For being so cozy with (not to mention

bankrolled by) the oil and gas industry, Donald Trump still manages to get a lot wrong about the world’s dominant petroleum industry. Here’s everything he’s gotten wrong, and occasionally right, about the oil and gas industry while on the 2024 campaign trail.

“On January 6, we were energy independent.” [June 27, 2024]

Fact check: What does “energy independence” actually mean? Experts frequently dismiss the term as a political buzzword that isn’t helpful for understanding the United States’ position in the global energy market.

According to one definition, “energy independence” means that the United States produces more energy than it consumes. By this metric, the U.S. became energy independent in 2019, during the Trump administration, for the first time in 40 years, though it was the cumulative result of the shale boom that started in 2005 and stretched across three presidential administrations. By

this same metric, U.S. “energy independence” actually reached its highest level in 70 years in 2022 under President Biden, not Trump.

Another way to define “energy independence” would be that the U.S. doesn’t import any energy. This definition would also make Trump’s statement inaccurate: In 2020 under Trump, the U.S. imported

7.9 million barrels of crude oil and petroleum products per day. In 2023, under Biden, that number rose to 8.51 million barrels per day. Under both Trump and Biden, the U.S. has been a net exporter of oil products due in large part to its processing of crude oil. Check out this visualization from the U.S. from the Energy Information Administration for more granular detail on U.S. petroleum flows.

“We’re refining the oil. We have our refinery for that oil. It’s really, I call it tar. It’s not oil. It’s terrible. We have real stuff, but we’re refining it in Houston. So for all of the environmentalists, you ought to look at that because all of that tar is going right up into the atmosphere. You just ought to take a look. It’s the only plant that can do it. We have the only plants that can take tar and make it into oil.” [

March 6, 2024]

Fact check: Just because Trump decides to call something “tar” doesn’t mean it actually is tar. What he seems to be talking about here are the Canadian oil sands, sometimes called tar sands, which contain bitumen. The heavy, dirty, and diluted crude oil is transported via rail and pipeline from Canada to Texas, which is where most (but contrary to Trump’s claim, not all) of the world’s specialized heavy oil refineries are located.

Extracting, transporting, and refining bitumen is a pollution-heavy process. “All of that tar” doesn’t literally go “right up into the atmosphere,” but the refining process does emit benzene, carbon monoxide, and sulfur dioxide, which are known to increase instances of cancer, asthma, and other health conditions in the people who live or work nearby.

“Just yesterday, Biden blocked the export of American natural gas to other countries … Now, why he stopped it, I guess it was the environmentalists. I guess. But it’s good for the environment, not bad. And it’s good for our country. I will approve the export terminals on my very first day back.” [Jan. 27, 2024]

Fact check: This is wrong in a number of ways. Let’s take it from the top: First, Biden did not block the export of liquified natural gas to other countries; he temporarily paused the approval of new licenses to export LNG, including 17 that had been in the, er, pipeline. The United States is already the top exporter of LNG in the world, with output expected to double by the end of the decade from projects that are already licensed and under construction. The LNG licensing pause “will not impact our ability to continue supplying LNG to our allies in the near-term,” the Biden administration has said; current exports have been more than enough to meet Europe’s needs so far, even accounting for the war in Ukraine.

The permitting process will resume once the Department of Energy has updated its criteria for determining whether new LNG export terminals are in the “public interest” once their climate impacts are considered.

Now, about those climate impacts: It’s true that natural gas burns “cleaner” than coal, producing about 40% less carbon dioxide (and about 30% less than oil). But natural gas is also largely composed of methane, “a climate-altering super pollutant,” Jeremy Symons, an environmental and political analyst and strategist, told Heatmap.

While methane breaks down more quickly in the atmosphere than CO2, it also traps more heat — about 80 times more heat over the course of 20 years. The process of liquifying natural gas not only requires additional energy, it also introduces new opportunities for methane to leak, adding to the fuel’s climate impacts. Once all those leaks have been quantified, argues Cornell University researcher Robert Howarth, LNG is not only not beneficial to the environment, it’s actually worse than other fossil fuels. Howarth’s paper has not yet been peer-reviewed, and some have questioned his conclusions in the past. But there’s no question that building new LNG facilities will lock the U.S. into producing planet-warming fuel for years to come.

LNG certainly isn’t “good for the environment” of the people who live near fracking sites and export terminals, either, where health issues are rampant. In addition to methane, LNG plants release volatile organic compounds, which have been linked to higher instances of cancer, asthma, and birth defects.

“You have the highest energy costs in the entire country. In the first year, they’re going to be reduced by 50% because we’re going to drill, baby, drill.” [Jan. 23, 2024]

Fact check: Trump made these remarks after winning the New Hampshire primary — and they’re wrong. For one thing, while energy is expensive in the Granite State, New Hampshire’s Department of Energy says its energy costs are the fifth-highest in the lower 48.

There’s an even bigger fallacy in Trump’s statement, though: that drilling can quickly lower energy prices. For one thing, oil from new leases

doesn’t hit the market for at least four years, according to the Government Accountability Office. (Offshore drilling takes even longer since building the rigs alone can take two to three years.) As NPR explains, there are also operational limits; drilling new wells is “not as simple as turning a spigot and watching oil gush out.”

