All summer, as the repeal of wind and solar tax credits and the surging power demands of data centers captured the spotlight, a more obscure but equally significant clean energy fight was unfolding in the background. Sustainability executives, academics, and carbon accounting experts have been sparring for months over how businesses should measure their electricity emissions.

The outcome could be just as consequential for shaping renewable energy markets and cleaning up the power grid as the aforementioned subsidies — perhaps even more so because those subsidies are going away. It will influence where and how — and potentially even whether — companies continue to voluntarily invest in clean energy. It has pitted tech heavyweights like Google and Microsoft against peers Meta and Amazon, all of which are racing each other to power their artificial intelligence operations without abandoning their sustainability commitments. And it could affect the pace of emissions reductions for decades to come.

In essence, the fight is over how to appraise the climate benefits of companies’ clean power purchases. The arena is the Greenhouse Gas Protocol, a nonprofit that creates voluntary emissions reporting standards. Companies use these standards to calculate emissions from their direct operations, from the electricity and gas that powers and heats their buildings, and from their supply chains. If you’ve ever seen a brand claim it “runs on 100% renewable energy,” that statement is likely backed by a Greenhouse Gas Protocol-sanctioned methodology.

For years, however, critics have poked holes in the group’s accounting rules and assumptions, charging it with enabling greenwashing. In response, the organization has decided to overhaul its standards, including for how companies should measure their electricity footprint, known as “scope 2” emissions.

The Greenhouse Gas Protocol first convened a technical working group to revise its Scope 2 Standard last September. By late June, the group had finalized a draft proposal with more rigorous criteria for clean energy claims, despite intense pushback on the underlying direction from companies and clean energy groups.

A flurry of op-eds, essays, and LinkedIn posts accused the working group of being on the “wrong track,” and called the proposal a “disaster” with “unintended consequences.” The Clean Energy Buyers Association, a trade group, penned a letter saying it was “inefficient and infeasible for most buyers and may curtail ambitious global climate action.” Similarly, the American Council on Renewable Energy warned that the plan “could unintentionally chill investment and growth in the clean energy sector.”

Next the draft will face a 60-day public consultation period that begins in early October. “There’ll be pushback from every direction,” Matthew Brander, a professor of carbon accounting at the University of Edinburgh and a member of the Scope 2 Working Group, told me. Ultimately, it will be up to the Working Group, the Protocol’s Independent Standards Board, and its Steering Committee, to decide whether the proposal will be adopted or significantly revised.

The challenge of creating a defensible standard begins with the fundamental physics of electricity. On the power grid, electrons from coal- and natural gas-fired power plants intermingle with those from wind and solar farms. There’s no way for companies hooking up to the grid to choose which electrons get delivered to their doors or opt out of certain resources. So if they want to reduce their carbon footprints, they can either decrease their energy consumption — by making their operations more efficient, say, or installing on-site solar panels — or they can turn to financial instruments such as renewable energy certificates, or RECs.

In general, a REC certifies that one megawatt-hour of clean power was generated, at some point, somewhere. The current Scope 2 Standard treats all RECs as interchangeable, but in reality, some RECs are far more effective than others at reducing emissions. The question now is how to improve the standard to account for these differences.

“There is no absolute truth,” Wilson Ricks, an engineering postdoctoral researcher at Princeton University and working group member, told me back in June. “I mean, there are more or less absolute truths about things like how much emissions are going into the atmosphere. But the system for how companies report a certain number, and what they’re able to claim about that number, is ultimately up to us.”

The current standard, finalized in 2015, instructs companies to report two numbers for their scope 2 emissions, based on two different methodologies. The formula for the first is straightforward: multiply the amount of electricity your facilities consume in a given year by the average emissions produced by the local power grids where you operate. This “location-based” number is a decent approximation of the carbon emitted as a result of the company’s actual energy use.

If the company buys RECs or similar market-based instruments, it can also calculate its “market-based” emissions. Under the 2015 standard, if a company consumed 100 megawatt-hours in a year and bought 100 megawatt-hours’ worth of certificates from a solar farm, it could report that its scope 2 emissions, under the market-based method, were zero. This is what enables companies to claim they “run on 100% renewable energy.”

RECs are fundamentally different from carbon offsets, in that they do not certify that any specific amount of emissions has been prevented. They can cut carbon indirectly by creating an additional revenue stream for renewable energy projects. But when a company buys RECs from a solar project in California, where the grid is saturated with solar, it will do less to reduce emissions than if it bought RECs from a solar project in Wyoming, where the grid is still largely powered by coal, or from a battery storage project in California, which can produce clean power at night.

There are other ways RECs can vary — for instance, companies can buy them directly from power producers by means of a long-term contract, or as one-off purchases on the spot market. Spot market REC purchases are generally less effective at displacing fossil fuels because they’re more likely to come from pre-existing wind and solar farms — sometimes ones that have been operating for years and would continue with or without REC sales. Long-term contracts, by contrast, can help get new clean energy projects financed because the guaranteed revenue helps developers secure financing. (There are exceptions to these rules, but these are broadly the dynamics.)

