While SpaceX founder and Tesla CEO Elon Musk is often lauded for turning technology like reusable rockets and American-made electric vehicles into thriving businesses in a way long thought impossible, or at least improbable, he has also more quietly done something about as unlikely: get investors excited about capital-intensive hard tech startups.

For most of the time Musk was sleeping on the floor of Tesla’s factory to oversee Model 3 assembly and his rockets were riding across the country on the back of flatbed trucks, the venture capitalists that fund the next generation of technology companies were largely enamored with software businesses, which required little capital to start up and could scale quickly with accelerating profitability.

Today, thanks in no small part to Musk, hard tech companies are able to raise hundreds of millions of dollars within a few years of being starting up, with top-flight venture capital firms such as Andreessen Horowitz building whole funds devoted to the broad sector.

That investor interest has helped nurture a series of startups founded and led by former SpaceX and Tesla employees. These types of businesses don’t have the forgiving characteristics of software companies; instead, they’re often incredibly capital intensive, and require years of design and manufacturing before profits show up. Climate tech and energy companies almost inevitably fall in this category, often working on trying to turn technology that may mostly exist in a lab with nascent markets and high barriers to scale into something that can generate real returns for investors.

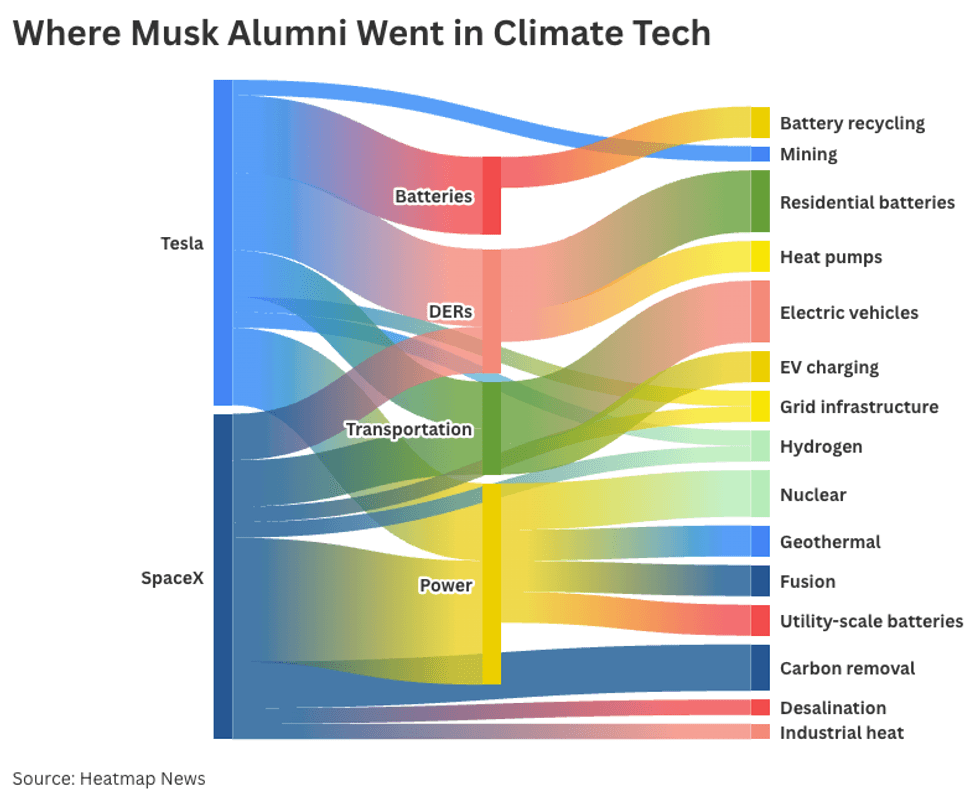

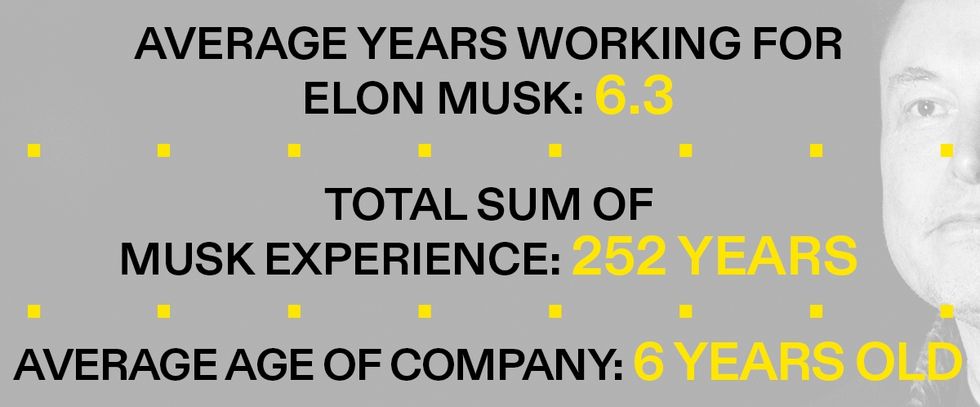

To mark the occasion of SpaceX’s initial public offering, Heatmap decided to survey the landscape of SpaceX and Tesla alumni now cutting their own swath through the climate tech marketplace. We identified 40 founders and executives, who all together spent a total of 252 years working for Musk. They’ve since moved on to companies in 9 different industries, from Musk-adjacent categories such as batteries and electric vehicles to carbon removal and grid tech. Cumulatively they’ve raised at least $27 billion, according to the data available in Crunchbase. (Since we finalized this list, one more Musk alum-founded company has emerged from stealth. Welcome to the world, Ambrosia Energy.)

