You’re not imagining things: Electricity prices are surging.

Electricity rates, which have increased steadily since the pandemic, are now on a serious upward tear. Over the past 12 months, power prices have increased more than twice as fast as inflation, according to recent government data. They will likely keep rising in years to come as new data centers and factories connect to the power grid.

That surge is a major problem for the economy — and for President Trump. On the campaign trail, Trump vowed to cut Americans’ electricity bills in half within his first year in office. “Your electric bill — including cars, air conditioning, heating, everything, your total electric bill — will be 50% less. We’re going to cut it in half,” he said.

Now Trump has mysteriously stopped talking about that pledge, and on Tuesday he blamed renewables for rising electricity rates. Even Trump’s Secretary of Energy Chris Wright has acknowledged that costs are doing the opposite of what the president has promised.

Trump’s promise to cut electricity rates in half was always ridiculous. But while his administration is likely making the electricity crisis worse, the roots of our current power shock did not begin in January.

Why has electricity gotten so much more expensive over the past five years? The answer, despite what the president might say, isn’t renewables. It has far more to do with the part of the power grid you’re most familiar with: the poles and wires outside your window.

How electricity costs are set

Before we begin, a warning: Electricity prices are weird.

In most of the U.S. economy, markets set prices for goods and services in response to supply and demand. But electricity prices emerge from a complicated mix of regulation, fuel costs, and wholesale auction. In general, electricity rates need to cover the costs of running the electricity system — and that turns out to be a complicated task.

You can split costs associated with the electricity system into three broad segments. The biggest and traditionally the most expensive part of the grid is generation — the power plants and the fuels needed to run them. The second category is transmission, which moves electricity across long distances and delivers it to local substations. The final category is distribution, the poles and wires that get electricity the “the last mile” to homes and businesses. (You can think of transmission as the highways for electricity and distribution as the local roads.)

In some states, especially those in the Southeast and Mountain West, monopoly electricity companies run the entire power grid — generation, transmission, and distribution. A quasi-judicial body of state officials regulates what this monopoly can do and what it can charge consumers. These monopoly utilities are supposed to make long-term decisions in partnership with these state commissions, and they must get their permission before they can raise electricity rates. But when fuel costs go up for their power plants — such as when natural gas or oil prices spike — they can often “pass through” those costs directly to consumers.

In other states, such as California or those in the Mid-Atlantic, electricity bills are split in two. The “generation” part of the bill is set through regulated electricity auctions that feature many different power plants and power companies. The market, in other words, sets generation costs. But the local power grid — the infrastructure that delivers electricity to customers — cannot be handled by a market, so it is managed by utilities that cover a particular service area. These local “transmission and distribution” utilities must get state regulators’ approval when they raise rates for their part of the bill.

The biggest driver of higher costs: poles and wires

The biggest driver of the power grid’s rising costs is … the power grid itself.

