We cannot hope to halt or even slow dangerous climate change without remaking our energy systems, and we cannot remake our energy systems without environmentally damaging projects like lithium mines.

This is the perplexing paradox at the heart of Extraction: The Frontiers of Green Capitalism, a new book by political scientist and climate activist Thea Riofrancos, coming out September 23, from Norton.

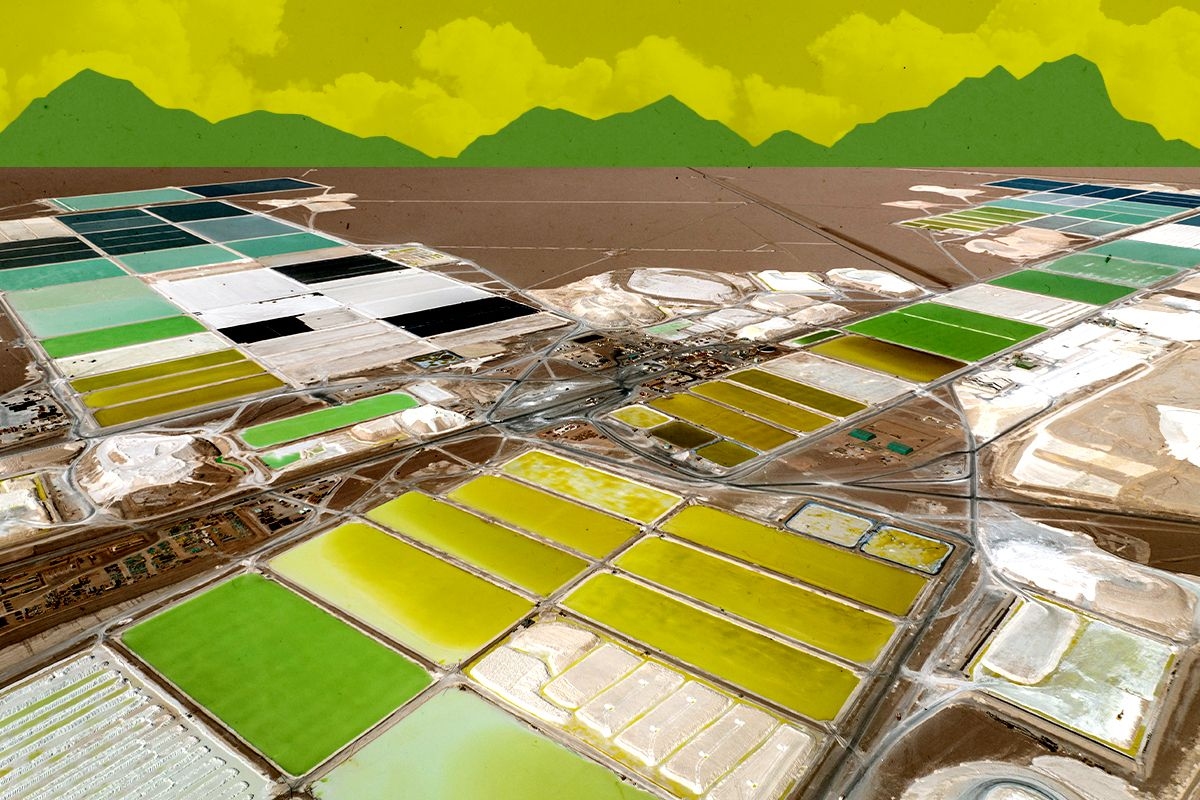

Riofrancos, a professor at Providence College, has spent much of her academic career studying mining and oil production in Latin America. In Extraction, she traces the lithium boom of the past five or so years, as the aims of the Global North and Global South began to resemble an inverted mirror. Countries in the latter group that have long been sites of mineral extraction — with little economic benefit — are now seeking to manufacture the more lucrative high tech products further down the supply chain. Meanwhile, after decades of offshoring, Europe and the U.S. suddenly want to bring mining back home in pursuit of “green dominance,” she writes. All of this is happening against the backdrop of China’s geopolitical rise, the war in Ukraine, the COVID-19 pandemic, and worsening effects of climate change.