Much to the dismay of environmentalists, the Biden administration has also been

keeping pace with Trump’s historic drilling. In fact, as of 2024, the U.S. is producing more domestic crude than at any point during Trump’s presidency.

But even with all this new domestic crude, the U.S. is still susceptible to fluctuations in the global price of oil. That’s partially because the U.S. imports a different kind of oil than it exports — what those in the trade call light, sweet crude, compared to the gunkier, heavy crude most U.S. refineries are set up for. Reconfiguring refineries to handle the light crude oil “could underserve some product markets and idle (or even strand) the hundreds of billions of dollars invested in refinery conversion capacity,” the American Petroleum Institute

warns. Plus, it would also take even more time.

All that means that the U.S. is stuck relying on importing and exporting oil

even if domestic production ramps up even more than it already has. And that, in turn, means we’re at the mercy of fluctuations in global energy costs, which remain out of the White House’s singular control.

One more thing to note: “The oil industry can decide to produce more oil whenever it wants,” the Center for American Progress, a liberal public policy think tank,

explains, noting that the oil industry is sitting on “more than 9,000 approved — but unused — drilling permits on federal lands.” This is the base of the criticism that the oil industry is raking in “unprecedented profits” and burdening Americans with an artificially high cost of energy.

“Energy caused inflation, and energy has destroyed many families. Energy is considered very strongly. Energy is considered a country killer.” [Dec. 17, 2023]

Fact check: Economists mostly agree that “energy caused” the spike in inflation that we’ve seen since 2020, so in that sense, Trump is correct. But in making this argument, he inadvertently endorses the case for clean energy — since renewables aren’t subject to the same kinds of supply volatility as fossil fuels, they are therefore considered intrinsically deflationary.

“We are a nation that is begging Venezuela and others for oil. ‘Please, please, please help us,’ Joe Biden says, and yet we have more liquid gold under our feet than any other country anywhere in the world. We are a nation that just recently heard that Saudi Arabia and Russia will be reducing their oil production while at the same time substantially increasing the price. And we met that threat by announcing that we will no longer be drilling for oil in large areas in Alaska or elsewhere, anywhere in our states. We are a nation that is consumed by the radical left’s Green New Deal, yet everyone knows that the Green New Deal is fake. It is really the green new scam.” [Dec. 17, 2023]

Fact check: First, the United States is the top oil-producing country globally, followed by Russia and Saudi Arabia. It is true that the U.S. eased oil sanctions on Venezuela late last year, though that reprieve was explicitly temporary and contingent on the country holding free and fair elections.

Trump also appears to be referencing the Biden administration’s

recent decision to cancel oil and gas leases in the Arctic National Wildlife Refuge and block 13 million acres in the National Petroleum Reserve in Alaska from new drilling. While that does qualify as a large area in Alaska, the moves notably do not stop ConocoPhillips’ controversial Willow drilling project from going forward.

Trump further seems to be alluding to Biden’s campaign promise to not approve any new drilling (“

...anywhere in our states!”), but that hasn’t exactly gone to plan; although Biden issued a pause on new oil and gas leases on federal lands one week after taking office, the administration then lifted that pause a little over a year later in the face of numerous legal and political challenges. Over the summer, however, the Interior Department did raise the cost of drilling on federal lands.

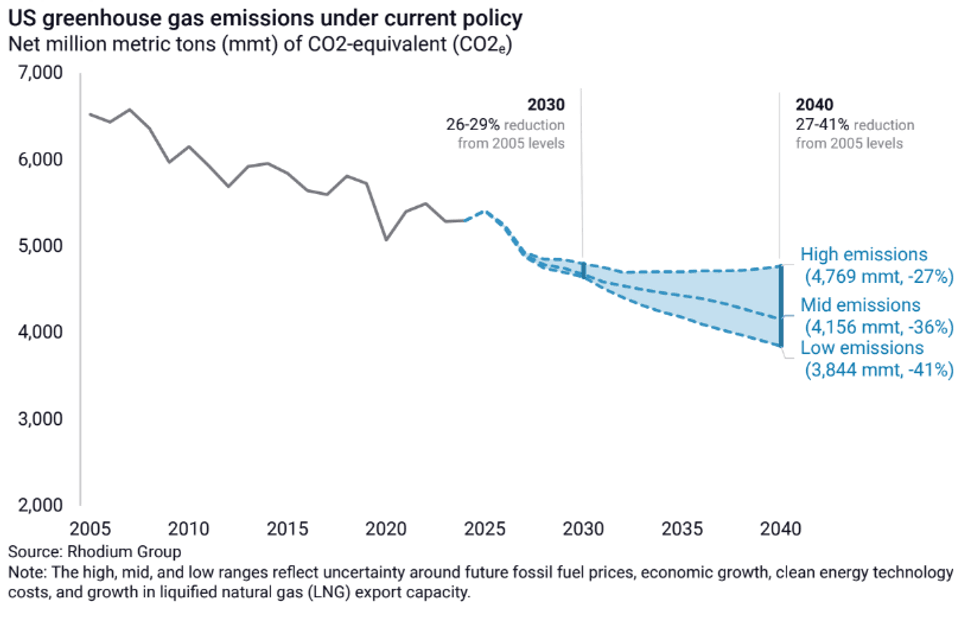

The 2030s crossroads.Rhodium Group

The 2030s crossroads.Rhodium Group