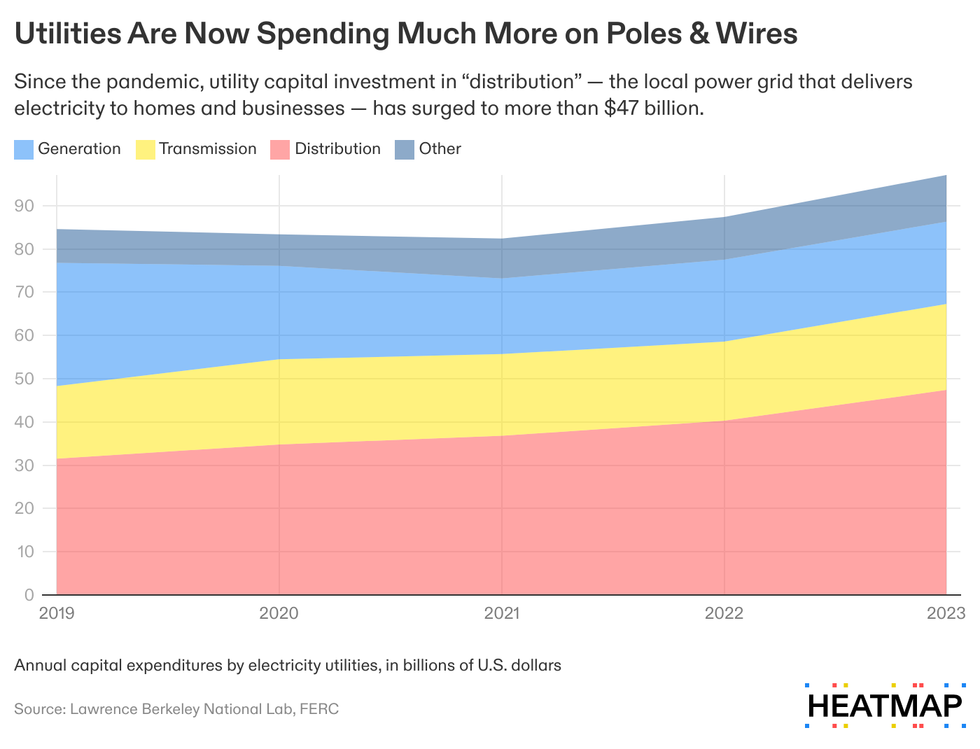

Historically, generation — building new power plants, and buying the fuel to run them — has driven the lion’s share of electricity rates. But since the pandemic, the cost of building the distribution system has ballooned.

Electricity costs are “now becoming a wires story and less of an electrons story,” Madalsa Singh, an economist at the University of California Santa Barbara, told me. In 2023, distribution made up nearly half of all utility spending, up from 37% in 2019, according to a recent Lawrence Berkeley National Laboratory report.

Where are these higher costs coming from? When you look under the hood, the possibly surprising answer is: the poles and wires themselves. Utilities spent roughly $6 billion more on “overhead poles, towers, and conductors” in 2023 than in 2019, according to the Lawrence Berkeley report. Spending on underground power lines — which are especially important out West to avoid sparking a wildfire — increased by about $4 billion over the same period.

Spending on transformers also surged. Transformers, which connect different circuits on the grid and keep the flow of electricity constant, are a crucial piece of transmission and distribution infrastructure. But they’ve been in critically short supply more or less since the supply chain crunch of the pandemic. Utility spending on transformers has more than doubled since 2019, according to Wood Mackenzie.

At least some of the costs are hitting because the grid is just old, Singh said. As equipment reaches the end of its life, it needs to be upgraded and hardened. But it’s not completely clear why that spike in distribution costs is happening now as opposed to in the 2010s, when the grid was almost as old and in need of repair as it was now.

Some observers have argued that for-profit utilities are “goldplating” distribution infrastructure, spending more on poles and wires because they know that customers will ultimately foot the bill for them. But when Singh studied California power companies, she found that even government-run utilities — i.e. utilities without private investors to satisfy — are now spending more on distribution than they used to, too. Distribution costs, in other words, seem to be going up for everyone.

Sprawling suburbs in some states may be driving some of those costs, she added. In California, people have pushed farther out into semi-developed or rural land in order to find cheaper housing. Because investor-owned utilities have a legal obligation to get wires and electricity to everyone in their service area, these new and more distant housing developments might be more expensive to connect to the grid than older ones.

These higher costs will usually appear on the “transmission and distribution” part of your power bill — the “wires” part, if it is broken out. What’s interesting is that as a share of total utility investment, virtually all of the cost inflation is happening on the distribution side of that ledger. While transmission costs have fluctuated year to year, they have hovered around 20% of total utility investment since 2019, according to the Lawrence Berkeley Labs report.

Higher transmission spending might eventually bring down electricity rates because it could allow utilities to access cheaper power in neighboring service areas — or connect to distant solar or wind projects. (If renewables were driving up power prices as the president claims, you might see it here, in the “transmission” part of the bill.) But Charles Hua, the founder and executive director of the think tank PowerLines, said that even now, most utilities are building out their local grids, not connecting to power projects that are farther away.

