Climate tech funding has slowed in the face of federal government pushback — but it has certainly not stopped. As the administration has cranked up its hostilities against everything from electric vehicles to wind turbines, companies and investors are responding by getting strategic, forming new coalitions to map, fund, and shape progress in the absence of public support.

Last month I covered the launch of the Climate Tech Atlas, an interdisciplinary effort that includes venture capitalists, nonprofits, and academics working to map out the most salient climate tech opportunities and help guide external research and funding in the sector. There’s also the All Aboard Coalition, which unites big name investors to help plug the missing middle finance gap. Sector-specific investment vehicles are popping up too, like the Oneworld BEV fund, a partnership between major airlines in the Oneworld Alliance and Breakthrough Energy Ventures to advance the commercialization of sustainable aviation fuels. All three of these new initiatives were announced in September alone.

“We are in a unique moment right now,” Carmichael Roberts, a managing partner at BEV told me via email. “Over the past decade, the climate tech ecosystem has made enormous progress driving innovation across every sector of the economy. That puts us in the position to step back and ask first, what areas are still crying out for urgent innovation?”

This year has also seen a number of climate tech companies struggle at key points in their attempts to scale. Sodium-ion battery company Natron Energy shut down in September, while direct air capture leader Climeworks laid off 22% of its staff in May, citing “current macroeconomic uncertainty” and “shifting policy priorities where climate tech is seeing reduced momentum.” Another direct air capture company, Noya, shuttered this August, while the battery recycling company Li-Cycle filed for bankruptcy in May.

Other startups pursuing emerging technologies — from carbon capture to long-duration battery storage, advanced geothermal, and next-generation nuclear — are looking to avoid the same fate. But while federal funding from places such as the Department of Energy’s Office of Clean Energy Demonstrations and the Loan Programs Office once provided an avenue for financing capital-intensive demonstration plants, the Trump administration is now retracting funding, going so far as to cancel contracts with projects previously approved under Biden.

The Oneworld fund, announced in mid-September, is BEV’s first to focus on a specific theme and its first to be backed by an industry coalition. Members of the Oneworld Alliance — which include Alaska Airlines, American Airlines, British Airways, and Cathay Pacific — had already committed to using SAF for 10% of their fuel by 2030, while also “playing an active role in the development of SAF at commercial scale.” Now, with alliance members serving as limited partners in the venture fund, they’ll benefit from the technical and commercial expertise of one of the sector’s most influential VC firms.

When I asked the BEV team to what degree the current political and economic uncertainties were making partnerships like this more valuable, Eric Toone, another BEV managing partner, responded with a refrain I’ve become familiar with — that the firm only backs technologies that “can ultimately compete on their own merits.” Yet it’s undeniable that the federal government tore up its decarbonization agenda at a moment when many climate tech firms’ investments are almost ready for deployment, a stage when government support can make all the difference.

“Many promising SAF technologies already exist, but they are stuck between lab success and commercial scale,” Roberts told me. “This is the moment when they most need capital, technical rigor, and committed offtake to bridge that gap.” While the Trump administration did maintain and extend the tax credit for clean fuels, it also reduced the maximum credit amount for SAF from $1.75 per gallon to $1, while private funding for SAF production and distribution infrastructure remains inadequate.

Given this landscape and the urgency airlines face in meeting their clean fuel targets, Toone told me the firm is open to backing companies “that are further along than what a typical BEV fund might pursue.” And while sustainable fuels are the first technology to benefit from this type of thematic focus, Roberts said that BEV is already eyeing other sectors where it plans to apply this same funding model.

As of early September, the firm is also part of the All Aboard Coalition. This elite group of venture firms is aiming to raise a $300 million fund by the end of October that will match investments in later-stage venture rounds, filling a gap known in climate tech circles as the “missing middle.” Assembled by Chris Anderson, an entrepreneur and primary convener of the TED Talks conference — which has featured many inspiring climate visionaries — the group includes 14 members such as Khosla Ventures, Prelude Ventures, DCVC, Gigascale Capital, and Energy Impact Partners.

“One of the consequences of being in the front row seat at TED all these years is you get persuaded of certain things,” he told me. “And I definitely got persuaded that climate is the outstanding, major problem we really have to fix.”

The bulk of the capital for the coalition will come from outside investors, though some members will contribute as well, Anderson told me. The goal is to incentivize these hotshots to co-invest with each other, providing a one-to-one funding match if they do so.