The book also spends time with the indigenous communities and environmental defenders fighting the lithium industry in Chile, Portugal, and the American West. Riofrancos doesn’t shy away from difficult questions, such as whether there is such a thing as a “right place” for a lithium mine. But she’s optimistic that there’s a better path than the one we’re on now. “The energy transition has presented a fork in the road for the entire economic and social order,” she writes. Down one road, we entrench existing power structures. Down the other, we capitalize on the energy transition to create a more just society.

Green capitalism, Riofrancos argues, is an oxymoron. While we can’t avoid extraction, we can reduce the need for it, for example through better public transit, smaller EV batteries, and minerals recycling, she concludes.

This interview has been edited and condensed for length and clarity.

Are there notable differences between lithium and the extraction of other natural resources?

Yes and no. Whether it’s copper or lithium or gold or cobalt — and even I would include hydrocarbons in this, to a degree — whether we look at the economics, the way that they have boom and bust cycles, the fact that governments, even neoliberal governments, tend to take a pretty concerted interest in extractive sectors within their jurisdiction, environmental concerns and direct forms of violence that are meted out at environmental defenders — no, it’s not different. Which should raise alarm bells because a lot of those dynamics are not positive.

What’s different, though, is that precisely because mining companies and host governments claim that the extraction of lithium is urgent and essential for the energy transition, what ends up happening is that these big claims are made — like, “We are now a sustainable mining company because we’re extracting lithium,” or, “This is part of our green industrial policy.” This toxic and dirty extractive sector is now greenified because of its role in the energy transition. On the one hand, that’s greenwashing. On the other, it’s an opening. When companies make those claims, it’s something to hold them accountable to.

I was somewhat surprised by the issues you describe with the way lithium mining is regulated in Chile — the companies do their own environmental monitoring, there’s a lack of transparent data, the brine they mine in the Atacama is not considered water under Chilean law, etc. It seems like the state could change a lot of this. Why hasn’t it?

States in the Global South, although not exclusively there, lack geological and hydrological data about their own territory. In ways that we can trace to colonialism and neocolonialism in terms of who controls the territory and who has knowledge about it, the actors that have the basic data about deposits, how they interact with water sources, all of that, are the companies. And so to even regulate these companies better, you first need to set up independent and objective sources of data collection — and that’s something that any state might struggle with, but especially in the Global South, given the kind of legacy under which these companies operated, with little oversight of the state.

The [U.S. Geological Survey] doesn’t exist everywhere in the world. Not every state has a surveying agency with that level of expertise. And even in the U.S., the USGS actually has quite partial knowledge of what’s here. And there are many examples of companies in the U.S. hiding proprietary knowledge from the government.

What about after Gabriel Boric became president in Chile, in 2022, and created this new public-private partnership between the mining giant SQM and the government. Wouldn’t that have given the Chilean government more visibility and more control?

I think in some ways he’s made strides. He has set aside many salt flats for conservation. A right wing government wouldn’t have done that. He also is inserting the state, via the state-owned copper company Codelco, entering into public-private partnerships with companies, including SQM. If all goes according to plan, that will help the state learn more about lithium extraction, or maybe even set up their own lithium company, which was the initial goal of this government.

I’ll just point out two things to show how this is difficult. According to indigenous communities and environmental activists that have been organizing around this, they were excluded from the initial moment where that memorandum of understanding between SQM and Codelco was signed, and so they felt like it was a reenactment of historic injuries by a government that they had cautiously supported or thought would be different. Now they’re back at the negotiating table and indigenous communities are being consulted again. But there was a critical moment where the MOU was signed and indigenous communities were not present, and actually learned about it from the media. These historic patterns are really hard to change because companies hold a lot of power.

Even a progressive government is balancing indigenous rights and ecological protection with a desire to not lose market share. Argentina is starting to catch up with Chile — is Chile still going to remain the number two producer globally? Does it need to change its regulations to attract more companies? This is the kind of double bind that Global South societies find themselves in.