The rising cost of natural disasters

The second biggest driver of higher electricity costs is disasters — natural and otherwise.

In California, ratepayers are now partially footing the bill for higher insurance costs associated with the risk of a grid-initiated wildfire, Sam Kozel, a researcher at E9 Insight, told me. Utilities also face higher costs whenever they rebuild the grid after a wildfire because they install sensors and software in their infrastructure that might help avoid the next blaze.

Similar stories are playing out elsewhere. Although the exact hazards vary region by region, some utilities and power grids have had to pay steep costs to rebuild from disasters or prevent the likelihood of the next one occurring.

In the Southeast, for instance, severe storms and hurricanes have knocked out huge swaths of the distribution grid, requiring emergency line crews to come in and rebuild. Those one-time, storm-induced costs then get recovered through higher utility rates over time.

Why have costs gone up so much this decade? Wildfires seem to grow faster now because of climate change — but wildfires in California are also primed to burn by a century of built-up fuel in forests. The increased disaster costs may also be partially the result of the bad luck of where storms happen to hit. Relatively few hurricanes made landfall in the U.S. during the 2010s — just 13, most of which happened in the second half of the decade. Eleven hurricanes have already come ashore in the 2020s.

A long-delayed electricity shock from Ukraine

Because fuel costs are broadly seen as outside a utility’s control, regulators generally give utilities more leeway to pass those costs directly through to customers. So when fuel prices go up, so do rates in many cases.

The most important fuel for the American power grid is natural gas, which produces more than 40% of American electricity. In 2022, surging demand and rising European imports caused American natural gas prices to increase more than 140%. But it can take time for a rise of that magnitude to work its way to consumers, and it can take even longer for electricity prices to come back down.

Although natural gas prices returned to pre-pandemic levels by 2023, utilities paid 30% more for fuel and energy that year than they did in 2019, according to Lawrence Berkeley National Lab. That’s because higher fuel costs do not immediately get processed in power bills.

The ultimate impact of these price shocks can be profound. North Carolina’s electricity rates rose from 2017 to 2024, for instance, largely because of natural gas price hikes, according to an Environmental Defense Fund analysis.

The very beginning of data center-induced power growth

The final contributor to higher power costs is the one that has attracted the most worry in the mainstream press: There is already more demand for electricity than there used to be.

A cascade of new data centers coming onto the grid will use up any spare electron they can get. In some regions, such as the Mid-Atlantic’s PJM power grid, these new data centers are beginning to drive up costs by increasing power prices in the capacity market, an annual auction to lock in adequate supply for moments of peak demand. Data centers added $9.4 billion in costs last year, according to an independent market monitor.

Under PJM’s rules, it will take several years for these capacity auction prices to work their way completely into consumer prices — but the process has already started. Hua told me that the power bill for his one-bedroom apartment in Washington, D.C., has risen over the past year thanks largely to these coming demand shocks. (The Mid-Atlantic grid implemented a capacity-auction price cap this year to try to limit future spikes.)

Across the country, wherever data centers have been hooked up to the grid but have not supplied or purchased their own around-the-clock power, costs will probably rise for consumers. But it will take some time for those costs to be felt.

In order to meet that demand, utilities and power providers will need to build more power plants, transmission lines, and — yes — poles and wires in the years to come. But recent Trump administration policies will make this harder. The reconciliation bill’s termination of wind and solar tax credits, its tariffs on electrical equipment, and a new swathe of anti-renewable regulations will make it much more expensive to add new power capacity to the strained grid. All those costs will eventually hit power bills, too, even if it takes a few years.

“We're just getting started in terms of price increases, and nothing the federal administration is doing ‘to assure American energy dominance’ is working in the right direction,” Kozel said. “They’re increasing all the headwinds.”

A vessel sails past the partially dried-up river bed of the Rhine in Duisburg, western Germany. Ina FASSBENDER / AFP via Getty Images

A vessel sails past the partially dried-up river bed of the Rhine in Duisburg, western Germany. Ina FASSBENDER / AFP via Getty Images