The Empire State took a big leap toward a carbon-free future this week.

Late Tuesday night, after more than a month of negotiations, the New York state legislature passed a $229 billion budget, enacting three major climate policies in the process. The legislation will not only give teeth to ambitious emissions targets the state established four years ago, but it also forms a sort of blueprint for state-level clean energy transitions around the country.

New York passed a law setting up targets to cut emissions across its economy back in 2019 when Andrew Cuomo was governor. But it didn’t stipulate how the state was supposed to achieve them. Instead, the law set in motion a multi-year process for state leaders and appointed advisors to work out the best path forward. The group’s findings were finally published in December, and two of the climate policies enacted this week — a ban on natural gas in new buildings and a cap-and-invest program — are key recommendations from that document. The third, which creates a new avenue for publicly-owned renewable energy projects, was not part of that plan, but was born out of a vigorous, four-year grassroots campaign by the Democratic Socialists of America.

New York’s budget deal won’t fill in all the gaps in its strategy to decarbonize. But it does accomplish a number of big and essential first steps, like limiting the growth of natural gas and developing sources of funding to pay for the transition. About half of the country has enacted greenhouse gas reduction targets, but few states have put in place the policies to achieve them.

Below, a look at New York’s three big climate moves and why they could be a model for other states looking to live up to their own climate goals.

1. The Gas Ban

Buildings are by far the largest contributor to climate change in New York, accounting for 32% of the state’s greenhouse gas emissions. They are also an exceedingly hard source to tackle, as those emissions come from a bunch of long-lived appliances like natural gas heating systems, stoves, and clothes dryers. But electric alternatives, which can be powered by renewable energy, are readily available. One easy first step any state can take is to stop the problem from getting worse by requiring that new buildings forego fossil fuels.

A few municipalities in the Empire State, like New York City and Ithaca, have already enacted bans on fossil fuel-burning appliances in new buildings. Now, Governor Kathy Hochul is set to pass a similar state-wide ban that will begin to go into effect in 2026. This is a year later than what was recommended by the state’s climate plan. But it will still send a powerful message that gas is no longer a growth industry in one of the biggest economies in the U.S.

“It is very, very clear now what the direction of travel is,” Pete Sikora, climate and inequality campaigns director of New York Communities for Change, a grassroots organization, told me. “That’s a monumental shift, as I see it, from an earlier environment, where Democrats were mouthing that ‘gas is a bridge fuel to the future.’ We’ve blown up that bridge. That bridge is collapsing into a ravine.”

While a few other states, like California and Washington, have effectively done the same thing via changes to their building codes, New York is the first state to build enough political support to cut off gas growth through its legislature. Jonny Kocher, a manager for the Carbon-Free Buildings Program at the clean energy group RMI, told me he anticipates that New York’s approach will have fewer exemptions than other states, and expects California and Washington to follow suit with legislation in order to strengthen their own policies. Washington State is currently facing a lawsuit for sidestepping the legislature.

Kocher said a gas ban isn’t necessarily a step that all states need to take in order to limit emissions from new buildings. The latest electric appliances, like heat pumps, are more efficient than gas-burning boilers or furnaces, and all-electric new construction will save consumers money in many parts of the country, so many states will move in this direction anyway. “We believe that states with existing (or new) energy efficiency goals will inevitably shift towards an all-electric code because it is simply the least expensive pathway to reach those energy efficiency goals,” he said in an email.

2. Funding the Transition

Implementation of New York’s climate plan has been somewhat piecemeal to date. Like many states, New York has a clean energy standard that requires utilities to buy an increasing amount of renewable energy each year. It also participates in a regional effort to cut emissions from power plants. That program raises some money for clean energy programs, like energy efficiency and electric vehicle rebates.

But while these policies are serving to clean up New York’s grid, they leave out other parts of the economy that also produce emissions, like fuel suppliers, natural gas utilities, and industrial facilities. The state has also failed to figure out how to pay for its energy transition, which is estimated to cost some $300 billion over the next 30 years. To address both of these gaps, Hochul announced in January that New York will establish a cap-and-invest program like those used by California and Washington State. The legislation passed this week fleshes out the “invest” side of the plan.

Cap-and-invest is similar to a price on carbon, and is often called a “polluter pays” program. Companies with big carbon footprints will have to purchase permits to pollute, and the number of permits available will shrink over time to ensure that the state hits its emissions targets.