All this is to say that the current standard allows for two companies that consumed the same amount of power and bought the same number of RECs to report that they have “zero emissions,” even if one helped reduce emissions by a lot and the other did little to nothing. Almost everyone agrees the situation can be improved. The question is how.

The proposal set for public comment next month introduces more granularity to the rules around RECs. Instead of tallying up annual aggregate energy use, companies would have to tally it up by hour and location. To lower companies' scope 2 footprints further, purchased RECs will have to be generated within the same grid region as the company’s operations, and match a distinct hour of consumption. (This “hourly matching” approach may sound familiar to anyone who followed the fight over the green hydrogen tax credit rules.)

Proponents see this as a way to make companies’ claims more credible — businesses would no longer be able to say they were using solar power at night, or wind power generated in Texas to supply a factory in Maine. While companies would still not be literally consuming the power from the RECs they buy, it would at least be theoretically possible that they could be. “It’s really, in my view, taking how we do electricity accounting back to some fundamentals of how the power system itself works,” Killian Daly, executive director of the nonprofit EnergyTag, which advocates for hourly matching, told me.

The granularity camp also argues that these rules create better incentives. Today, companies mostly buy solar RECs because they’re cheap and abundant. But solar alone can’t get us to zero emissions electricity, Ricks told me. Hourly matching will force companies to consider signing contracts with energy storage and geothermal projects, for example, or reducing their energy use during times when there’s less clean energy available. “It incentivizes the actions and investments in the technologies and business practices that will be needed to actually finish the job of decarbonizing grids,” he said.

While the standard is technically voluntary, companies that object to the revision will likely be stuck with it, as governments in California and Europe have started to integrate the Greenhouse Gas Protocol’s methodologies into their mandatory corporate disclosure rules.

The proposal’s critics, however, contend that time and location matching will be so costly and difficult to implement that it may lead companies to simply stop buying clean energy. One analysis by the electricity data science nonprofit WattTime found that the draft revision could increase emissions compared to the status quo if it causes a decline in corporate clean power procurement. “We’re looking at a potentially really catastrophic failure of the renewable energy market,” Gavin McCormick, the co-founder and executive director of WattTime, told me.

Another concern is that companies with operations in multiple regions could shift from signing long-term contracts for RECs, often called power purchase agreements, to relying on the spot market. These contracts must be large to be beneficial for developers because negotiating multiple offtake agreements for a single renewable energy project increases costs and risk. Such deals may still make sense for big energy users like data centers, but a company like Starbucks, with cafes throughout the country, will have to start sourcing fewer RECs in more places to cover all the parts of the world where they operate.

The granularity fans assert that their proposal will not be as challenging or expensive as critics claim — and regardless, they argue, real decarbonization is difficult. It should be hard for companies to make bold claims like saying they are 100% clean, Daly told me. “We need to get to a place where companies can be celebrated for being like, I’m not 100% matched, but I will be in five years,” he said.

The proposal does include carve-outs allowing smaller companies to continue to use annual matching and for legacy clean energy contracts, even if they don’t meet hourly or location requirements. But critics like McCormick argue that the whole point of revising the standard is to help catalyze greater emission reductions. Less participation in the market would hurt that goal — but more than that, these accounting rules aren’t designed to measure emissions, let alone maximize real-world emission reductions. You could still have one company that spends the time and money to invest in scarce resources at odd hours and achieves 60% clean power, while another achieves the same proportion by continuing to buy abundant solar RECs. Both would still get to claim the same sustainability laurels.

The biggest corporate defender of time and location matching is Google. On the other side are tech giants Meta and Amazon, among others, arguing for an approach more explicitly focused on emissions. They want the Greenhouse Gas Protocol to endorse a different accounting scheme that measures the fossil fuel emissions displaced by a given clean energy purchase and allows companies to subtract that amount from their total scope 2 footprint — much more akin to the way carbon offsets work.

If done right, this method would recognize the difference between a solar REC in California and one in Wyoming. It would give companies more flexibility, potentially deploying capital to less developed parts of the world that need help to decarbonize. It could also, eventually, encourage investment in less mature and therefore more expensive resources, like energy storage and geothermal — although perhaps not until there’s solar panels on every corner of the globe.

This idea, too, is risky. Calculating the real-world emissions impact of a REC, which the scope 2 working group calls “consequential accounting” is an exercise in counterfactuals. It requires making assumptions about what the world would have looked like if the REC hadn’t been purchased, both in the near term and long term. Would the clean energy have been generated anyway?

McCormick, who is a proponent of this emissions-focused approach, argues that it’s possible to measure the counterfactual in the electricity market with greater certainty than with something like forestry carbon offsets. With electricity, he told me, “there's five minute-level data for almost every power plant in the world, as opposed to forests. If you're lucky, you measure some forests, once a year. It's like a factor of 10,000 times more data, so all the models are more accurate.”