“First-of-a-kind rounds seem out of reach for a lot of people in the chain,” Anderson explained, referring to the network of investors that must come together to help a company fund expensive new infrastructure. At this stage, its tech has progressed beyond the capital-light, early-stage rounds but is still considered too risky for traditional infrastructure investors to take on. Companies might be seeking $100 million or more from venture firms that are used to writing checks for orders of magnitude less. “Really the purpose of the fund is to create a collective belief that there is a pathway to getting these companies funded. If you have that collective belief, then it’s much easier for a lead investor to step forward and to pull a few other people in.”

Anderson acknowledged that a $300 million fund will not go “nearly far enough.”

“It’s a starter fund. It’s a proof of concept,” he told me. “The world needs to make a couple hundred of these bets at some point.”

Other coalitions, such as the Climate Tech Atlas, are working to steer the sector towards the best bets. This group — which also includes Breakthrough Energy Ventures, alongside others such as the nonprofit investment platform Elemental Impact, the consulting firm McKinsey, and Stanford University’s Doerr School of Sustainability — has mapped out the technological milestones it sees as the clearest pathways to decarbonization. The aim is to help investors, founders, policymakers and academics alike direct their energies towards the most relevant and investable opportunities, regardless of political headwinds.

“The scale at which the government participates in the development of these new technologies — or puts a thumb on the scale for technologies in particular — will vary,” Sonia Aggarwal, CEO of the policy firm Energy Innovation, which is also a member of the alliance, told me. “But certainly that has no real bearing on the fundamental fact that innovators are out there right now thinking about these grand challenges, and there are exciting new ideas for technologies that can get to that commercial scale in the coming years.”

And indeed, sometimes the most promising ideas can take shape in moments of deep uncertainty. Some of the biggest success stories of recent tech history — Uber, Airbnb, WhatsApp, and Square — all got their start during the 2008 financial crisis or its aftermath. “Some of the strongest companies and founders are building in uncertain times,” Dawn Lippert, founder and CEO of Elemental Impact, told me. “That’s very much what we see right now.”

These groups are far from the only private-sector actors coming together to help navigate industry headwinds. When the Environmental Protection Agency withdrew support for the most widely used U.S.-based carbon accounting model for estimating scope 3 emissions, leading emissions accounting platform Watershed partnered with Stanford University’s Sustainable Solutions Lab to launch an initiative that ensures continued access. And recognizing the difficulty that early stage climate tech startups face in securing insurance, the nonprofit GreenRE Coalition and the philanthropic funder Trellis Climate partnered to create a new type of bond tailored to the needs of climate tech startups.

Whether it will all be enough to accelerate or even sustain much-needed momentum in climate tech funding is impossible to predict. But at least the private sector seems to agree that, in this moment, good old teamwork is worth one heck of a try.

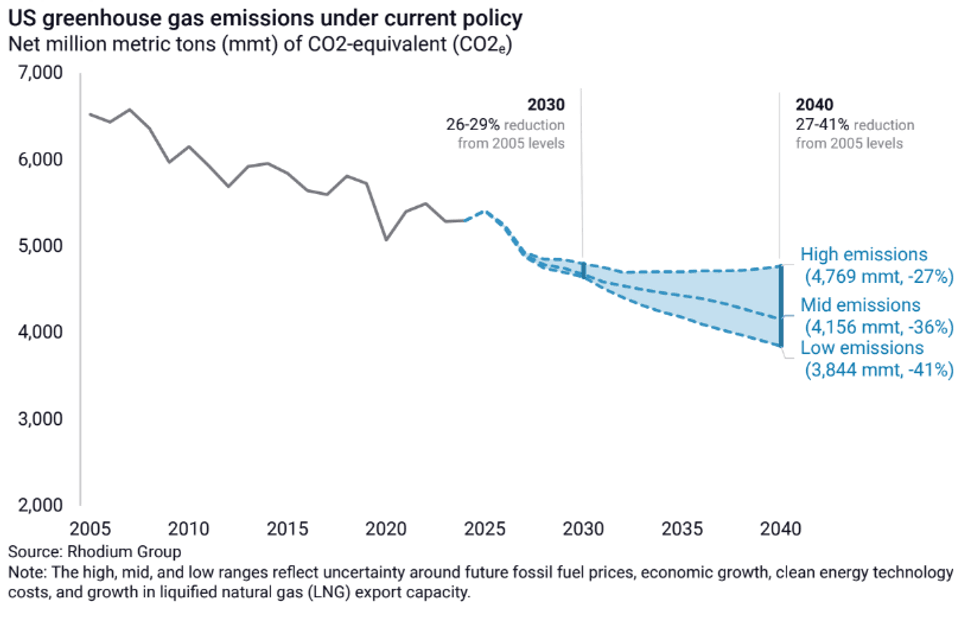

The 2030s crossroads.Rhodium Group

The 2030s crossroads.Rhodium Group