When politicians tell the CEO of Radiant that they love small modular reactors, he groans inwardly and just keeps smiling.

Doug Bernauer’s Radiant is not trying to make SMRs. His company — a VC-backed startup currently in the pre-application phase with the Nuclear Regulatory Commission — is designing a portable nuclear microreactor, which is intended to replace diesel generators. The politicians don’t always know the difference, Bernauer told me.

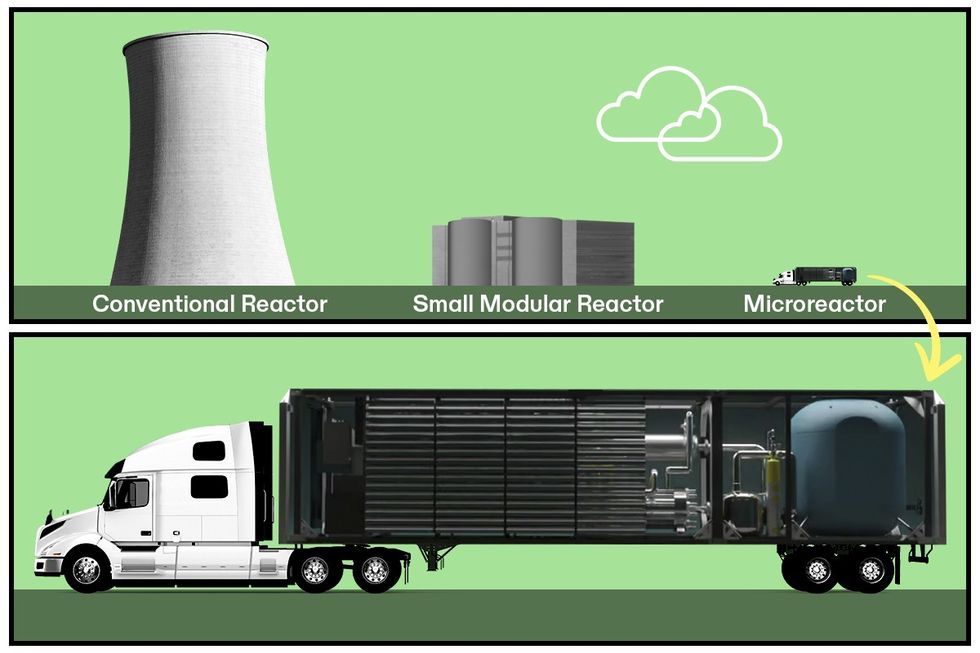

The SMR-microreactor confusion is common outside the world of nuclear. While they are both versions of advanced nuclear technologies not yet built in the United States (all of our nuclear power comes from big, old-fashioned plants), SMRs and microreactors have different designs, power outputs, costs, financing models, and potential use cases.

Unlike SMRs, microreactors are too small to ever become key energy players within a full-sized grid. But they could replace fossil fuels in some of the hardest to decarbonize sectors and locations in the world: mines, factories, towns in remote locations (especially Alaska and northern Canada), military bases, and (ironically) oil fields. For those customers, they could also make power supply and prices more consistent, secure, and dependable than fossil fuels, whose fluctuating prices batter industrial sectors and the residents of remote towns without discrimination.

Perhaps even more importantly, microreactors’ small size and comparatively low price could make them a gateway drug for new nuclear technologies in the U.S., helping companies and regulators build the know-how they need to lower the risk and cost for larger projects.

Heatmap Illustration/Radiant, IAEA, Getty Images

Heatmap Illustration/Radiant, IAEA, Getty Images

The big problem with this idea? No functional commercial nuclear microreactor actually exists. Industry experts cannot say with confidence that they know what the technological hurdles are going to be, how to solve them, or what it’s going to cost to address them.

“My crystal ball is broken,” John Parsons, an economist researching risk in energy at the Massachusetts Institute of Technology, said when I asked him whether he believed microreactors would make it through the technical gauntlet. “I’m hopeful. But I’m also very open-minded. I don’t know what’s going to happen. And I really believe we need a lot of shots on goal, and not all shots are going to go through,” he said.

Recent advances in both technology and regulation indicate that in the next few years, we should have some answers.

Private companies are expecting to conduct their first tests in about two years, and they are in conversations with potential customers. Radiant is hoping to test at the Idaho National Laboratory in 2026; Westinghouse and Ultra Safe Nuclear Corporation have contracts to test microreactors there as well. BWX Technologies is currently procuring the parts for a demonstration reactor through the Department of Defense’s prototype program — called Project Pele — and plans to test in about two years; X-energy signed an expanded contract in 2023 to build a prototype for Project Pele as well. Eielson Air Force Base in Alaska is commissioning a pilot microreactor. Schools including Pennsylvania State University and the University of Illinois have announced their interest as potential customers. Mining companies and other industry players in Alaska regularly express interest in embracing this technology.

The government is also quietly smoothing the way, removing barriers to make those tests possible. On March 4, the Nuclear Regulatory Commission released a new draft of licensing rules that will shape the future for these microreactors, and early March’s emergency spending bill included more than $2.5 billion repurposed for investment in a domestic supply chain of the type of nuclear fuel most advanced reactors will require.

“If we are truly committed as a nation to sticking to our climate goals, then we will absolutely get to a place where there are a bunch of microreactors replacing otherwise difficult to decarbonize sectors and applications,” said Kathryn Huff, the head of the office of nuclear energy at the Department of Energy.

