Now it is over. Early on Wednesday morning, negotiators in Dubai reached an agreement at the 28th Conference of the Parties to the UN Framework Convention on Climate Change, the global meeting otherwise known as COP28.

Their final text for

the Global Stocktake — a kind of report card on humanity’s progress on its Paris Agreement goals — is contradictory and half-hearted. Instead of blunt language instructing countries to “phase out fossil fuels,” it instead provides a range of options that could let countries achieve “deep, rapid, and sustained reductions in greenhouse gas emissions.” One of these possibilities is the tripling of global renewable capacity; another is a call for “transitioning away from fossil fuels.”

So far, this language — this call for leaving fossil fuels — has attracted the most attention by far. Simon Stiell, the UN’s top climate official,

said that it marked “the beginning of the end” of the fossil-fuel era, while the climate journalist and activist Bill McKibben has argued that the phrase can become a useful tool for activists, who can now beat it across the head of the Biden administration.

But a separate phrase in the agreement caught my attention. Immediately after calling for transitioning away from fossil fuels, the text makes a different point: that the world must accelerate the development of “zero- and low-emission technologies, including,

inter alia, renewables, nuclear, abatement and removal technologies such as carbon capture and utilization and storage, particularly in hard-to-abate sectors, and low-carbon hydrogen production.”

This language may rankle some readers because it seems to give pride of place to carbon capture and storage technology, or CCS, which would allow fossil fuel-burning plants to catch emissions before they enter the atmosphere. (It also seems to conflate CCS with carbon removal technology, even though they are different.) But I believe that the overarching demand — the call for accelerating climate-friendly technologies — represents a crucial insight, one that I could not stop thinking about at the COP itself, and one that is linked to any realistic demand to phase out fossil fuels. Here is that insight: The world will only be able to decarbonize when it develops abundant energy technologies that emit little carbon and that are price-competitive if not

cheaper than their fossil-fueled alternatives.

Just as COP28 began, the Rhodium Group, an energy research firm, published a new study looking at how carbon pollution will rise and fall through the end of the century. Unlike other such studies — which ask either how the planet will fare if no new climate policy passes, or what the world must do to avoid 1.5 degrees Celsius of warming — this new study tried to look at what was

likely to happen. Given what we know about how countries’ emissions rise and fall with their economies, and when and how they tend to pass climate policy, how much warming can we expect by the end of the century?

As the report’s authors put it, the study was aimed not at policymakers, but at policy takers — the officials, executives, engineers, and local leaders who are starting to plan for the world of 2100.

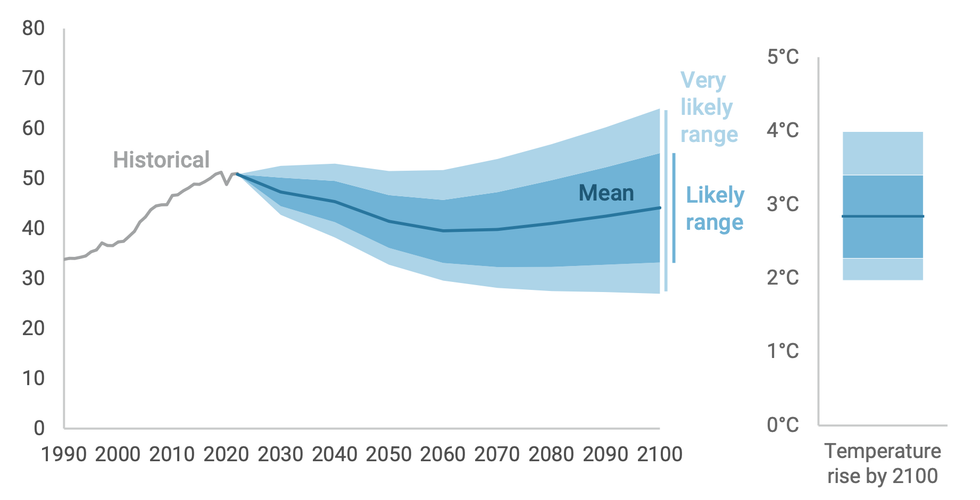

Here’s the good news: Global greenhouse gas emissions are likely to peak this decade, the report found. Sometime during the 2020s, humanity’s emissions of carbon dioxide, methane, and other climate pollution will reach an all-time high and begin to fall. (Right now, we emit

the equivalent of 50.6 billion tons of the stuff every year.) This will represent a world-historic turning point in our species’ effort to govern the global climate system, and it will probably happen before Morocco, Portugal, and Spain host the 2030 World Cup.

