An investment boom is exploding in outer space. Investors have thrown their backing behind space-based solar power, orbital data centers, and even extraterrestrial power grids. SpaceX is pursuing an IPO — potentially the largest the world has ever seen — in part to fund its own off-Earth data center ambitions. The Space Foundation reported that the global space economy reached $613 billion in 2024, combining commercial revenue and government funding, while PricewaterhouseCoopers estimates the sector could grow to reach $2 trillion by 2040, largely driven by private sector innovation and support.

Different though they may be, these technologies all leverage the vast unknown outside our atmosphere to monitor, manage, and optimize terrestrial energy and climate systems.

This boom comes after roughly a decade of sharply falling launch costs, which has fueled a surge in satellite deployments for telecommunications and remote sensing applications. Together, these shifts have expanded the scope of what’s technically and economically possible in space — and in turn, broadened the range of systems and services needed to make this off-Earth infrastructure work.

“We’ve got over 14,000 satellites in space already, and that’s growing every day. It’s going to triple over the next five, six years,” Jeff Johnson, a general partner at the venture firm B Capital, told me. “And if you look at the other trend that’s happening, the power requirements for what’s going up in space have been growing dramatically and will continue to do so.” As Johnson explained, that’s because we’re asking satellites to do more — and to do it faster — than ever before: deliver high-speed internet globally, extend cell coverage in remote areas, and perform onboard data processing before transmitting imagery and other information down to Earth.

SpaceX, of course, has been the dominant force driving down launch costs while dramatically increasing the scale of satellite deployments with its partially reusable Falcon 9 rockets. More recently, it’s laid out an ambitious plan to put 100 gigawatts of “AI compute satellites” into orbit each year, with launches beginning as soon as 2028. As the company wrote in its S-1 filing ahead of its pending IPO, “we believe orbital AI compute is an incredibly difficult technical challenge that only we can solve at scale in the near term.” It also acknowledged, however, that the effort involves “significant technical complexity, unproven technologies, or technologies that do not exist,” and that ultimately, “such initiatives may not achieve commercial viability.”

It’s a startlingly frank assessment of an industry that holds both great potential and significant uncertainty. Much of SpaceX’s growth strategy — and likely the prospects of numerous other companies looking to launch large infrastructure into space — hinges on the success of its next-generation rocket called Starship. Designed to be fully reusable and much larger than any rocket built before, Starship will be capable of carrying roughly five to six times the volume and over eight times the massas Falcon 9. Throughout its 12 test launches so far, the rocket has seen both success and failures, accumulating mounting delays along the way.

The uncertainty around Starship’s future is one reason Johnson’s firm invested in Star Catcher, a startup that bills itself as “the first power grid in space.” He doesn’t view the startup’s value proposition as dependent on Starship’s success, betting that it can serve as critical infrastructure for satellites already in orbit today — not just for the bigger and better systems that future launch vehicles could enable.