Eric Gimon, a senior fellow at the nonprofit Energy Innovation, was a microreactor skeptic until about a month ago. His own recent research has made him far more optimistic that these microreactors might actually be technologically feasible, he told me when I reached out for an honest critique. “If they can make (the microreactors) work, it’s attractive,” he said. “There are a lot of industrial players that are going to want to buy them.”

“If your goal is to produce power at 4 cents per kilowatt hour, why would you buy any power that’s way more expensive than what you need? You do it because if that adds diversity to the portfolio and less variance, then you can get an overall portfolio that is lower cost or a lower risk for the same cost,” he told me.

Understanding the differences

Everyone I spoke to in the industry began our conversation with the same analogy: In the world of nuclear, full-size power plants are to airports what microreactors are to airplanes. Just as it's easier to build and regulate an airplane than an entire airport, in theory the microreactors should be built in a factory, regulated and licensed in the factory, and then rented out to or sold to the end user. An airport requires approvals specific to the construction site, a huge team of people employed for a long time to construct it and then another team to maintain it, and complicated financing based on the idea that the airport could be used for 50 or more years; a full-scale nuclear plant is the same. An airplane can basically be ordered online; a microreactor should be the same.

“They are sized to be similar to that kind of scope, where you could really consolidate a lot of the chemical and manufacturing oversight to a single location rather than moving thousands of people to a construction site,” Huff told me.

Microreactors should produce relatively small amounts of power (a maximum of 10-20 megawatts) and lots of heat with a tiny amount of nuclear fuel. They are usually portable, and if they aren’t portable they require a limited amount of construction or installation. Because it should not be possible to handle the fuel once it leaves the factory (most of the proposed reactor designs set the fuel deep into a dense, inaccessible matrix), these reactors wouldn’t require the same safety and security measures on site as a nuclear power plant. They’re easily operated or managed by people without nuclear expertise, and their safety design — called passive safety — should make it technically impossible for a reactor to meltdown.

“The excess reactivity is so small that you actually can’t get the reactor hot enough that you could start damaging the fuel. That’s something unique about the microreactor that would not necessarily be true for other types of nuclear,” Jeff Waksman, the program manager for the Department of Defense’s Strategic Capabilities Office, told me.

Microreactors should also cost on the order of tens of millions of dollars, not hundreds. That’s low enough that a company, university, town, or other similarly-sized entity could buy one or more of them. Because they’re cheaper than traditional nuclear, they don’t require lenders to take big risks on money committed over a very long period of time. If a mining company wanted to replace a diesel generator with one of these, they should be able to finance it in exactly the same way (a loan from the bank, for example). This makes their financial logic quite different from SMRs, which can suffer from some of the same problems as full-size nuclear power plants (see: NuScale’s recent setbacks).

“All of the things that contribute to a faster innovation cycle are true for microreactors compared to larger reactors. So you can just — build one,” said Rachel Slaybaugh, a partner at DCVC and a board member at Radiant, Fervo Energy, and Fourth Power.

The cost problem

Because microreactors max out at around 20 megawatts of energy, the economies of scale that eventually bring down energy prices for full-scale nuclear power can’t be replicated. While Jigar Shah, the director of the loan programs office at the DOE, speculated in a recent interview that costs might eventually go just below 10 cents per kilowatt hour, Parsons is skeptical that anyone could provide a practical cost estimate. It’s absolutely going to cost more than either large reactors or SMRs, Parsons said.

But cost comparisons to other types of nuclear technology aren’t practical, according to Slaybaugh. “You are going to be able to command a cost parity with diesel generators. It’s easy to get to a point where they make financial sense,” she said. “You can see why someone would pick one: This is not making noise, it’s not making local air pollution, you don’t have to deal with the diesel logistics complexity. You sell it at price parity, and maybe the first few customers pay a premium because they are excited about it.”

That premium price for the initial technology is the largest hurdle raised by every single person I spoke with, from the DOE to analysts and researchers to the different microreactor companies.

But there is one customer already inclined to pay a substantial premium: the Department of Defense. The U.S. military has greater resiliency and security needs than other consumers when it comes to its power supply, making the cost of microreactors more palatable. (And it doesn’t hurt that the taxpayer already foots the bill for enormous defense contracts, including for aircraft carriers and submarines powered by nuclear reactors). It’s common for technological innovations (think the internet, GPS, advanced prosthetics) to begin with the military and then expand outward to the consumer. Project Pele and the requests for proposals at Eielson Air Force Base both indicate that the pathway might be one for microreactors, according to Parsons.

For the president of BWXT Advanced Technologies, the Department of Defense’s decision to commission his company’s microreactor for Project Pele removed his last doubts that these microreactors would eventually be built. “The DOD being the first mover has extreme advantage for the country, and for eventually the commercial industry,” Joseph Miller told me. “The first mover was the barrier, and now it’s just 1,000 things that we’re working on all day every day to make it real, and there’s no gotcha out there that I see. That wasn’t the case when we were doing the design work, but now we’re making procurements to be able to assemble and deliver the reactor.”

Regardless of whether Miller’s optimism is well-founded, the experience gained in trying to make them happen is invaluable for a nuclear industry that’s been stuck in the mud for far too long.

“I've been talking with the federal government about the fact that there’s broader value in terms of getting wins on the board for the nuclear sector and getting the industry more experienced with building new things in a way that isn't quite so complicated,” Slaybaugh said. “Let’s have them build a thing that’s small and kind of cheap, and then they can go build a bigger thing that’s a little more expensive and a little more complicated. Let’s get some real reps in with microreactors.”

Heatmap Illustration/Radiant, IAEA, Getty Images

Heatmap Illustration/Radiant, IAEA, Getty Images