The ban is good news for America’s beleaguered solar manufacturing industry, which the Trump administration has championed with tariffs but hobbled by axing key federal tax credits that included bonuses for projects using domestically produced panels. T1 Energy, shares of which nosedived this week after the latest quarterly earnings showed losses far outpacing revenue, just spent another $135 million on patents from a rival in Singapore in a bid to vertically integrate production of a more efficient type of photovoltaic technology. Tesla, meanwhile, is promising to “multiply” American solar production by “an order of magnitude.” Yet Elon Musk’s behemoth is cutting long-term deals to buy other people’s solar power. The company just inked an agreement with a KKR-backed solar and battery project in Arizona to buy 90% of its output.

2. Electricity demand is on track to keep growing for the next 15 years

The 2030s crossroads.Rhodium Group

The 2030s crossroads.Rhodium Group

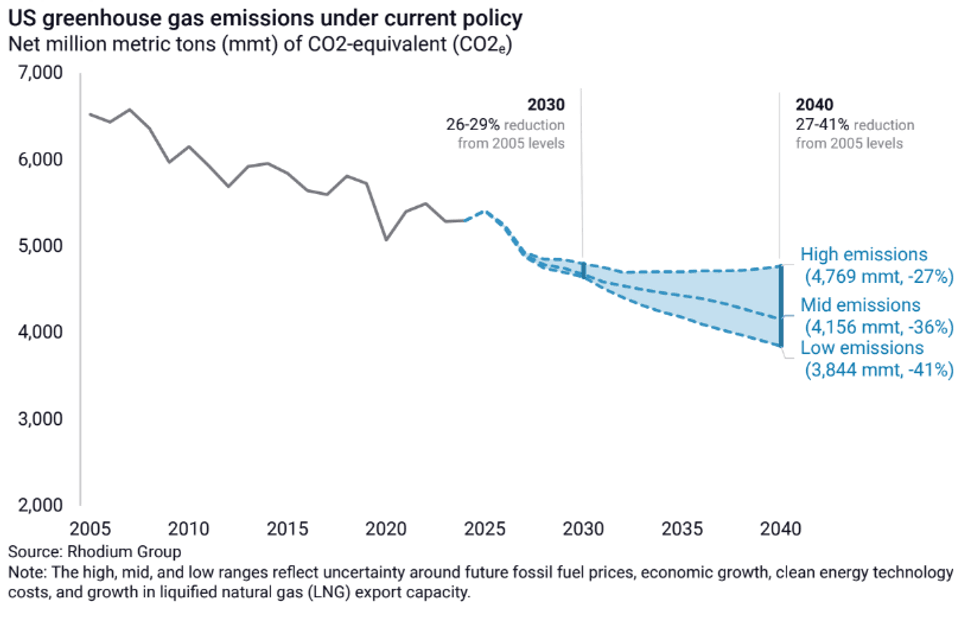

Reasonable people debate just how much electricity is needed to satisfy the demands of the data center boom — and the bears are likely to get a boost amid this week’s selloff of AI stocks. But the latest projections from the Rhodium Group forecast U.S. electricity demand growth to accelerate over the next 15 years, “growing faster than it has since the turn of the century.” Data centers will account for between 62% and 77% of the growth in 2030, and between 59% and 66% in 2040, ultimately reaching 17% of total electricity demand that year. Electric vehicles will make up the second-largest source of new demand growth in the low- and mid-emissions scenarios the consultancy outlined through 2040. In the high-emissions scenario, heavy industry will account for a quarter of the demand growth between 2025 and 2040. Overall, the findings show divergent pathways in the 2030s. By 2040, the U.S. will either reduce its greenhouse gas emissions by 41% below 2005 levels — or just 27%. Across all three scenarios, the “historic influx of renewables” coming online between now and 2030 keeps emissions declining. After 2030, however, the grid’s trajectory either continues to deploy nearly 53 gigawatts of renewables per year through 2040 in a low-emissions scenario or drops to 3 gigawatts per year in a high-emissions scenario where cheap natural gas dominates.

For months now, the Greenhouse Gas Protocol, the nonprofit behind a voluntary but widely used corporate standard for carbon accounting rules, has been revising its approach. Last year, my colleague Emily Pontecorvo explained the stakes of the revision process as an “obscure philosophical battle that could reshape the clean energy economy. In April, she broke news from whistleblowers that the changes underway were drumming up controversy. This morning she’s out with a new story on Greenhouse Gas Protocol’s plans to marry its standard to those by the International Organization for Standardization. The short of it is this: the changes are getting a lot of pushback, and credibility of the forthcoming new standard remains an open question.