Heatmap asked these founders and executives by email what they learned from their experiences working at Musk-led companies, and we heard back from more than a dozen of them. The vast majority of those told us it was no accident that they’d ended up where they have after working for Musk.

“While working at Tesla, I was surrounded by people who were there for the hard stuff and thrived on it,” Mateo Jaramillo, co-founder and CEO of the long-duration battery company Form Energy and a former Tesla Energy vice president, told us. “It's not just that they tolerated it — that was the stuff they lived for. There are moments in a company's arc when that kind of mentality is required, and at Tesla in those days it was like walking through a crucible every single day, with truly no idea how things were going to resolve. And yet you keep going and figure it out along the way.”

Musk himself has been a formidable digester of investor capital, including from Founders Fund, the venture capital firm founded by his former PayPal colleague Peter Thiel, which invested in SpaceX before its first successful launch.

Founders Fund has since become an investor in several Musk-alumni-founded companies, including the fuel enrichment startup General Matter, the geothermal company Endurance Energy, and the hydrogen company Hgen.

Another frequent investor, Andreessen Horowitz, had previously been the great promoter of software businesses. Its cofounders Marc Andreessen and Ben Horowitz wrote the seminal essay “Why Software Is Eating The World,” which became a manifesto for its investments in businesses like Facebook (now Meta) and Twitter (now X). Since then, a16z, as it’s known, has expanded its remit and invested in several Musk-alumni founded companies, including the power electronics company Heron Power, the mining services company Mariana Minerals, electric boat company Arc, and home battery company Base Power.

These investments are not just simply giving money to Tesla and SpaceX employees to do the same things they did in their previous jobs. Many of the companies we looked at were founded by SpaceX alumni and have nothing to do with space, rockets, or satellites.

Mike Schroepfer, former Meta chief technical officer and founder of hard tech VC firm Gigascale Capital, which has invested in Heron and Form, as well as clean power and carbon removal company Arbor and nuclear microreactor company Radiant, told us that when founders have a Musk company on their resume, it tells him “they’ve been trained to build in the physical world, which is rarer than people think.”

And what’s rare can be profitable.