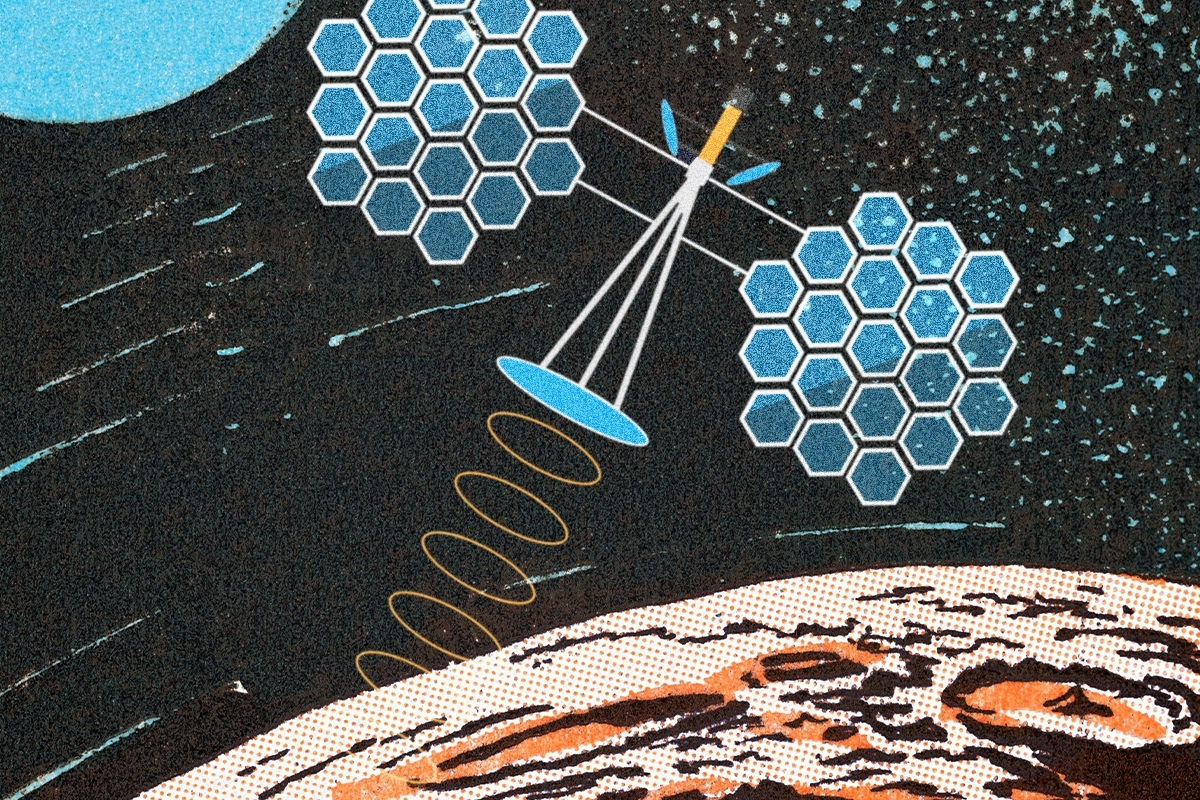

Founded less than two years ago, Star Catcher is developing a laser-based system to beam solar energy to satellites in low Earth orbit, supplying additional power directly to their solar arrays even when they’re in Earth’s shadow. This enables satellites to perform ever more power-intensive operations. It also addresses a fundamental constraint of satellite design: A satellite is only as powerful as the size of its solar array, which must be small enough to fit inside a rocket and also degrades over time.

“The average satellite in the Earth’s orbit has like 1,500 watts of power generation, which is as much as my kids’ gaming computer uses,” Andrew Rush, Star Catcher’s CEO, told me. “But we’re saying that satellite is going to be a cell tower, it’s going to be a data center, and those are multi-kilowatt, tens of kilowatts, hundreds of kilowatts applications. There’s a big disconnect there.”

B Capital led Star Catcher’s oversubscribed $65 million Series A round, which closed earlier this month. The fresh capital will help the company demonstrate its system in orbit and move towards commercialization. Star Catcher plans to launch its own constellation of power node satellites with the sole purpose of harnessing energy from the sun — or, as Rush quipped, “the greatest fusion reactor known to humankind.” Each node will then beam that energy to other power-hungry satellites by directing concentrated, near-infrared laser light at their solar panels. This type of light can deliver far greater power density than diffuse sunlight, providing satellites with a roughly 10-fold increase in power capacity compared to what they would generate alone.

As Rush explained, this then enables both satellite and rocket companies to “shrink the size of the solar arrays, and therefore, shrink the size of the spacecraft — actually make it less complex, less massive, and therefore less costly to field.” Already, he said the startup has signed seven power purchase agreements with satellite companies such as Loft Orbital and Astro Digital, as well as agreements or letters of intent with “almost every orbital data center startup” including Starcloud, which wants to begin offering cloud computing in space by early 2027.

For its part, Star Catcher aims to scale commercially by the end of the decade. Rush argues that just as bringing data processing closer to mobile users on the ground speeds up browsing and streaming, the growth of satellite broadband will create demand for the same infrastructure in space. That means everything from caching streaming content to running AI inference and processing satellite data in orbit, thus reducing the latency involved with routing everything to space and back.

While Star Catcher is focused on providing grid infrastructure for conventional satellites and orbital data centers, another recently funded startup, Cowboy Space, wants to build those data centers itself — and the rockets that will bring them to space. The company was founded in 2024 under the name Aetherflux, with the goal of beaming solar energy from space down to Earth. But with its latest $275 million Series B fundraise earlier this month, the company unveiled both a new name and a new mission.

Modern rocket designs from SpaceX — Cowboy Space’s most formidable competitor — pair a reusable lower section with a disposable upper section that carries satellites into orbit mounted at the rocket’s tip. After that upper section releases the satellite into orbit, the now purposeless component drifts through space, eventually burning up as it reenters Earth’s atmosphere. But Cowboy Space aims to transform what would otherwise be discarded debris into an orbital, 1-megawatt data center, integrating hundreds of Nvidia chips into the rocket’s upper section.