Some granularity proponents, including Ricks, agree that consequential accounting is valuable and could have a place in corporate reporting, but worry that it’s ripe for abuse. “At the end of the day, you can't ever verify whether the system you're using to assign a given company a given number is right, because you can't observe that counterfactual world,” he said. “We need to be very cautious about how it’s designed, and also how companies actually report what they’re doing and what level of confidence is communicated.”

Both proposals are flawed, and both have potential to allow at least some companies to claim progress on paper while having little real-world impact. In some ways, the disagreement is more philosophical than scientific. What should this standard be trying to achieve? Should it be steering corporate dollars into clean energy, accuracy of claims be damned? Or should it be protecting companies from accusations of greenwashing? What impacts do we care about more, faster emissions reductions or strategic decarbonization?

“They’re actually not opposing views,” McCormick told me. “There’s these people making this point and there’s these people making this point. They’re running into each other, but they’re actually not saying opposite things.”

To Michael Gillenwater, executive director of the Greenhouse Gas Management Institute, a carbon accounting research and training nonprofit, people are attempting to hide policy questions within the logic and principles of accounting. “We’re asking the emissions inventories to do too much — to do more than they can — and therefore we end up with a mess,” he told me. Corporate disclosures serve many different purposes — helping investors assess risk, informing a company’s internal target setting and performance tracking, creating transparency for consumers. “A corporate inventory might be one little piece of that puzzle,” he said.

Gillenwater is among those that think the working group’s time- and location-matching proposal would stifle corporate investment in clean energy when the goal should be to foster it. But his preferred solution is to forget trying to come up with a single metric and to encourage companies to make multiple disclosures. Companies could publish their location-based greenhouse gas inventory and then use market-based accounting to make a separate “mitigation intervention statement.” To sum it up, Gillenwater said, “keep the emissions inventory clean.”

The risk there is that the public — or indeed anyone not deeply versed in these nuances — will not understand the difference. That’s why Brander, the Edinburgh professor, argues that regardless of how it all shakes out, the Greenhouse Gas Protocol itself needs to provide more explicit guidance on what these numbers mean and how companies are allowed to talk about them.

“At the moment, the current proposals don’t include any text on how to interpret the numbers,” he said. “It’s almost incredible, really, for an accounting standard to say, here’s a number, but we’re not going to tell you how to interpret it. It’s really problematic.”

All this pushback may prompt changes. After the upcoming comment period closes in late November or early December, the working group could decide to revise the proposal and send it out for public consultation again. The entire revision process isn’t estimated to be completed until the end of 2027 at the earliest.

With wind and solar tax credits scheduled to sunset around then, voluntary action by companies will take on even greater importance in shaping the clean energy transition. While in theory, the Greenhouse Gas Protocol solely develops accounting rules and does not force companies to take any particular action, it’s undeniable that its decisions will set the stage for the next chapter of decarbonization. That chapter could either be about solving for round-the-clock clean power, or just trying to keep corporate clean energy investment flowing and growing, hopefully with higher integrity.

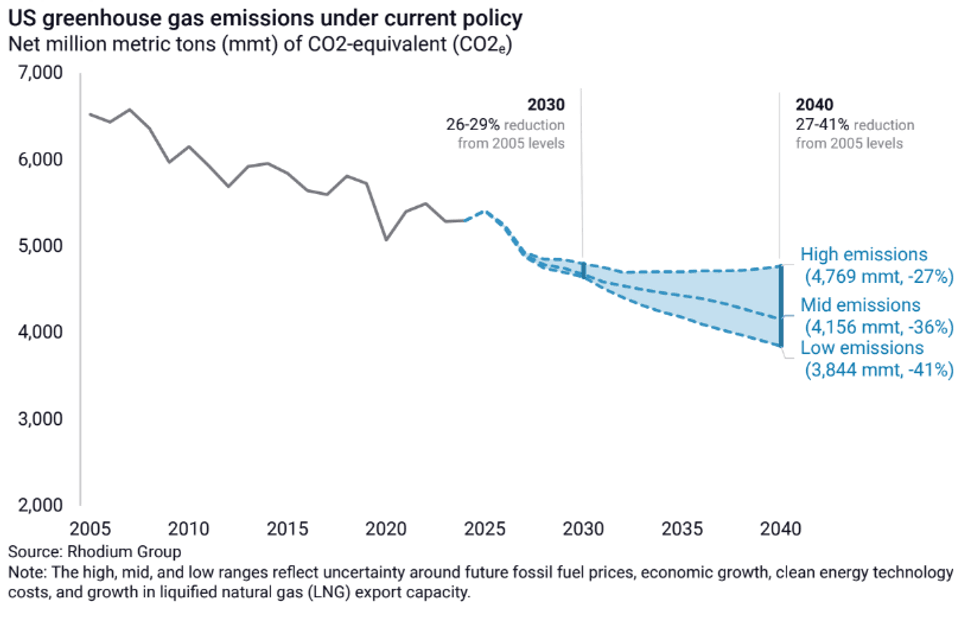

The 2030s crossroads.Rhodium Group

The 2030s crossroads.Rhodium Group