“Hardware is capital-intensive for the best possible reason” Schroepfer said. “You’re building the foundations the world runs on, and those things have to work reliably and get cheaper as they scale. The dollar figure tells you investors are starting to take the physical world seriously again.”

Philip Schröder, who left the European battery startup Sonnen to run Tesla’s Germany and Austria business, told us that after he rejoined his former company, the European battery startup, they were able to raise “one of the largest cleantech financing rounds in Europe.”

It’s not just raising money where a SpaceX or Tesla pedigree helps. Many former employees of the two companies left with enough of a financial cushion to take a risk on something new. When asked how being part of SpaceX helped him found his own company, John Bucknell, who worked on the Raptor rocket engine at SpaceX, said that having worked for Musk gave him the “financial freedom” necessary to start a company — in his case Virtus Solis, which is developing solar power in space.

But it also doesn’t hurt when raising money to put a SpaceX or Tesla logo on a slide deck, considering the size of returns they’ve generated for their backers.

Former Tesla employees have started and run some of the buzziest and best funded battery, transportation, and electrical infrastructure companies in the world. These include Lucid Motors, led until recently by former Tesla VP of vehicle engineering Peter Rawlinson, battery recycling company Redwood Materials, founded by former Tesla chief technical officer J.B. Straubel, and Heron Power, founded by Drew Baglino, who worked at Tesla from 2006 to 2024, ending his career there leading its powertrain and energy divisions.

When asked how their current work was connected to their past work for Musk or what they had learned, the founders and executives we surveyed — especially the SpaceX alumni — focused more on management and engineering principles than anything specific to energy or transportation.

“You can get way more done in a day and can move way faster than you think,” Justin Lopas, the co-founder of the home battery company Base Power, and a former manufacturing engineer at SpaceX, told us of what he’d learned from Musk.

Musk’s legendary short deadlines (which he says he only expects to hit about half the time) came up frequently among the group. Describing his time at Tesla, Arch Rao, the founder and chief executive of the smart electric panel company Span and a former head of products at Tesla Energy, told us, “The milestones to hit were incredibly audacious, but with the right group of people, possible. This has been a key model for how Span has scaled from the very early days to today.”

Jonathan Criss, the co-founder and chief executive of the desalination company Vital Lyfe, who worked at SpaceX for over a decade on both the Dragon spacecraft and the satellite communications service Starlink, told us that the rocket company had a unique “building for rate” philosophy, where engineers work backwards from a specific production goal, as opposed to first designing a product and then figuring out how to manufacture it as cheaply as possible. “That capability lets us design and manufacture highly reliable products at a fraction of the cost of most of the industry,” Criss said.

Investors, too, recognize SpaceX and Tesla alumni’s ability to work fast. Schroepfer, of Gigascale Capital, told us that speed sets these founders apart. “They know physical products can take years to get from first unit to cost-competitive scale. Even with a long timeline, they move with urgency,” he said. “They get how iteration and cost-down curves only work if you move fast, learn fast, and scale deliberately.”

Several founders also talked about learning to challenge assumptions. “At Tesla, there was a strong culture of questioning established ways of doing things,” Enric Asuncion, the co-founder and CEO of the EV charging company Wallbox who worked as a program manager for vehicle charging at Tesla, told us. Austin Spiegel, the co-founder and CEO of the infrastructure management software company Sift and a former software engineer at SpaceX, said that his former employer never accepted that something was good enough just because it existed. “Instead of buying off-the-shelf software, they asked, what would this look like if we designed it for a company that's going to launch and land rockets for the first time? That stuck with me.”

A former product engineer for Tesla’s Powerwall battery business, Cole Ashman, gave another example. He described how, for years, enabling a home to island from the power grid during a blackout required a labor-intensive, expensive electrical job. Tesla engineered a backup switch that was quicker and easier to install, but it required utility cooperation. “Conventional wisdom said it would never get broad approval,” Ashman, who founded the battery startup Pila, told us. “Tesla did the unglamorous work of bringing utilities along and moving the codes and standards — and pulled the whole industry forward.”