You write about this tension between expanding extraction and minimizing environmental and community impacts. Do you believe there are actually ways to minimize these impacts?

Absolutely. You can do anything better. I believe in human ingenuity and science and figuring out how to improve processes. There are ways to extract using less water, using a smaller land footprint, using fewer polluting energy sources. One of the reasons emissions from mining are not insignificant is a lot of it happens off-grid, and for now, that means diesel generators or gasoline-powered mining vehicles, let alone the cargo ships that are shipping the stuff around the world. So we could think about localizing or regionalizing supply chains.

The question is, how do we get companies to change their practices? They might do it if a regulator tells them they have to, if civil society puts so much pressure on them that it just becomes reputational harm if they don’t do it, if perhaps activist shareholders ask or tell the company to change its practices.

But the company, if it’s a shareholder-owned company, has one main obligation, which is to maximize the value of their shares. Changing your technological setup and your physical plant arrangement is costly, and it may not immediately produce more profits. And so you have to think about, what are the crude economic dynamics that keep companies on a particular technological path in terms of how they do their physical operations? And then think, using the power of policy, of economics, of consumer pressure, whatever it is, how to get them to make a decision that may not be in their immediate shareholder interest.

One theme in the book is that countries in the West are making a case for domestic mining by arguing that it will be greener than mining in the Global South. Is there any evidence for that? What’s the logic?

This was honestly one of the most surprising things in my research as someone that primarily has worked in Latin America. I heard some rumblings — and this was in 2019, before the pandemic — of EU officials wanting to onshore. It confused me because mining is toxic, it’s low value-added. And what I learned is that it had come to a point where Western policymakers saw the whole supply chain as a domain of geostrategic power.

And then, probably some people really feel this way, and other people are using it as nice rhetoric, but Western policymakers also started to come to the idea that it would be more “responsible” to mine in the West. This is in no small part due to the fact that the mining industry has deservedly gotten a lot of negative coverage for, in some cases, outright killing people. In other cases, you have an avalanche that destroys a village. You have water contamination. There are issues around forced labor, how the Uyghurs are treated in China. So there was a lot of bad press on the industry. I think they thought, We can solve a few problems at once. We can increase our geopolitical power by having domestic supply chains for the most important 21st century technologies, and we can also make the claim to consumers, regulators, and the media that this is better if you care about responsible, ethical, green mining.

The reality is, of course, more complex than that. Our mining law in the U.S. that governs hard rock mining on public lands is from 1872, which tells you everything you need to know. It’s extremely out of date with the modern mining industry and the scale of harm that mining poses, and it also literally was implemented during the westward expansion and dispossession of indigenous peoples to serve that end.

In fact, countries in Latin America tend to have better — on paper — governance of mining than the U.S., though they may not have the state capacity to always implement it. In Europe, there’s even more dependence on imports. A lot of the European countries have almost no regulations on the books for basic things like, how do you deal with mining waste? And so in the Global North, what we have to fight for is a mining governance regime and a set of legal codes and regulations that is up to date.

This book is pretty critical of the way communities have been treated in the lithium boom so far. What are some of the ways community engagement can be done better?

We see better outcomes when communities are organized, when they actually identify as a community, have some meetings, maybe set up a group to coordinate themselves. Like, who’s going to go to the public hearing? Who’s going to contact a lawyer? Who’s going to contact the water expert? Because communities need a lot of outside help. The companies have lawyers, they have experts, they probably have friends in government. A lot of lawyers and experts that companies hire used to work for the government, and they know these processes inside out, and so the community needs to be as or more organized. They’re already on the losing end of a power imbalance.

In a way, none of this is about what companies can do, because I presume that companies are responsive to pressure. Multinationals, insofar as they’re shareholder-owned, their main goal is to maximize value, and that’s it. It’s that simple. And so in order to get them to behave differently towards communities, outside forces need to take a role. The first outside force is the community itself. A second is, how involved is the government? And how objective and public-serving is the government? Where governments take a more objective role and help protect the baseline rights of communities, make sure that those rights are not being violated by companies, help distribute more culturally sensitive and appropriate information about the mine, we could get better outcomes that way.

