Current conditions: Deadly flooding in parts of the Midwest is forecast to worsen Tuesday before rivers crest midweek • Northern China remains in drought as the southern province of Guangdong suffers flooding, landslides, and mudslides • Western India braces for heavy rains.

THE TOP FIVE

1. SCOTUS takes on NEPA

The U.S. Supreme Court is due to close out its latest session this week (although decisions could stretch into July), and court- and climate-watchers are expecting it to issue a death blow to a legal precedent called the Chevron deference, which gave federal agencies wide latitude to interpret their mandates where the law was vague. More than 19,000 federal court decisions rest on Chevron as a binding precedent, according to the Center for American Progress, and ending it would add to the already hefty legal burden of defending climate regulations.

But wait, there’s more! On Monday, the court agreed to take up a case that could determine whether federal agencies can consider a project’s indirect emissions when evaluating its environmental impacts. The case concerns a proposed railway that would transport oil in northeast Utah, which had its approval from the Surface Transportation Board thrown out by a federal appeals court last year. The appeals court ruled that the agency’s environmental review failed to assess how the railway would affect future oil development, along with several other environmental considerations. A group of Utah counties say those impacts are beyond the agency’s obligations under the National Environmental Policy Act.

A decision by the Supreme Court, which is expected to hear arguments in the fall, has the potential to apply not only to railways but also to many other projects regulated by the federal government, including pipelines and shipping ports.

2. Midwest floods leave path of destruction

A railroad bridge connecting Sioux City, Iowa, and North Sioux City, South Dakota, collapsed late Sunday amid flooding in the Midwest that also put a Minnesota dam in “imminent failure condition,” officials said.

The bridge, owned by BNSF Railway, spanned the Big Sioux River, where the water was about 45 feet high as of Monday morning — surpassing the previous record by more than 7 feet.

Minnesota’s Rapidan Dam on the Blue Earth River suffered a “partial failure” on Monday after water breached the west side of the dam and washed away an Xcel Energy substation. The Blue Earth County Sheriff's Office said on Facebook that it doesn’t know whether the dam will hold but that “there are no current plans for a mass evacuation.”

3. A California utility bets big on enhanced geothermal

The enhanced geothermal startup Fervo, which uses techniques borrowed from fracking oil and gas to access heat below the earth's surface to generate electricity, said today that it had signed the “world’s largest” geothermal power purchase agreements. The two deals with Southern California Edison, a California utility, add up to 320 megawatts from the company's Utah site. California utilities are mandated by the state energy regulator to buy 1,000 megawatts of non-weather-dependent power with no greenhouse gas emissions, for which geothermal fits the bill. The power will start flowing, Fervo said, by 2026 and will be fully up and running by 2028.

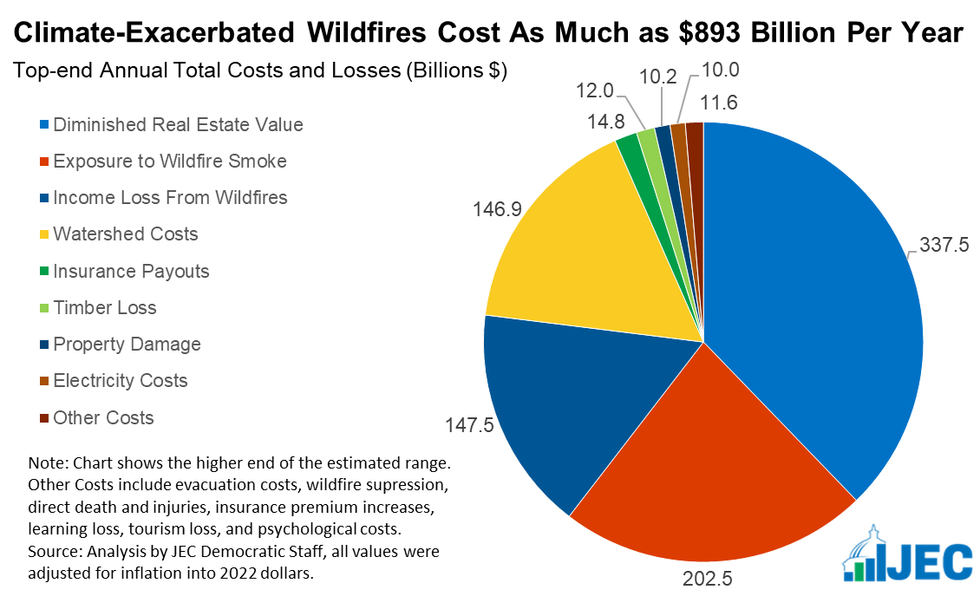

4. Study: Extreme wildfires are multiplying

Extreme wildfires have doubled in intensity and frequency over the past two decades due to climate change, according to a new study. The research, published in the journal Nature Ecology & Evolution, used satellite data to measure the occurrence of particularly powerful wildfires between 2003 and 2023. It found that such extreme events increased 2.2-fold during that period, with six of the past seven years ranking among the worst.

The changes aren’t uniform across biomes: Temperate conifer forests and boreal forests, both of which are prevalent in North America, are among the hardest hit. A report released last fall by Democrats on the Senate’s Joint Economic Committee showed the staggering cost of the fires to the United States. Accounting for damage to timber stocks and watersheds, smoke damage, lost income, and diminished real estate value on top of the property and insurance costs, the report found that fires cost the U.S. as much as $893 billion per year.

Senate Joint Economic Committee Democrats

Senate Joint Economic Committee Democrats

5. Coal plants’ reliability is diminishing

Coal plants are becoming less dependable as they age, the North American Electric Reliability Corporation said in its 2024 State of Reliability report. Coal plants’ weighted equivalent forced outage rate — defined as as “the probability that a group of units will not meet their generating requirements because of forced outages or forced derates,” with more weight given to larger generating units — was about 12% in 2023, compared with an average of 10% between 2014 and 2022, Jack Norris, a performance analysis engineer with NERC, told reporters. Norris said most other generation sources “have remained within a percentile over the same period,” while coal’s outage rates have been on the rise, Utility Dive reported. Rising maintenance needs and pressure to accommodate variable energy sources are also “having a negative impact on these units’ reliability,” Norris said.

THE KICKER

Germany will likely stop using coal before 2038 “just due to the economic viability,” the country’s climate envoy said Monday.