“We started with a blank sheet of paper with a goal of packing as many GPUs as tightly and densely as possible, and getting them to space,” Joseph Yaffe, the startup’s COO, told me over email. “We believe that this is a first-of-its-kind approach — the launch vehicle and the orbital data center designed as a single integrated system from day one.”

He told me that existing launch providers couldn’t offer the launch capacity or flexibility that Cowboy Space needs, and that the economics just wouldn’t pencil unless they did it themselves. Of course that’s an extremely tall order. SpaceX currently dominates the market for private rocket launches, a sector notoriously littered with failures. Only a few other private companies have even managed to make a dent in the space, and they’re still far behind Elon Musk’s industry giant.

Yaffe naturally thinks his company is well-positioned to become the exception, and prominent backers such as Index Ventures, Breakthrough Energy Ventures, and Andreessen Horowitz seem to agree. The startup is targeting the end of 2028 for its first proprietary rocket launch. Eventually, Cowboy Space plans to deliver processing power on par with conventional data centers, with Yaffe explaining that “abundant solar power and radiative cooling in orbit are what make that cost structure achievable.”

It’s true that space-based data centers would not require the same energy- and water-intensive fans, chillers, or cooling towers used on Earth, instead dissipating heat into space via infrared radiation — essentially emitting thermal energy as invisible light. But using today’s technology, power dense satellites can’t radiate heat quickly enough to sustain AI workloads, and how Cowboy Space plans to overcome this remains an open question. Even Nvidia CEO Jensen Huang acknowledged the difficulty, remarking in a recent keynote address at the GPU Technology Conference in San Jose that “we have to figure out how to cool these systems out in space.”

But if Cowboy Space and others can overcome these technical hurdles, there are some clear advantages to putting data centers into orbit. For one, building these energy-hungry behemoths has become a fraught political issue on both sides of the aisle, with local opposition exploding this year. Then there are the familiar constraints of limited power availability and interminably long grid interconnection queues, which are preventing hyperscalers from ramping up their AI efforts as quickly — and cleanly — as they’d like.

“AI demand is growing faster than terrestrial infrastructure can scale,” Yaffe argues. He’s betting that this dynamic will hold even if policy fixes such as permitting reform eventually materialize. “Orbital data centers aren’t a replacement for terrestrial infrastructure. The long-term opportunity is about expanding total compute capacity.”

Likewise, Johnson of B Capital doesn’t see the primary value proposition of orbital data centers as alleviating power or permitting constraints. “The reason why things are moving to space isn’t because we don’t have telecommunications that work right on Earth, it’s because new use cases are getting unlocked that are better,” he told me. “The first time you’re on a plane and use Startlink, you see that. The first time you need to be somewhere that isn’t really served well by Wi-Fi, and you use it, you see that. So there’s use cases that are transformational that can get unlocked by the space economy”

Not everyone is as bullish, however. Luigi Scatteia, the lead of PwC’s global space practice, told me he expects there to be “some form of data relay in orbit.” That might look more like space-based computing networks processing data from Earth observation satellites, as we’re already seeing the beginnings of today. But full-on data centers with the capabilities of terrestrial server farms? Launched from rockets? “I’m just going to say what my professor in university always used to tell us: Anything you do on Earth is always going to be more difficult in space.”

He, too, thinks the real unlock for orbital data centers and beyond would be “if Starship really works as intended,” he told me. “If you really want to do massive things in space — if you want to have a paradigm shift, a Copernican change — you need to drastically raise the capacity and lower the cost to orbit.”

No question these are two incredibly difficult tasks, not just for SpaceX but for the broader ecosystem of emerging space startups betting that private industry can fundamentally reshape the space economy. But according to Rush of Star Catcher, investors are now increasingly willing to take that bet too, in a way they weren’t when he first entered the industry a decade ago.

“Now, there’s the full spectrum of capital available, from seed all the way through IPO and beyond,” Rush told me. And that money is flowing to “really every flavor of space company. And so just by that metric alone, this is the golden age to build in space.”

A transformer factory in Jiangsu Province, China. Costfoto/NurPhoto via Getty Images

A transformer factory in Jiangsu Province, China. Costfoto/NurPhoto via Getty Images