Sign up to receive Heatmap AM in your inbox every morning:

3. Five states step up to take nuclear waste

For decades, the U.S. plan to deal with nuclear waste has focused on building a highly controversial repository in the Nevada desert. But that effort, as I explained yesterday, was put on indefinite hiatus in 2010 when the Obama administration canceled funding on behalf of then-Senate Majority Leader Harry Reid, a Nevada Democrat. In the meantime, states such as Texas and New Mexico have demonstrated that both Republican and Democratic governments are still willing to fight efforts to build intermediate-term storage facilities for nuclear waste in their states. On Tuesday, five states officially stepped up and made bids to host what the Department of Energy is calling its Nuclear Lifecycle Innovation Campuses, which will house startups that recycle spent nuclear waste into fresh fuel and medical isotopes. The Energy Department named Utah, Tennessee, Oklahoma, Louisiana, and Idaho as finalists for the facilities. “I’m pleased to announce that after reviewing 28 applications from 26 states, the Energy Department has selected five initial contenders to further explore building Nuclear Lifecycle Innovation Campuses,” Secretary of Energy Chris Wright said in a statement. “These campuses will be massive generators of economic growth, create thousands of high-paying jobs, and be crucial to unleashing America’s nuclear renaissance.”

Just last week, the Energy Department opened the door to nuclear projects sited on floating offshore platforms. It’s a novel idea for the U.S., but Russia launched its Akademik Lomonosov, a floating nuclear station, in 2019 in what is widely recognized as the world’s first real small modular reactor and only operating non-land nuclear plant. A new peer-reviewed study the World Nuclear Association conducted on the Rosatom-owned plant ranked it “on par with Russia’s top units,” World Nuclear News reported.

4. Interior Department approves a major solar project in Nevada, despite permitting freeze

Trump’s permitting freeze for renewables projects started to thaw for solar in particular earlier this year as the administration faced mounting pressure to stop thwarting the fastest-growing source of power in a country increasingly starved for new and swiftly available sources of electricity. The easing, as my colleague Jael Holzman wrote, was also part of a legal strategy. Regardless of the reasoning, the thaw is continuing — and not just because of the literal heat dome pushing temperatures in the Southwest into the triple digits. On Tuesday, the Department of the Interior’s Bureau of Land Management announced plans to advance a solar project in the Nevada desert. The Mosey solar farm, which would produce enough power at maximum output for 200,000 homes, is now under evaluation at the agency’s Nevada office, the agency notified the Federal Register. The regulator plans to conduct an environmental analysis and a resource management plan tweak needed for a project in a utility corridor. E&E News credited the administration’s shift on this particular project to lobbying by the state’s Republican governor, Joe Lombardo.

The project is part of developer Clearway’s larger efforts in Nevada. Separately, the company has volunteered to scrap one of its other solar projects in favor of building a gas plant, Jael reported this week.

5. A major battery facility in PJM just started construction

Yesterday, I told you the board of PJM Interconnection had scheduled an emergency auction to drum up 7 gigawatts of additional capacity to supply the electricity demand from data centers starting in 2028. It’s just one incremental way the nation’s largest grid system is “lurching toward reforms,” as my colleague Matthew Zeitlin wrote. It’s also inching toward more actual power infrastructure. On Wednesday, the developer Eolian Energy started construction on Flint Grid, a 1 gigawatt-hour storage project outside Columbus, Ohio. Located near a hub of data center and industrial power users, the Flint Grid project is “the first large-scale battery energy storage system to qualify for the PJM capacity market.” If it comes online in spring 2027 as promised on the project’s new website, it will represent more than half the new battery storage capacity in PJM’s line up for 2027 to 2028. The project is also the first grid-scale battery project permitted by the Ohio Power Siting Board and the largest in the PJM territory to date.

“There’s growing consternation about how the US can rapidly scale infrastructure to support America’s growing electricity demand, but not nearly enough conversation about how to use existing technology to unlock the wasted capacity that already exists on the grid,” Eolian founder and CEO Aaron Zubaty said in a statement. “This project requires hundreds of millions of dollars to construct, and we committed the necessary capital and resources years before today’s demand forecasts became headline news. As policymakers consider changes to competitive electricity markets, it’s critical that they avoid undermining the long-term investments already.”

THE KICKER

Lithium production typically involves either mining hard rocks or extracting salts through brines. Both are water intensive processes with considerable environmental tolls. Scientists at Texas A&M University are now developing a new approach involving the deployment of tiny, fish-like swimming nanorobots that capture lithium ions from seawater. Backed by a $1 million Energy Department grant, it’s among more than a dozen projects the agency is supporting in a bid to bolster domestic critical mineral supplies. “Unlike traditional mining that digs up land or pumps brine from underground and requires massive amounts of energy, these autonomous micro/nanorobots move freely through seawater to harvest lithium with virtually zero infrastructure footprint,” Jingjing Qiu, one of the mechanical engineers leading the research, said in a statement.

The 2030s crossroads.Rhodium Group

The 2030s crossroads.Rhodium Group