The largest hydrogen producer in the world, Air Products, stands to earn up to $440 million per year in clean energy tax credits once it opens its massive, $7 billion complex in Louisiana in 2028. But a recent report argues that while the hydrogen produced there will be highly profitable for Air Products, it’s a “lose-lose proposition” for the environment — and for taxpayers.

The research adds to the long-running debate around the climate benefits of “blue hydrogen,” which is produced via the separation of hydrogen molecules from carbon molecules in natural gas, with systems that capture the resulting carbon emissions and store them underground. Advocates of the technology say it’s a critical bridge to a renewables-powered hydrogen economy, as it allows for cleaner hydrogen production now by relying on existing infrastructure. Critics, however, say that blue hydrogen’s emissions benefits are minimal if any, and that a focus on this technology diverts money from more meaningful climate solutions.

The blue hydrogen produced at Air Products’ Louisiana facility will be eligible for the lucrative 45Q carbon sequestration tax credit, which was expanded by the Inflation Reduction Act in 2022 and provides up to $85 per metric ton of carbon that’s permanently locked away.

The March report from the Institute for Energy Economics and Financial Analysis, however, argues that Air Products makes overly optimistic assumptions about both methane leakage rates and the effectiveness of carbon capture equipment, while underestimating the potency of methane in the short term. The company’s estimates are largely based on a Department of Energy life cycle analysis tool, which the report's authors also believe is flawed. The result, the authors write, is that the Louisiana plant would “cost billions of dollars in subsidies for essentially zero environmental benefit.”

With lawmakers in Congress considering which IRA tax credits to preserve and which ones to cut to make way for Trump’s spending priorities, now is a critical moment for climate-focused policymakers to have their priorities in order. It’s worth asking which provisions from Biden’s signature climate law are actually delivering a climate bang for their buck.

Air Products says that its Louisiana facility will sequester 5 million metric tons of CO2 annually over the 12 years that it’s eligible for the tax credit, which equates to $6.3 billion in total tax savings. To state the obvious, that’s a lot of taxpayer money for a project that a leading research group asserts will likely be a net negative for the environment.

“As you start expanding the envelope to take into account the full footprint and the full impact of this project and its product, there’s just not much of a benefit there, if any. It may be making things worse.” Anika Juhn, an energy data analyst at IEEFA and one of the report’s authors, told me. These findings are not specific just to Air Products’ upcoming facility — they’re “broadly applicable to other blue hydrogen projects,” Juhn said. (My colleague Emily Pontecorvo, for instance, wrote about a similar finding regarding methane leakage from the Permian Basin.) At least four of the DOE’s seven hydrogen hubs rely on natural gas with carbon capture and storage to some degree. Meanwhile, the Trump administration is looking to cut funding for the hubs that primarily produce hydrogen via renewable energy.

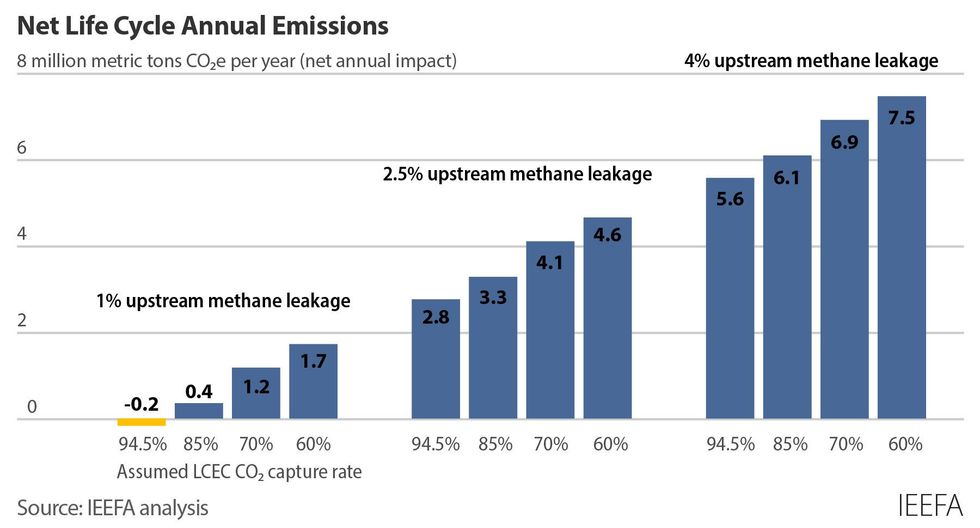

The DOE’s life cycle analysis tool uses an industrial methane leakage rate of 0.9% and a carbon capture rate of 94.5% for the specific method the Air Products facility will use, called autothermal reforming. (Or at least that’s what the IEEFA report said — I couldn’t find evidence of this carbon capture number in the government’s model itself.)

When Juhn and her co-author David Schlissel adjusted the analysis of Air Products’ Louisiana project using more typical industrial methane leakage rates of 1% to 4% and carbon capture rates ranging from 60% to 94.5%, they found that only under the most optimistic scenario would the project yield any carbon reductions at all. Even then, avoided emissions would only be about 200,000 metric tons per year of CO2 equivalent, whereas at the high end of the report’s “realistic scenario,” the project could result in an additional 7.5 million metric tons of CO2 equivalent annually.

