The breakthrough in Wisconsin shows how investing in local interventions can accelerate the energy transition — and points the way forward for clean energy advocates trying to navigate federal headwinds.

As skyrocketing electricity demand and soaring costs draw attention to our power systems, clean energy offers a formidable solution. Wind, solar, and storage technologies have matured enough that they can be built quickly and cheaply virtually anywhere, for anyone, at any scale. And now, as the world contends with yet another conflict roiling fossil fuel markets, these energy sources offer a shield from volatility.

Given these clear advantages, it’s worth asking, “Why aren’t clean energy projects moving forward faster in more places?”

Our team at Invest in Our Future has learned a lot in the past three years about the answer.

Invest in Our Future’s creation marked a departure from philanthropy’s longstanding approach to climate and clean energy, which often focused on developing and passing policy to spur reductions in greenhouse gas pollution. Instead, with the Inflation Reduction Act on the books, my organization was formed with a singular focus: maximize the reach and impact of federal clean energy investments in the face of on-the-ground constraints.

Our remit was to ensure this ambitious policy advancing commercially-ready technology resulted in actual projects getting built and benefiting people. That meant mobilizing organizations to raise awareness of IRA programs and incentives and help communities access IRA dollars. It also meant finding a way around the significant barriers that stood in the way of deployment, even with historic levels of government support.

First, utility-scale projects were hit with organized, vocal opposition upset by the prospect of rapid changes to the local landscape and skeptical of out-of-town developers. That resistance often seized on siting and permitting processes to delay or altogether stop projects from being built. And too infrequently did countervailing forces try to speak to their concerns or organize support.

There were also funding problems for more community-oriented projects. In many cases, neither private investors nor public officials fully understood the opportunity or potential returns for projects like rooftop solar for schools, microgrids for hospitals and health centers, or electrified buses that double as mobile batteries during blackouts, leaving a sizable project pipeline struggling to pencil out.

Clean energy employers also struggled to hire, and workers couldn’t see a career path in the sector.

And as media habits changed, and national leaders spread disinformation, clean energy got more polarized.

For some, there was a political logic behind the IRA that suggested new projects would set off a self-reinforcing cycle of support for federal clean energy policy. But building support and real champions takes time. Consider that utility-scale solar projects, for example, need 24 months at minimum just to reach operational status. The work of connecting projects and benefits in the public mind extends further still. With barriers slowing deployment, the advantages of new projects needed time to take root.

Still, where projects did move forward, Invest in Our Future cultivated local validators who could share authentic stories about how clean energy improved their lives. When we mobilized local champions to engage with decisionmakers last year, they left a big impression. But we needed more of them — from more places, drawing value from more projects.

So after Congress repealed much of the IRA last summer, we developed new, interlocking strategies to address the major barriers to deployment and push as many projects forward in as many communities as possible.

By educating local decision-makers early and mobilizing active, vocal support from a wide range of perspectives — farmers and faith leaders, landowners and labor, educators and entrepreneurs — we can boost the number of projects that secure siting and permitting approvals.

By identifying high-potential, commercial-scale community projects with local lenders, packaging them into aggregated investments, and demonstrating low risk and reliable returns, we can draw institutional investors and lower-cost capital toward an otherwise underfunded but important segment.

Setting high and consistent job quality standards across clean energy industries will counter real and perceived concerns around safety, benefits, and wages, helping attract more workers who can go on to serve as advocates for new projects.

And deepening investment in storytelling by local champions will build the credibility of — and, in turn, support for — clean energy projects from the ground up.

Market forces are increasingly and irreversibly favoring clean energy. Influential allies of the president are coming around on solar, and longtime critics of renewables acknowledge that the transition is inevitable. What’s needed most now is a push from the ground up.

Our grantees are delivering it. Their work on siting and permitting, for example, helped gain approval for nearly 20 gigawatts of clean capacity in 2025. That included projects like Wisconsin’s Badger Hollow wind farm and Illinois’s 210-megawatt Glacier Moraine solar project — which was initially denied a permit but triumphed in a reconsideration vote after more than a dozen local residents mobilized to sway public opinion. Greenlight America and their partners managed to win eight permitting campaigns over one week last December alone.

Yet funding for these efforts is limited. Climate solutions receive less than 2% of total giving. Most funding within that segment has long flowed to regulatory and policy-focused work, which made sense while clean energy needed policy support to compete on economics. But today, with clean energy cheaper than fossil fuels in most parts of the country, there’s a real gap between our goals and on-the-ground success that we can bridge by focusing more on getting projects built.

Deploying clean energy at the community level happens to be one of our most effective tools for drawing down greenhouse gas pollution — with the added advantage of helping to lower costs, strengthen economic growth and community resilience, and generate good jobs. Through Invest in Our Future, I’ve met leaders driving progress often in the most challenging places in the country. Despite all the setbacks and discouraging headlines last year brought, these leaders have not lost their sense of urgency, or their resolve to build clean energy. That resolve — and their track record of success — should give us all hope. We should give them our support in return.

Constellation's Clinton Clean Energy Center nuclear plant in Clinton, Illinois. Scott Olson/Getty Images

Constellation's Clinton Clean Energy Center nuclear plant in Clinton, Illinois. Scott Olson/Getty Images

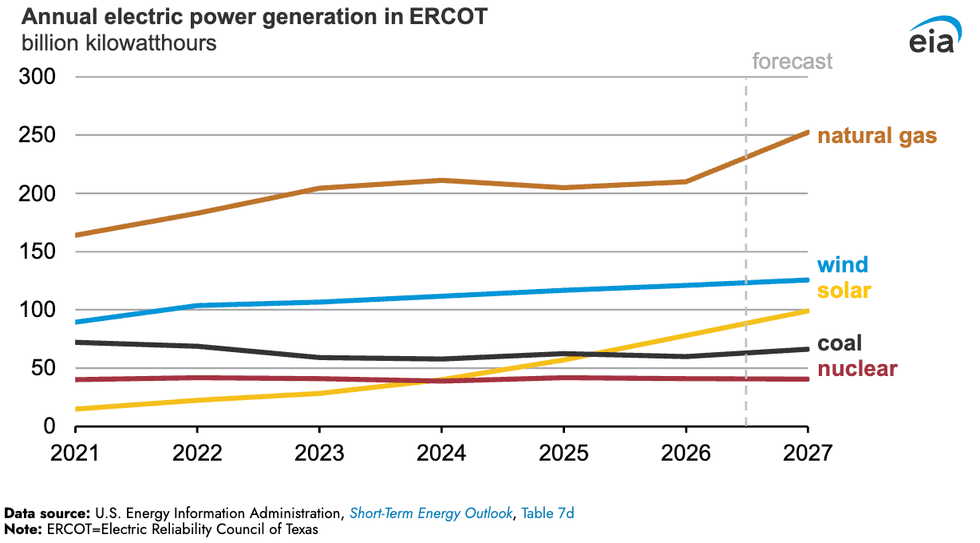

Solar is now the third-largest electricity source in Texas.EIA

Solar is now the third-largest electricity source in Texas.EIA