Current conditions: The remnants of Tropical Storm Chantal will bring heavy rain and potential flash floods to the Carolinas, southeastern Virginia, and southern Delaware through Monday night • Two people are dead and 300 injured after Typhoon Danas hit Taiwan • Life-threatening rainfall is expected to last through Monday in Central Texas.

THE TOP FIVE

1. Death toll in Central Texas floods climbs to 82, with more than 40 still missing

Jim Vondruska/Getty Images

Jim Vondruska/Getty Images

The flash floods in Central Texas are expected to become one of the deadliest such events in the past 100 years, with authorities updating the death toll to 82 people on Sunday night. Another 41 people are still missing after the storms, which began Thursday night and raised the Guadalupe River some 26 feet in less than an hour, providing little chance for holiday weekend campers and RVers to escape.

Although it’s far too soon to definitively attribute the disaster to climate change, a warmer atmosphere is capable of holding more moisture and producing heavy bursts of life-threatening rainfall. Disasters like the one in Texas are one of the “hardest things to predict that’s becoming worse faster than almost anything else in a warming climate, and it’s at a moment where we’re defunding the ability of meteorologists and emergency managers to coordinate,” Daniel Swain of the University of California Agriculture and Natural Resources told the Los Angeles Times. Meteorologists who spoke to Wired argued that the National Weather Service “accurately predicted the risk of flooding in Texas and could not have foreseen the extreme severity of the storm” ahead of the event, while The New York Times noted that staffing shortages at the agency following President Trump’s layoffs potentially resulted in “the loss of experienced people who would typically have helped communicate with local authorities in the hours after flash flood warnings were issued overnight.”

2. Trump to send up to 15 tariff letters to trade partners on Monday

President Trump announced this weekend that his administration plans to send up to 15 letters on Monday to important trade partners detailing their tariff rates. Though Trump didn’t specify which countries would receive such letters or what the rates could be, he said the tariffs would go into effect on August 1 — an extension from the administration’s 90-day pause through July 9 — and range “from maybe 60% or 70% tariffs to 10% and 20% tariffs.” Treasury Secretary Scott Bessent added on CNN on Sunday that the administration would subsequently send an additional round of letters to 100 less significant trade partners, warning them that “if you don’t move things along” with trade negotiations, “then on August 1, you will boomerang back to your April 2 tariff level.” Trump’s proposed tariffs have already rattled industries as diverse as steel and aluminum, oil, plastics, agriculture, and bicycles, as we’ve covered extensively here at Heatmap. Trump’s weekend announcement also sent jitters through global markets on Monday morning.