The other management concept that came up frequently was “ownership,” the idea of devolving responsibility down to engineers who were directly responsible for the projects they were working on. Working at SpaceX “taught me how to run a challenging hardware development program: how to choose and organize engineers around a tough unsolved problem, and give each of them real ownership from concept to mission success,” Colin Ho, founder and chief technology officer at the electrolyzer company Hgen, told us.

Frank Tybor, the chief technology officer at Infravision, the drone grid maintenance company and a former launch engineer at SpaceX, told us that “one of the things that made SpaceX special was the concentration of exceptionally talented people who were willing to take ownership of difficult problems and work across traditional organizational boundaries to solve them.”

Andreessen has endorsed the description of Musk-run companies and SpaceX specifically as a “zone of shocking competence” that attracts the best engineers, which its alumni founders have tried to recreate. Justin Cohen, the founder and CEO of Maritime Fusion who did stints at both Tesla and SpaceX, told us the talent network was “analogous to SEAL Team 6 of engineering; there is no better on earth.”

Several mentioned the Musk alumni network as a recruitment resource for their own businesses. “Tesla has cultivated a highly passionate ecosystem of engineers and tech developers,” Rao, the Span founder, told us. “My experience at Tesla helped me quickly identify what a skillful talent pool looks like and expect rapid and ambitious development from them.”

Brad Hartwig, a former SpaceX manufacturing engineer and founder and chief executive of Arbor Energy told us that “several early Arbor employees came from SpaceX, and that shared experience helped us build a world-class engineering team quickly. Many of us have worked on complex, high-stakes technology; we’ve already proven that we can execute in demanding environments, which helps when building a hard-tech company from scratch.”

When asked to name specific, non-Musk employees that influenced them, one name came up more than another: J.B. Straubel, the former Tesla chief technology officer and founder of Redwood Materials.

“Straubel is easily one of the smartest yet incredibly humble engineers and leaders I’ve had the opportunity to work with,” Rao told us.

Straubel, along with Heron Power’s Drew Baglino, “were both influential in how they helped solve complex problems within the company while dealing with constant pressure on cash & company survival,” Kunal Girotra, former Tesla Energy chief and founder of the battery company Lunar Energy, told us.

Jaramillo, the Form Energy founder, also singled out Straubel and Baglino, saying, “They’re very different people from each other, but both technically world class, with incredibly high standards. They drove that mindset into their teams from an engineering perspective — to never compromise on those standards.” About Straubel specifically, Jaramillo said that he had an “amazingly calibrated impatience, to know precisely when enough study is done, to just push start and get going in the physical world, and accept that you're going to learn things along the way.”

While Musk and his legions of former employees have helped turn hard tech and climate tech into an investible sector for venture capitalists, the amount of money the companies we’ve looked at have raised — about $30 billion — pales in comparison to the hottest sector, artificial intelligence. Even SpaceX, the signature hard tech company of its era, is itself running a massive “neo-cloud” business, renting out data center capacity to companies like Anthropic and Google to the tune of around $2 billion a month.

That being said, Tesla and SpaceX, which together are worth around $3 trillion, will continue to produce engineers and managers with sizable net worths and resumes uniquely looked favorably on by investors.

More than 4,000 current and former SpaceX employees are expected to become instant millionaires after the IPO, with 400 potentially getting at least $100 million, generating a wave of wealth that can give potential founders the cushion necessary to found their own company — or the capital necessary to become investors themselves.

“I think this is the emergence of a hardware mafia,” Schroepfer told us. “The PayPal mafia helped define an era of software and internet companies. This group will probably define an era where the center of gravity moves back toward atoms: energy, industry, mobility, infrastructure, manufacturing, and the physical systems that modern life depends on.”

Editor’s note: This story has been updated to correct the description of Arbor Energy.