Current conditions: Hurricane Kiko is soaking Hawaii and slashing the archipelago with giant waves • Nearly a foot of rain is forecast to fall on parts of Texas, risking flash floods • Dry, windy weather across broad swaths of South Africa is bringing “extremely high” fire risk.

THE TOP FIVE

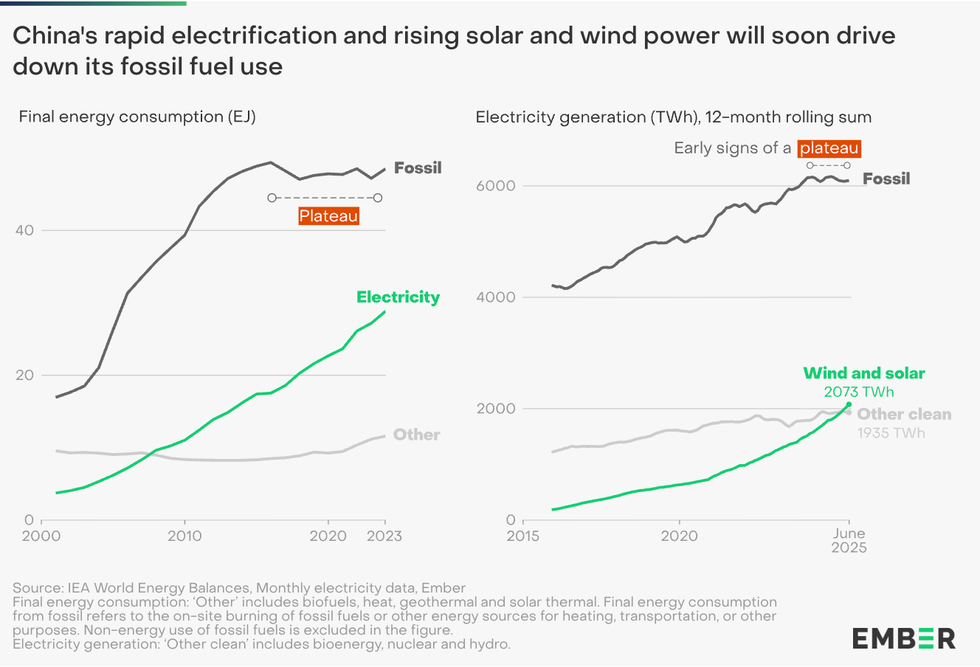

1. China’s clean energy boom is tilting the world toward a fossil phaseout

China's clean-energy investments are paying green dividends. Ember

China's clean-energy investments are paying green dividends. Ember

China’s clean energy boom is bringing a global decline in fossil fuel demand into sight amid declines in usage in the buildings, vehicles, and industries of the world’s second-largest economy, according to the think tank Ember’s latest China Energy Transition Review. The report, released Tuesday morning, found that exports of solar panels, batteries, electric vehicles, and heat pumps are soaring, particularly to emerging economies, making the possibility of developing nations making possible an “energy leapfrog” over the coal phase of growth. From 2015 to 2023, China’s end consumption of fossil fuels fell 1.7% across buildings, industry and transport, while electricity use as a replacement rose by 65%. In power generation, fossil output dropped 2% in the first half of 2025 compared to the same period last year, as wind and solar generation soared by 16% and 43%, respectively. Last year alone, Beijing invested $625 billion in clean energy, 31% of the global total.

“China is now the main engine of the global clean energy transition,” Muyi Yang, coordinating lead author of Ember’s 2025 analysis, said in a statement. “Policy and investment decisions made in China over the last two decades are fundamentally changing the basis of China’s own energy system, and enabling other countries to also move swiftly from fossil to clean.”