And that is roughly where the good news ends. Because unlike in rosy net-zero studies where humanity’s carbon emissions peak and then rapidly fall to zero, the report does

not project any near-term pollution plunge. Instead, global emissions waver and plateau through the 2030s and 2040s, falling in some years, rising slightly in others, cutting an unmistakably downward trend while failing to get anywhere close to zero. By 2060, annual emissions will have fallen to 39 gigatons, only 22% below today’s levels.

And — worse news, now — that is as low as emissions will ever get this century, the report projects. Driven by explosive economic growth in Southeast Asia and sub-Saharan Africa, global emissions begin to rise — slowly but inexorably — starting in the 2060s. They keep rising in the 2070s, 2080s, and 2090s. By the year 2090, emissions will have reached 44 gigatons, only 13% below today’s levels and roughly where emissions stood in 2003.

How Greenhouse Gas Emissions Could Fall — Then Rise — in the 21st Century

Rhodium Group

Rhodium Group

In other words, after a century of work to fight climate change, humanity will find itself roughly where it began. But now, with several thousand additional gigatons of emissions in the atmosphere, the planet will be about 2.8 degrees Celsius warmer (or about 5 degrees Fahrenheit). At its high end estimate, temperatures could rise as much as 4 degrees Celsius, or more than 7 degrees Fahrenheit.

This temperature rise will be caused by legacy emissions from polluters like the United States and China, but as the century goes on, it will increasingly come from Asian and African countries such as Vietnam, Indonesia, Nigeria, Kenya, and others. Why? It’s not like these countries, say, reject renewables or electric vehicles: In fact, Rhodium anticipates that renewables will have grown up to 22-fold by the end of the century.

Instead, emissions rise because fossil fuels are cheap and globally abundant — they remain one of the easiest ways to power an explosively growing society — and because of the growth of the so-called hard-to-abate sectors in these countries are slated to grow just as quickly as the economies themselves. Indonesia, Nigeria, and Vietnam will demand many megatons of new steel, cement, and chemicals to furnish their growing societies; right now, the only economical way to make those materials requires releasing immense amounts of carbon pollution into the atmosphere.

Let’s be clear: Rhodium’s report is a projection, not a prophecy. It should not provoke despair, I think, but determination. Many of the so-called hard-to-abate activities, such as steel or petrochemical making, should more aptly be called activities-that-we-haven’t-tried-very-hard-to-abate yet; people will likely find a way to do them by the middle of the century. (When I asked Bill Gates what he thought about the Rhodium Group’s findings, he replied that predicting the carbon intensity of certain activities in 2060 was all but impossible: We might have safe, cheap, and abundant nuclear fission by then, or even nuclear fusion.)

Yet it heralds a shift in climate geopolitics that, while it has not yet happened, is not so far away. Since the modern era of global climate politics began in 1990, most carbon emissions have come from just a handful of countries: China, the United States, and the 37 other rich, developed democracies that make up the Organization for Economic Cooperation and Development, or OECD. These countries have emitted 55% of climate pollution since 1990, while the rest of the world — the remaining low- and middle-income countries — have emitted only 45%.

But from now to 2100, that relationship is set to reverse. Through the end of the century, China and the OECD countries emit only 40% of total global emissions, according to Rhodium’s projections. The rest of the world, meanwhile, will emit 60% of global emissions.

In other words, decarbonization will soon become a challenge for middle-income countries. These countries will not be able to spend extra to buy climate-friendly technologies, but they are simply too populous for rich countries to subsidize. At the same time, these countries lack an existing fleet of fossil-fuel-consuming equipment, so they will not need to transition away from fossil fuels in the first place. Unlike in the United States, where we will have to shut down our oil-and-gas economy as we build a new one to replace it, Kenya or Indonesia can more or less build a climate-friendly middle-class economy de novo, much in the same way that in the 2000s countries “leapfrogged” landline telephones and adopted cell phones. Yet countries will only be able to leapfrog the fossil-fuel era if the climate equivalent of cell phones exist: if climate-friendly technologies are plentiful, useful, and price-competitive.

That’s not all it will take, of course. The world will have to phase down the production and consumption of fossil fuels, because the existence of climate-friendly technologies will not guarantee their use. Humanity may also have to create and enforce a strong moral taboo around burning fossil fuels, much in the same way that it has created a taboo around, say, child labor. But none of that can happen unless climate-friendly alternatives exist: Otherwise countries will ensure that they gain access to the energy that their development requires.

Rhodium Group

Rhodium Group