The transition to clean energy is largely a shift from molecules to electrons — gasoline in the tank is out, electricity stored in a battery cell is in. It follows, then, that as the transition progresses, the balance of power in the energy industry will shift from oil and gas production to electricity generation.

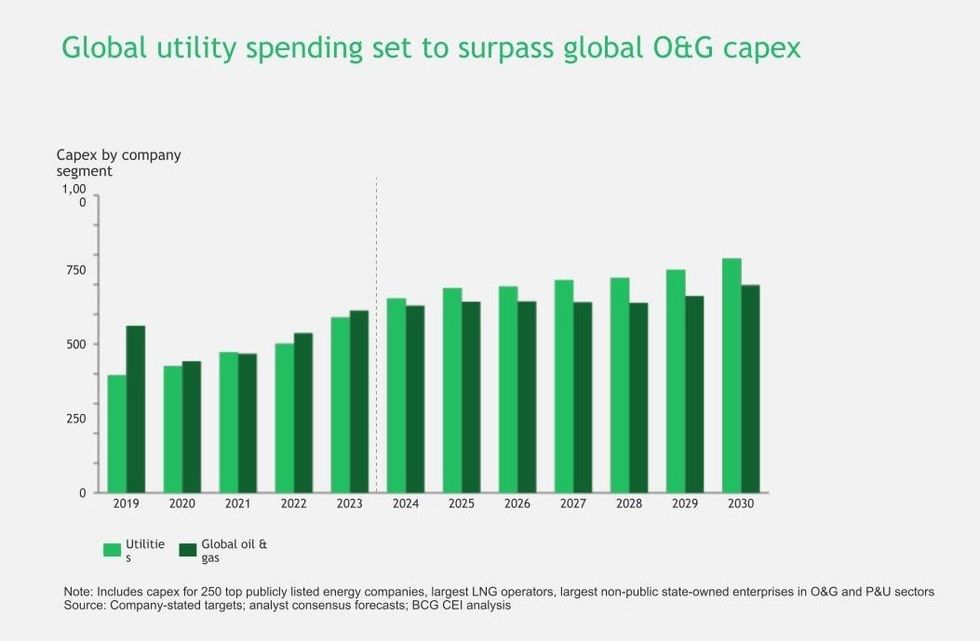

We may look back on 2024 as the year the scales tipped. Among the top 260 publicly listed energy companies, utilities’ capital expenditures around the globe were slightly higher this year than oil and gas spending, according to a recent analysis from Boston Consulting Group, and the authors expect the trend to grow through the end of the decade. But it wasn’t a sudden spike in EV adoption or home electrification or some other climate solution that put utility spending in the lead. It was the rise in data centers.

“When we went through all the data, all the 260 companies, it was the data centers that were having the biggest impact, most definitely,” Rebecca Fitz, a partner and director at Boston Consulting Group and lead author of the report, told me. “I’ve been in this sector for a long time, and to have such a rapid change in demand outlook, coupled with quick changes to capex, is a big story.”

Boston Consulting Group Center For Energy Impact

Boston Consulting Group Center For Energy Impact

The finding was the surprise headline of an annual report that Fitz’ group has completed for the past three years called “Follow the Capital,” an analysis of what’s driving changes in capital supply and demand in the energy sector using data culled from publicly available sources. Data for prior years comes from regulatory and investor fillings. Future years are modeled using public announcements, plans filed with regulators, and a few conservative assumptions, Fitz told me.

Surging demand for electricity from data centers was perhaps the biggest energy story of 2024, and the trend seemed to accelerate as the year went on. In just the past few months, almost every major tech company has signed an agreement to buy power from a nuclear plant, either reviving formerly shuttered reactors or helping to build new ones. GE Vernova, which manufactures energy generation equipment, reported last week that it had secured contracts for 9 gigawatts’ worth of new gas turbines since its previous quarterly report in October, “tied to both load growth in the U.S and … serving the hyperscaler demand associated with AI.” As the “Follow the Capital” authors were wrapping up this year’s edition in November, they found that U.S. utilities had added $50 billion in planned capex during the third quarter alone, mostly due to data center demand growth.

Data center demand isn’t the only factor playing into the above chart. Though utility spending is definitely up, oil and gas companies are also reining in capex growth in favor of shareholder returns, Fitz told me. But oil and gas also sees the winds changing and is making moves to get into the power business. Two weeks ago, during a panel hosted by the Atlantic Council, Chevron CEO Mike Wirth said the company was “looking at possible solutions to build large-scale power generation” that would serve data centers directly, rather than feed into the grid, so that regular electricity ratepayers would not shoulder the costs. “There’s sensitivity to increasing electricity rates for the average person just for the benefit of a few of these tech companies,” he said.

Beating Chevron to the punch, last week ExxonMobil announced that it was “moving fast” on this exact type of project, designing a natural gas plant that would “use carbon capture to remove more than 90% of the associated CO2 emissions” and directly power data centers without connecting to the grid.

“I have no doubt that most of the oil and gas sector is looking at opportunities in this area,” said Fitz.

Though the report covers global companies and spending, the data center demand signal is hyperlocal. Among the 30 largest North American utilities, 65% of demand growth is concentrated within just six of them, the report says. Though the report does not name the companies, Fitz told me that Texas, North Carolina, Virginia, and Ohio were seeing the most aggressive plans.

Artificial intelligence boosters often argue that this demand pull is a boon for the energy transition. By ushering in the age of electrons, the logic goes, tech companies with deep pockets can drive the first deployments of new clean energy technologies like advanced nuclear and geothermal power plants. These early deployments would then help lower costs and give rise to cheaper, cleaner electricity for the rest of us average energy consumers and our future electric cars, stoves, and water heaters.

But that’s not the only potential outcome. “Follow the Capital” found that when the six utilities most affected by demand growth recently revised their integrated resource plans, they increased the amount of natural gas generation they planned to add from 26% of total new generation to 31%. As GE Vernova reported, orders for gas generators are skyrocketing. “I can’t think of a time that the gas business has had more fun than they’re having right now,” the company’s CEO Scott Strazik said during a recent investor update.

As my colleague Matthew Zeitlin reported, the industry is turning to natural gas plants because they can run 24/7 and they are not as dependent on transmission lines as renewables are, so they can be built faster and more cheaply. Renewables paired with energy storage are only competitive with gas if there’s infrastructure to support it, sources told him.

The age of electrons may be nigh, but whether it helps to stop climate change is a separate question altogether.

Boston Consulting Group Center For Energy Impact

Boston Consulting Group Center For Energy Impact

Women snooze on the Havana waterfront on Sunday.YAMIL LAGE / AFP via Getty Images

Women snooze on the Havana waterfront on Sunday.YAMIL LAGE / AFP via Getty Images