These programs are complex and notoriously hard to implement well. Policy experts and environmental justice advocates have criticized California’s program for giving companies too much leeway to purchase carbon offsets instead of reducing their pollution, and for auctioning off more permits than needed.

Many of the details in New York have yet to be worked out. But the budget deal ensures that at least 30% of the proceeds raised by the program will be returned to New Yorkers to offset higher costs that may result from it. The rest will go into a climate action fund to pay for all kinds of clean energy projects and incentives.

3. Public Power

A growing number of climate advocates are starting to unite around a more radical vision for the transition to clean energy — a shift toward publicly-owned power. Some consider it a key tenet of the Green New Deal, others just see it as a way to bring more accountability to energy companies. Utilities have historically been some of the biggest obstructors of climate action. Proponents argue that publicly-owned utilities would be better equipped to usher in the energy transition since they aren’t beholden to shareholders and can prioritize clean energy and equity over profit.

“If you’re leaving it up to the market, you can create incentives, but you have less power over where this energy is sited, who is benefitting,” said Johanna Bozuwa, executive director of the Climate and Community project.

In New York, advocates discovered that they had a “sleeping giant” in the New York Power Authority. The state-owned utility operates several big hydroelectric dams and a number of fossil fuel power plants, but its ability to build and operate solar and wind projects was severely curtailed under statute. After a four year push, and the election of a slew of DSA candidates into the legislature, the public power movement successfully pressured Hochul into changing that.

The budget deal mandates strong labor standards for any new generation built and also instructs NYPA to retire its fossil fuel plants by 2030, five years earlier than previously planned.

It remains to be seen whether authorizing NYPA to build will actually result in it using that authority. But the odds are better than they were a year ago, thanks to the Inflation Reduction Act. The law made a key change to the country’s clean energy tax credits, allowing public institutions and nonprofits to claim them for the first time. Bozuwa told me that this means other states will be looking at what happens in New York and could follow its lead.

“Not every state has a NYPA, but I think that people will look to NYPA and say, ‘oh, my gosh, we could be doing that too,’” she said. “Because there’s so much money flowing in, this is the perfect time for states or even municipalities to start to develop a renewable energy generation fleet.”

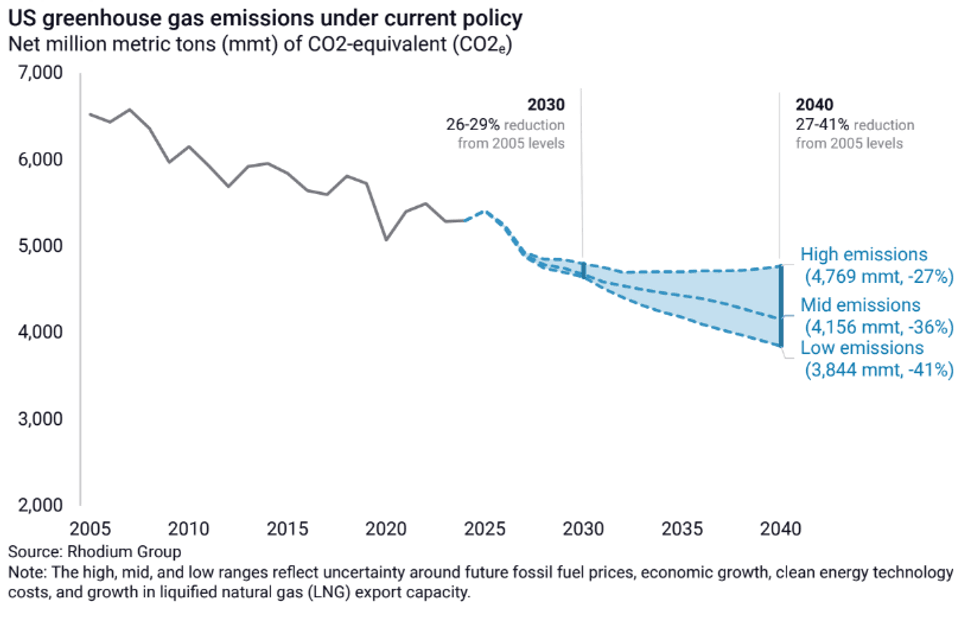

The 2030s crossroads.Rhodium Group

The 2030s crossroads.Rhodium Group