2. Tesla’s U.S. market share plunged to its lowest recorded level

As Americans scramble to buy electric vehicles ahead of the expiration of the $7,500 consumer tax credit at the end of this month, fewer of those cars are Teslas. The preliminary August data Cox Automotive released on Monday showed the best month for EVs in U.S. history was the worst for Tesla ever recorded. EVs climbed to almost 10% of total car sales last month, but Tesla’s share fell to 38%, with 55,000 cars sold all month. That’s up just 3% compared to July and down 6% from the year prior, while the company’s total market share fell from just over 40% in July and 45% in the first half of the year. By contrast, Heatmap’s Matthew Zeitlin noted, Tesla commanded about 80% of U.S. EV sales in 2020.

Also on Tuesday, the company unveiled two new energy storage products that could boost its utility division. At the RE+ conference in Las Vegas, Tesla presented the Megapack 3, the latest generation of its utility-scale battery system, and the Megablock, which integrates the Megapack 3 with transformers and switchgear. Batteries were Tesla’s fastest growing business in the first quarter of this year, as Matthew reported in April, but the company feared that tariffs would affect the business. “The energy segment — which includes the company’s battery energy storage businesses for residences (Powerwall) and for utility-scale generation (Megapack) — has recently been a bright spot for the company, even as its car sales have leveled off and declined.”

3. Google backs long-duration energy storage experiments in Arizona

Google inked a deal with the Salt River Project, the utility serving much of Arizona’s largest metropolis, to test the performance of long-duration energy storage projects. The first-of-a-kind research collaboration aims to “better understand the real-world performance of emerging non-lithium ion long duration energy storage technologies” in the Phoenix area, the power company said in a press release. Google will fund a portion of the costs and evaluate data on the pilot projects’ operational success. “We believe that long duration energy storage will play an essential role in meeting SRP’s sustainability goals and ensuring grid reliability,” Chico Hunter, the nonprofit Salt River Project’s manager of innovation and development, said in a statement.

As I reported in this newsletter in July, Google also backed the Italian carbon dioxide-based storage startup Energy Dome as the tech giant pushes to expand its portfolio of technologies to power its data centers 24/7.

4. The European Union backs research into more nuclear power

The European Union has been a solid backer of fusion energy research. But the anti-nuclear trifecta of Germany, Austria, and Luxembourg has long thwarted bloc-wide efforts to bolster fission, which provides the bulk of the continent’s electricity. With Berlin finally joining Paris in backing traditional nuclear power, that blockade is no longer holding. The European Commission has proposed spending $11.5 billion on bolstering research in both fusion and fission, the trade publication NucNet reported Monday.

5. Data center trade group pushes U.S. regulators to ‘unleash’ nuclear

Meanwhile in the United States, where nuclear power remains broadly supported across the political spectrum, the biggest question is how quickly new reactors can come online. The data center industry has now called on the Nuclear Regulatory Commission to streamline licensing of new reactors to help meet its surging demand for electricity. In a letter to NRC Chair David Wright shared with E&E News, the Data Center Coalition, a trade group representing server farms, urged the agency to update its regulations to ensure quicker deployment of advanced reactors. “Increasingly, DCC members are forming strategic partnerships and committing to offtake agreements with utilities and nuclear technology developers, injecting new momentum into this strategic sector,” wrote Cy McNeill, the group’s director of federal affairs. “We are approaching the cusp of a truly revitalized nuclear sector.”

The push comes amid what Heatmap’s Katie Brigham called a “nuclear power dealmaking boom.”

THE KICKER

Patagonia’s billionaire founder helped popularize the greenest trend in apparel — buying less of higher quality, longer-lasting clothing. Now the retailer is pushing to bring that same ethos to the food business. The company’s edible offerings of tinned fish and crackers designed for hiking is now expanding into baby foods, oils, and sauces, The New York Times reported in a new profile of the retailer. Fifty years from now, founder Yvon Chouinard told the newsletter, “I could see the food business being bigger than the apparel business.”

China's clean-energy investments are paying green dividends. Ember

China's clean-energy investments are paying green dividends. Ember