You had activists tell you, “I support lithium mining, but this is the wrong place for it.” Do you think there is such a thing as a right or wrong place, or even a better or worse place for a lithium mine?

This was honestly the most vexing question that I had to contemplate in my own research. I often think about how these communities are called NIMBYs, and there’s two reasons that’s a really inappropriate term. First of all, the “my backyard” — not every person has private property, or that’s not their stake in the matter. It’s not about, this is going to decrease the value of my property, or this is going to disrupt my ocean view. It’s about the land that they have a deep relationship with.

The second thing is, I don’t think most of the people that call these communities NIMBYs would really want to live next to a large-scale mine, either. They are just enormous scars on the landscape. I understand that they are necessary, to some degree, to provide for the technologies that we enjoy, including life-saving and planet-saving technology. Even in my perfect world, where everyone is riding an electric bus or bike or walking around, some lithium is still needed in the near term. In the future, we could conceivably enter into a circular economy, but we don’t have the level of feedstock for that yet.

So the question remains, where are we going to mine? I don’t have an easy answer to that, but I will say that in the entire process of land use planning, the corporation is the protagonist. In the U.S., a place that I think most political scientists would say has more state capacity than a country in Africa or Latin America, we do not use that capacity to proactively plan land use. I think it would make sense to really rearrange the process such that governments plan with substantial community input, and then corporations, if we want to have private corporations doing this, get the ability to compete for contracts. I know that would be a big lift to change that policy dynamic, but I think we need to have the conversation.

You write a lot about this difficult dance between supply and demand in mining. What are you seeing right now in how the lithium industry is reacting to Trump’s dismantling of EV policy?

With Trump, it’s particularly interesting and bizarre because on the list of fast-tracked mines, you have several lithium mines and some lithium processing along with other “critical minerals.” He really wants to expand mining, to the point that the Pentagon is now the No. 1 investor in our only rare earth mine in the U.S. They bought 15% of MP Materials’ shares, the company that manages the Mountain Pass mine. And so Trump is fast-tracking mines, he’s sending huge amounts of public money to financially underwrite these mining companies. But yet, he’s destroying demand for rare earths. He loves to talk about AI and military tech — that’s a small slice of demand. It’s really about wind turbines and electric vehicle motors. That’s really where the demand is. With lithium, it’s even clearer.

That all seems like a recipe for prices to crash.

The thing is, they already had crashed because of a supply glut. But at the same time, the market will likely pick back up because we’re seeing so much action elsewhere in the world. It’s very easy to focus on the U.S., especially because the U.S. government is such a basket case right now. But if we zoom out, there’s been a bunch of recent reporting, including in Heatmap, on how rapidly the energy transition is going in other parts of the world, with China playing an enormous role not only on the trade side, but also in foreign direct investment, in setting up solar and EV manufacturing hubs in the Global South.

And so I think that Trump can dismantle EVs as much as he wants in the U.S., and that’s a shame given that transportation is our most polluting sector. I mean, that pains me as a climate activist. But the world is bigger than the U.S.

The last thing I’ll say — and this is another interesting contradiction — in the Big, Beautiful Bill, it’s not across the board against all green technologies. There’s this distinction that conservatives increasingly like to make called “clean, firm power.” So they put nuclear, geothermal, and battery storage in that. Now, battery storage, what is that made of? Lithium. So in a weird way, they like lithium mining, they like batteries for storage, they just don’t like electric vehicles. We’re still going to have lithium demand in the U.S., and lots of individual people will still buy electric cars, and blue states will still procure them for their public fleets. He’s not going to kill the market. He’s just going to slow its growth, primarily by making it less affordable for working and middle class people.

EPA Administrator Lee Zeldin. Kevin Lamarque-Pool/Getty Images

EPA Administrator Lee Zeldin. Kevin Lamarque-Pool/Getty Images