Courtesy of IEEFA

Courtesy of IEEFA

To calculate the net life cycle emissions of a hydrogen project, the authors had to take the estimated benefits of hydrogen production into account, a task complicated by the fact that Air Products hasn’t announced any offtakers, making it impossible to know what dirtier (or cleaner) options customers might turn to if they didn’t have access to blue hydrogen. So instead, IEEFA relied on the White House’s general estimate that the 3 million metric tons of blue and green hydrogen (i.e. hydrogen released from water molecules using carbon-free electricity) produced by the hydrogen hubs would displace 25 million metric tons of CO2. But because the White House didn’t release its formula for determining avoided emissions, take their numbers with a grain of salt.

All of Air Products’ calculations thus come with the usual caveat, which is that they’re measured against an unknowable counterfactual — essentially a best guess at what would happen if plans for the Air Products facility went poof. Would the end users opt for hydrogen alternatives or would they rely on a standard natural gas-powered hydrogen facility with no carbon capture? Is it possible that a green hydrogen plant using renewables-powered electrolysis would be built instead?

All we know is that a portion of the hydrogen will be turned into ammonia and exported abroad, where Juhn told me it’s likely to be burned as fuel. Another portion will be injected into an existing 700-mile hydrogen pipeline on the Gulf Coast for use by existing customers in industries such as energy, transportation and chemicals.

While Air Products did not respond to my request for comment on the report, I was able to discuss the results with John Thompson, a director at the climate nonprofit Clean Air Task Force, which advocates for a wide array of climate-focused technologies, including hydrogen with carbon capture and storage. He took issue with the IEEFA study’s methodology, and told me that blue hydrogen projects have the potential to be a big win for the climate, so long as they’re replacing “gray” hydrogen projects — that is, those powered by natural gas with no carbon capture.

“When you do displace gray hydrogen, you get huge, huge benefits,” Thompson told me. Despite all the unknowns involved, he’s confident the Louisiana project will do just that, primarily due to the existing network of hydrogen pipelines at the site. “Those pipelines are there because they’re serving existing customers — refineries, ammonia plants, chemical manufacturing,” he said, meaning that “the likelihood that you’re displacing existing sources is pretty great.”

Thompson also took issue with the notion that a 95% capture rate is overly optimistic, telling me that there’s no technical barriers to achieving industrial capture rates in the 90s. “The 95% capture rate that they’re proposing to build towards is what is commercially guaranteed by many vendors,” Thompson said. “It hasn’t been widely used, not because it’s not commercially available, but because it’s costly, and there hasn’t been much demand for it until we got into climate considerations.”

To Thompson, the IEEFA report looked more like an “advocacy piece.” To IEEFA, the Louisiana project still appears to be a government subsidized money-making scheme. Notably, the Air Products facility probably will not qualify for the much debated 45V clean hydrogen production tax credit, the most generous subsidy of all in the IRA. That credit provides up to $3 per kilogram of clean hydrogen produced — a whopping $3,000 per metric ton — for projects with the lowest emissions intensity. It’s also tech-neutral, meaning that so long as blue hydrogen projects have life cycle emissions under 4 kilograms of carbon dioxide equivalent per kilogram of hydrogen produced, they will be eligible for at least a $0.60 credit per kilogram of clean hydrogen.

Air Products said last May that it would not even attempt to claim this credit for the Louisiana facility, even as the company asserts that the complex will produce “near-zero carbon emissions.” A 2023 DOE report indicated few blue hydrogen projects will be eligible, period, given “the added [natural gas] and electricity needed to run the [carbon capture and storage] facility.”

So at least by the DOE’s own standards, the hydrogen produced by Air Products will not be “clean.” That’s not a precondition for the carbon sequestration tax credit, though, which doesn’t demand life cycle analysis, just proof that you’re putting a certain amount of CO2 in the ground. Juhn thinks that’s a big mistake. These analyses are “the only way that you can know whether or not investing in CCS projects makes sense, either in a climate sense or in a financial sense,” she told me.

But as fossil fuel interests including Occidental and ExxonMobil have advocated for preserving and even increasing the 45Q tax credit, Juhn doesn’t expect to see any changes to the rule that would mandate more stringent requirements.

“I do hear the fossil fuel industry saying, Oh, we need blue hydrogen first because we can get things moving. We can get this online and we can start creating this product to stimulate demand,” she told me, citing a common argument that blue hydrogen is a necessary stepping stone to creating a robust, economical green hydrogen economy. “But the problem is that these facilities, they’re not going to go away when green hydrogen projects come online, and these projects are being built with a 25-, 30-year lifespan.”

At the very least, what everyone can agree on is the need to address upstream methane leakage. “It’s not enough to do carbon capture, I can’t emphasize that enough,” Thompson told me, pointing out that methane emissions are “not a law of thermodynamics” but rather “a variable that we can control if we choose to.” Unfortunately, it looks like the Trump administration won’t be choosing to, as the president recently signed legislation scrapping a Biden-era rule that imposed fees on oil and gas producers who emit excess methane.

Courtesy of IEEFA

Courtesy of IEEFA