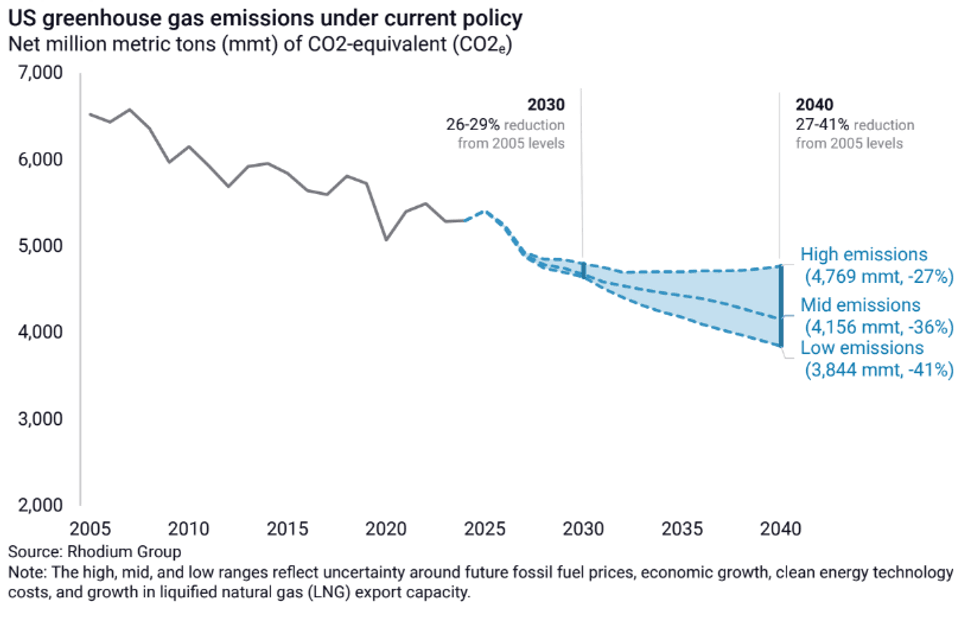

The 2030s crossroads.Rhodium Group

The 2030s crossroads.Rhodium Group