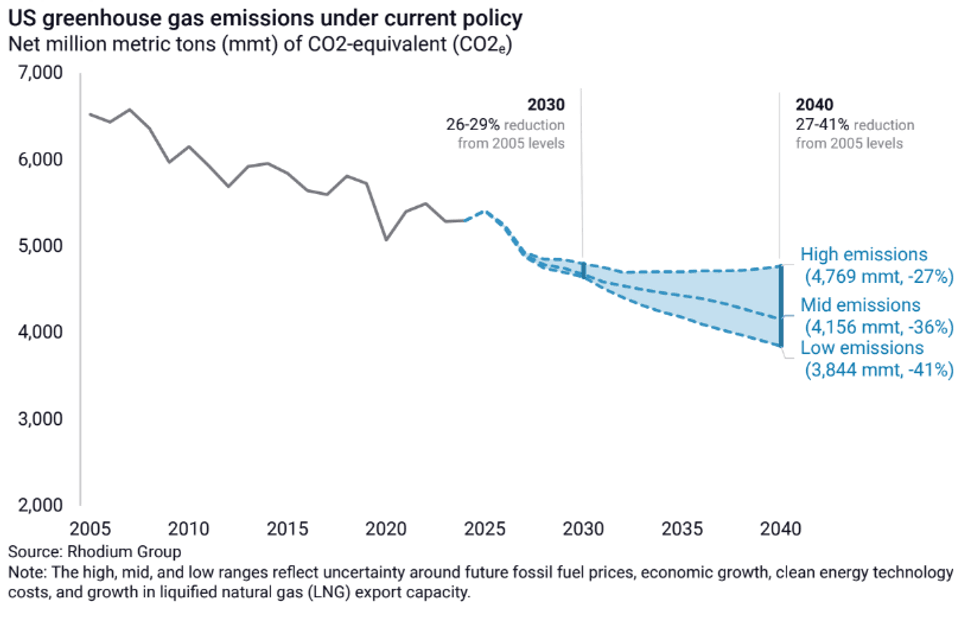

3. Trump’s big, beautiful bill will add an extra 7 billion tons of emissions by 2030: analysis

President Trump’s gutting of the Inflation Reduction Act with the signing of the budget reconciliation bill last week will add an extra 7 billion tons of emissions to the atmosphere by 2030, a new analysis by Climate Brief has found. The rollback on renewable energy credits and policy means that “U.S. emissions are now set to drop to just 3% below current levels by 2030 — effectively flatlining — rather than falling 40% as required to hit the now-defunct [Paris Agreement] target,” Carbon Brief notes. As a result, the U.S. will be about 2 billion tons short of its emissions goal by 2030, adding an emissions equivalent of “roughly the annual output of Indonesia, the world’s sixth-largest emitter.”

To reach its conclusions, Carbon Brief utilized modeling by Princeton University’s REPEAT Project, which examined how the current obstacles facing U.S. wind and solar energy will impact U.S. emissions targets, as well as the likely slowdown in electric vehicle sales and energy efficiency upgrades due to the removal of subsidies. “Under this new set of U.S. policies, emissions are only expected to be 20% lower than 2005 levels by 2030,” Carbon Brief writes.

4. SKF announces ‘world record’ for tidal turbine reliability

Engineering giant SKF announced late last week that it had set a new world record for tidal turbine reliability, with its systems in northern Scotland having operated continuously for over six years at 1.5 megawatts “without the need for unplanned or disruptive maintenance.” The news represents a significant milestone for the technology since “harsh conditions, high maintenance, and technical challenges” have traditionally made tidal systems difficult to implement in the real world, Interesting Engineering notes. The pilot program, MayGen, is operated by SAE Renewables and aims, as its next step, to begin deploying 3-megawatt powertrains for 30 turbines across Scotland, France, and Japan starting next year.

5. Ocean current in Southern Hemisphere reverses, could result in ‘unprecedented global climate impacts’

Satellites monitoring the Southern Ocean have detected for the first time a collapse and reversal of a major current in the Atlantic Meridional Overturning Circulation. “This is an unprecedented observation and a potential game-changer,” said physicist Marilena Oltmanns, the lead author of a paper on the finding, adding that the changes could “alter the Southern Ocean’s capacity to sequester heat and carbon.”

A breakthrough in satellite ocean observation technology enabled scientists to recognize that, since 2016, the Southern Ocean has become saltier, even as Antarctic sea ice has melted at a rate comparable to the loss of Greenland’s ice. The two factors have altered the Southern Ocean’s properties like “we’ve never seen before,” Antonio Turiel, a co-author of the study, explained. “While the world is debating the potential collapse of the AMOC in the North Atlantic, we’re seeing that the Southern Ocean is drastically changing, as sea ice coverage declines and the upper ocean is becoming saltier,” he went on. “This could have unprecedented global climate impacts.” Read more about the oceanic feedback loop and its potential global consequences at Science Daily, here.

THE KICKER

The French public research university Sciences Po will open the Paris Climate School in September 2026, making it the first school in Europe to offer a “degree in humanities and social sciences dedicated to ecological transition.” The first cohort will comprise 100 master’s students in an English-language program. “Faced with the ecological emergency, it is essential to train a new generation of leaders who can think and act differently,” said Laurence Tubiana, the dean of the Paris Climate School.

Jim Vondruska/Getty Images

Jim Vondruska/Getty Images

The 2030s crossroads.Rhodium Group

The 2030s crossroads.Rhodium Group